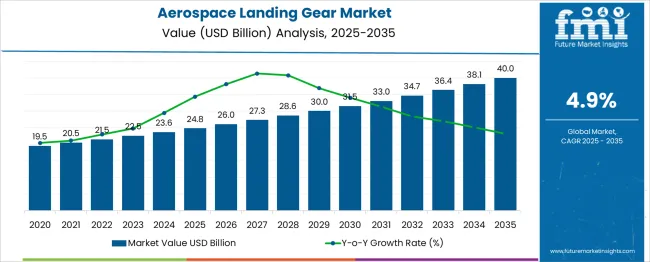

The global Aerospace Landing Gear Market is entering a decade of stable, high-confidence expansion, with total market value forecast to rise from USD 24.8 billion in 2025 to USD 40.0 billion by 2035, registering a compound annual growth rate (CAGR) of 4.9%. The market’s trajectory reflects consistent aircraft production growth, strong OEM backlogs, and a structural shift toward lighter, more durable, and digitally enabled landing gear systems.

Between 2025 and 2030, the market is expected to grow to USD 31.5 billion, adding USD 6.7 billion in incremental value and averaging USD 1.3 billion in annual gains. This phase is supported by narrow-body aircraft production stability, regional fleet expansion, and predictable aftermarket replacement cycles. Established suppliers with long-standing OEM certifications and deep platform integration are positioned to retain, and in some cases strengthen, their market share due to high technical and regulatory barriers to entry.

From 2030 to 2035, the market accelerates further, adding USD 8.5 billion in value as annual increments approach USD 1.9 billion by the end of the forecast window. Growth in this period is reinforced by rising global passenger traffic, rapid growth of regional and low-cost carriers, and large-scale upgrades to advanced landing gear architectures that prioritize weight reduction, lifecycle efficiency, and digital condition monitoring.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-23369

Main Landing Gear Systems Anchor Market Revenue

By 2025, main landing gear (LG) systems are projected to account for 61.0% of global market revenue, reflecting their essential role in supporting aircraft loads during taxi, takeoff, and landing. The segment’s dominance is reinforced by engineering investments in shock absorption, load distribution, retraction mechanisms, and structural fatigue resistance. Modularization and weight-optimized architectures are increasingly standard in next-generation main landing gear designs, enabling easier maintenance and reduced aircraft downtime.

The recurring overhaul requirements of main landing gear assemblies within global maintenance, repair, and overhaul (MRO) networks are also contributing to consistent revenue streams, particularly for narrow-body and wide-body commercial aircraft fleets.

Tri-Cycle Configurations Become the Global Standard

The tri-cycle landing gear arrangement is forecast to hold 67.0% of total market share in 2025, underlining its position as the preferred configuration across both commercial and military platforms. This architecture delivers superior aircraft balance, safer ground handling, enhanced pilot visibility, and reduced aerodynamic drag during taxi operations.

Advances in nose-wheel steering systems, hydraulic actuation units, and distributed braking technologies have improved operational precision and reliability. Global airworthiness directives and fleet standardization strategies continue to reinforce tri-cycle arrangements as the default configuration for newly developed aircraft.

Fixed-Wing Aircraft Drive Platform-Level Demand

Fixed-wing aircraft are expected to represent 54.0% of total market share in 2025, supported by strong demand from commercial aviation, defense aviation, and air cargo operators. This platform segment encompasses a wide range of aircraft, from regional jets to wide-body intercontinental aircraft and intelligence, surveillance, and reconnaissance platforms.

Surging cargo traffic, particularly in Asia-Pacific and the Middle East, is accelerating the adoption of landing gear systems optimized for higher landing weights and faster turnaround cycles. OEMs and Tier 1 suppliers are increasingly embedding digital diagnostics and lifecycle management tools to minimize ground time and maximize operational efficiency.

Advanced Materials Reshape Landing Gear System Design

Material innovation is transforming the performance profile of modern landing gear. Increased use of titanium alloys, carbon composites, and high-strength steels is enabling higher load-bearing capacity while reducing system weight. These material shifts directly contribute to lower aircraft fuel consumption and reduced carbon emissions across airline fleets.

Manufacturers are also integrating embedded health monitoring sensors that track stress cycles, temperature variations, and hydraulic performance in real time. Predictive maintenance, powered by digital data streams, is becoming a standard capability, allowing operators to schedule overhauls based on actual component condition rather than fixed service intervals.

The gradual transition toward electric and hybrid actuation systems is further optimizing energy efficiency and reducing dependency on traditional hydraulic architectures, aligning landing gear systems with next-generation aircraft sustainability targets.

MRO and Aftermarket Services Provide Structural Revenue Stability

The aerospace landing gear aftermarket remains a structurally resilient revenue channel. Regulatory mandates require periodic landing gear inspections, disassembly, refurbishment, and re-certification after predefined flight cycles or calendar intervals. This recurring demand has made landing gear one of the most predictable segments within the broader aircraft MRO ecosystem.

MRO providers across North America, Europe, and Asia-Pacific are expanding specialist capabilities to handle complex gear assemblies and next-generation material systems. The growing trend of maintenance outsourcing by airlines is creating scalable opportunities for independent MRO providers and OEM-authorized service centers.

Personalize Your Experience: Ask for Customization to Meet Your Requirements

https://www.futuremarketinsights.com/customization-available/rep-gb-23369

Asia-Pacific Emerges as the Fastest-Growing Regional Hub

While North America continues to hold a leadership position due to established OEMs and mature MRO infrastructure, Asia-Pacific is demonstrating the most rapid expansion. China is forecast to grow at a 6.6% CAGR, supported by rising domestic aircraft production and modernization of airline fleets. India, with a projected 6.1% CAGR, is benefitting from defense procurement programs, regional connectivity expansion, and increasing MRO investments.

In Europe, Germany is advancing at 5.6% CAGR, driven by strong engineering capabilities and participation in multinational aerospace programs. The United Kingdom is expanding at 4.7% CAGR, supported by exports and high-value component manufacturing. The United States, at 4.2% CAGR, reflects stable growth across commercial, defense, and business aviation programs.

High Barriers to Entry Preserve Competitive Stability

The aerospace landing gear market remains highly protected by engineering complexity, certification rigor, and long product lifecycle requirements. High-precision manufacturing, extensive qualification testing, and long-term service obligations make competitive displacement difficult, ensuring that incumbent suppliers maintain strong strategic positions over the forecast period.

Leading industry participants include Safran Landing Systems, Heroux-Devtek, Inc., SPP Canada Aircraft, Inc., Triumph Group, UTC Aerospace Systems, Magellan Aerospace, Liebherr Group, Hawker Pacific Aerospace, GKN Aerospace, and Eaton Corporation. These companies continue to expand through material innovation, digital system integration, and global MRO network development.

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.