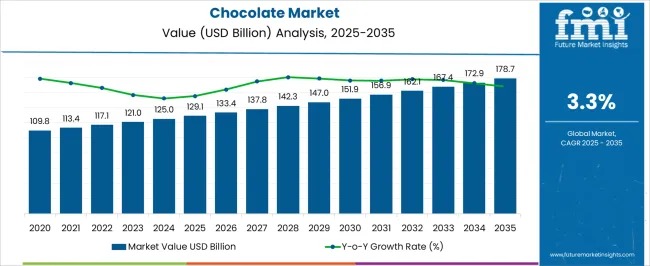

The global chocolate market continues to expand steadily, underpinned by strong consumer demand and sustained innovation, while operating within one of the most regulated environments in the food industry. Valued at USD 129.1 billion in 2025, the market is projected to reach USD 178.7 billion by 2035, registering a compound annual growth rate (CAGR) of 3.3% over the forecast period. This measured growth reflects a mature yet resilient sector balancing indulgence, health considerations, sustainability, and compliance across major global markets.

Chocolate manufacturers operate under stringent food safety laws, labeling mandates, and ingredient regulations enforced by authorities in North America, Europe, and Asia-Pacific. These frameworks directly influence formulation choices, packaging standards, and production processes. While compliance increases operational costs through investments in quality assurance, testing, and certification, it also reinforces consumer trust and long-term brand equity in an increasingly transparent food ecosystem.

Get Exclusive Access To Data Tables, Market Sizing Dashboards, And Analyst Insights. Request Sample Report! https://www.futuremarketinsights.com/reports/sample/rep-gb-26037

Regulatory oversight has also accelerated innovation across the chocolate value chain. Restrictions on sugar content, mandatory allergen disclosures, and limitations on additives have prompted manufacturers to develop sugar-reduced, high-cocoa, and clean-label alternatives. At the same time, sustainability-focused regulations and voluntary certifications promoting ethical cocoa sourcing have reshaped procurement strategies. Although these initiatives raise sourcing and compliance costs, they strengthen brand positioning among ethically conscious consumers and institutional buyers.

Trade policies and import-export tariffs further shape competitive dynamics, influencing regional pricing strategies and market accessibility. As a result, regulatory factors act as both constraints and catalysts, guiding strategic decision-making and reinforcing the market’s gradual but stable growth trajectory.

Market Snapshot and Structural Importance

Chocolate represents a significant pillar of the global confectionery and sweet goods industry, accounting for approximately 18% of total confectionery consumption worldwide. Within the dark, milk, and white chocolate category, it holds a 12.5% share, driven by flavor diversity and functional benefits. The market also contributes nearly 15% to the broader sweet and snack foods ecosystem, supported by strong gifting traditions, convenience formats, and brand loyalty.

Quick Market Highlights (2025):

- Market value: USD 129.1 billion

- Forecast value (2035): USD 178.7 billion

- CAGR (2025–2035): 3.3%

- Leading segment: Milk chocolate (51.2% share)

- Key growth regions: North America, Europe, Asia-Pacific

Milk Chocolate Maintains Market Leadership

Milk chocolate continues to dominate the global market, capturing 51.2% of total revenue in 2025. Its creamy texture, balanced sweetness, and broad demographic appeal make it the preferred choice across mature and emerging markets. Strong brand recognition, cost-efficient mass production, and seasonal gifting demand further reinforce its leadership position. Ongoing flavor extensions and nostalgic marketing campaigns ensure sustained relevance across age groups.

Packaging and Distribution Shape Market Reach

Plastic packaging leads the market with a 43.7% share, valued for its durability, lightweight nature, and barrier properties that protect against moisture and oxygen. Innovations in recyclable and biodegradable plastics are helping manufacturers align with sustainability goals while maintaining operational efficiency.

On the distribution front, supermarkets and hypermarkets account for 48.9% of chocolate sales, benefiting from high footfall, promotional pricing, and impulse buying behavior. Strategic shelf placement, in-store marketing, and seasonal assortments continue to drive volume through organized retail, complemented by the rapid rise of e-commerce and direct-to-consumer models.

Growth Drivers Reinforce Long-Term Stability

The chocolate market’s steady expansion is supported by premiumization trends, rising disposable incomes, and urbanization, particularly in emerging economies. Consumers are increasingly drawn to high-quality ingredients, artisanal offerings, and functional chocolates enriched with vitamins, probiotics, or plant-based components. Digital marketing, personalized gifting, and subscription models are further reshaping purchasing behavior and broadening consumer reach.

Technological advancements in cocoa processing, fermentation, and supply chain traceability have enhanced product consistency and sustainability outcomes. These efficiencies reduce waste, stabilize input costs, and improve time-to-market, strengthening competitiveness across regions.

Regional Momentum Across Key Markets

Asia-Pacific remains the fastest-growing region, led by China (4.5% CAGR) and India (4.1% CAGR), driven by premium gifting culture, expanding modern retail, and digital commerce adoption. Europe shows stable growth, with Germany (3.8%) and France (3.5%) benefiting from demand for premium, organic, and ethically sourced chocolates. The United States (2.8%) reflects a mature market focused on artisanal, functional, and low-sugar innovations.

Competitive Landscape Focused on Experience and Trust

Global leaders such as Mars, Incorporated, Nestlé SA, Ferrero Group, Mondelēz International, and The Hershey Company continue to dominate through scale, brand strength, and global distribution. Meanwhile, companies like Barry Callebaut AG serve the B2B segment with specialty formulations, while premium players such as Lindt & Sprüngli differentiate through craftsmanship, heritage, and ethical sourcing.

Competition has shifted beyond price toward product experience, sustainability credentials, and brand storytelling. As regulations tighten and consumer expectations evolve, companies that successfully integrate compliance, innovation, and ethical practices are best positioned to capture value in the global chocolate market through 2035.