The global eye health ingredients industry is entering a phase of sustained value expansion, underpinned by rising consumer focus on preventive healthcare and vision longevity. Valued at USD 174.8 million in 2025, the market is projected to reach USD 360.3 million by 2035, advancing at a CAGR of 7.5% over the decade. This growth trajectory translates into an absolute dollar opportunity of nearly USD 185.5 million, highlighting the increasing commercial relevance of specialized ingredients formulated to support ocular health.

Market analysts note that this expansion is not driven by volume alone, but by value-added formulations incorporating clinically supported carotenoids, antioxidants, and omega-based compounds. The shift reflects a broader transformation in consumer behavior, where eye health is no longer addressed reactively but is increasingly managed through daily nutrition, supplements, and fortified foods. As digital lifestyles intensify and populations age, eye health ingredients are becoming integral to long-term wellness strategies rather than niche additions.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-25055

The market’s consistent growth is also reinforced by frequent product launches and the deepening integration of nutraceuticals into everyday consumption. Eye health ingredients are now widely present across dietary supplements, functional foods, beverages, and ophthalmic formulations, strengthening their visibility across both preventive and lifestyle-driven categories. Over the forecast period, the sizeable absolute dollar opportunity underscores a favorable environment for established ingredient suppliers as well as emerging innovators focused on differentiated formulations.

Market Size, Contribution, and Strategic Importance

Eye health ingredients represent a meaningful pillar within the broader nutrition and wellness ecosystem. The segment is estimated to contribute nearly 9% of the nutraceutical ingredients market, about 11% of the dietary supplements market, close to 7% of the functional food and beverages market, nearly 10% of preventive healthcare ingredients, and around 6% of the specialty ingredients market. When viewed collectively, this equates to an aggregated influence of approximately 43% across its parent categories.

This substantial overlap demonstrates that eye health ingredients are not confined to a single application area. Instead, they influence sourcing strategies, formulation decisions, and product positioning across multiple verticals. Rising consumption of lutein, zeaxanthin, beta carotene, vitamin A, bilberry extracts, and omega-3 fatty acids has reinforced the segment’s importance, particularly as these compounds are increasingly associated with reducing risks of age-related macular degeneration, cataracts, dry eye syndrome, and digital eye strain.

Why the Market Is Expanding Steadily

Growth in the eye health ingredients market is being driven by a convergence of demographic, lifestyle, and scientific factors. Increasing screen exposure across all age groups has amplified awareness of digital eye strain, while aging populations globally are more proactive about maintaining vision quality. Nutraceutical research and public health publications continue to highlight the role of dietary supplementation in ocular wellness, encouraging broader adoption.

At the same time, consumers are gravitating toward ingredients with strong clinical backing. Manufacturers have responded by investing in formulation science, combining antioxidants, carotenoids, and essential fatty acids into targeted blends designed for enhanced efficacy. Expanding distribution through online platforms, specialty health stores, and mass retail channels has further accelerated accessibility and uptake.

Segmental Dynamics Shaping Market Value

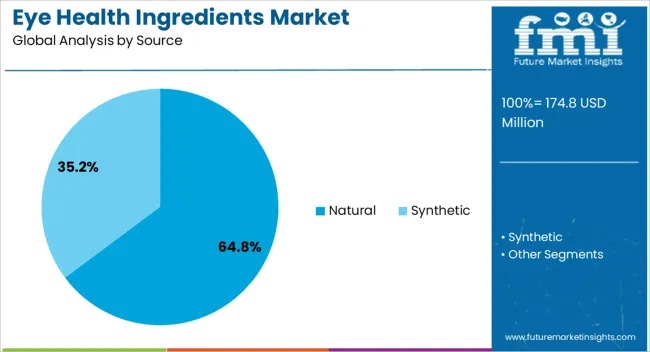

By source, natural eye health ingredients dominate the market, accounting for an estimated 64.8% of revenue in 2025. Consumer preference for plant-based and minimally processed ingredients has driven demand for naturally derived carotenoids and antioxidants. Ingredients sourced from marigold flowers, bilberry, algae, and botanical extracts are widely perceived as safer and better aligned with clean-label expectations, enabling suppliers to command premium pricing.

By ingredient type, lutein leads the market with an estimated 39.5% share in 2025. Its well-documented role in retinal health and protection against blue-light-induced oxidative stress has made it a cornerstone of modern eye health formulations. Continuous clinical validation and improved extraction technologies have enhanced lutein’s stability and potency, supporting its widespread inclusion across supplements, fortified foods, and functional beverages.

From a formulation standpoint, soft gel delivery formats are projected to account for 41.7% of market revenue in 2025. Their dominance stems from superior bioavailability, particularly for lipid-soluble compounds such as lutein, zeaxanthin, and omega-3 fatty acids. Soft gels also offer precise dosing, ingredient protection, and consumer convenience, making them the preferred choice for premium nutraceutical brands.

Regional Growth Patterns Highlight Emerging Opportunities

Regionally, the eye health ingredients market shows varied growth dynamics. Asia-Pacific is emerging as the fastest-growing region, supported by large populations, expanding nutraceutical manufacturing capacity, and rising adoption of fortified products. China leads global growth with a projected CAGR of 10.1%, driven by high screen time, increasing myopia prevalence, and strong domestic production of lutein and zeaxanthin.

India follows with a CAGR of 9.4%, supported by a growing middle class, increased awareness of preventive nutrition, and expanding functional food and supplement consumption. European markets such as Germany, France, and the UK exhibit steady growth, characterized by regulatory compliance, premium formulations, and strong consumer trust in clinically validated products. The United States, while more mature, continues to generate stable demand due to high healthcare spending and consistent adoption of condition-specific eye health supplements.

Drivers, Trends, and Market Challenges

Key demand drivers include heightened awareness of preventive healthcare, rising incidence of vision-related disorders, and strong interest in functional nutrition. Clean-label preferences, plant-derived carotenoids, and algae-based omega-3s are shaping ingredient selection. Personalized nutrition is also gaining momentum, with tailored eye health solutions designed around age, lifestyle, and screen exposure.

However, the market faces notable challenges. Agricultural dependency for carotenoid sourcing creates raw material price volatility, while high extraction and production costs can limit affordability. Regulatory complexity around health claims and labeling standards remains a barrier, particularly for smaller players with limited compliance resources.

Competitive Landscape and Outlook

Competition in the eye health ingredients market centers on translating scientific credibility into market trust. Leading players such as Alcon, Bausch & Lomb, Amway, Solgar, BASF, DSM, and MacuShield emphasize clinically supported formulations, ingredient provenance, and bioavailability. Differentiation increasingly depends on how effectively suppliers communicate efficacy, stability, and regulatory compliance to brand owners and formulators.

Looking ahead, the eye health ingredients market is positioned for sustained growth as preventive vision care becomes a mainstream priority. Investments in ingredient innovation, natural sourcing, and targeted formulations are expected to define competitive advantage, making eye health ingredients a strategic focus area across the global nutrition, wellness, and healthcare landscape.