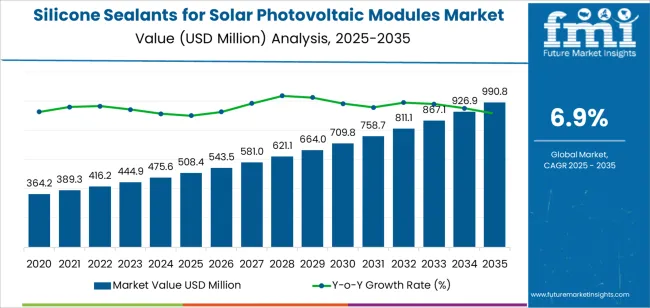

The global Silicone Sealants for Solar Photovoltaic Modules market is on course for remarkable expansion, with an estimated valuation of USD 508.4 million in 2025 and a forecasted rise to nearly USD 990 million by 2035. Driven by the unabated global shift toward renewable energy, this upward trajectory presents outstanding opportunities for both established chemical manufacturers and new entrants poised to innovate and scale within the evolving solar ecosystem.

Silicone sealants play an essential role in the durability, performance, and longevity of solar photovoltaic (PV) modules — acting as resilient adhesive agents that protect assemblies from extreme temperatures, moisture intrusion, and UV degradation. As global demand for solar installations — from residential rooftops to utility-scale farms — continues to mount, so too does the need for more advanced silicone sealing solutions that can withstand diverse operating conditions.

Market Growth Dynamics

The decade through 2035 is expected to be defined by strong double-digit momentum in the PV sealants segment, fueled by rapid solar deployment and ongoing enhancements in material science. Improvements such as neutral-cure formulations, accelerated curing times, and enhanced optical clarity are among the technological advancements that enable silicone sealants to align more closely with next-generation modules, including bifacial and flexible technologies.

A growing emphasis on sustainability, automation, and performance optimization is reshaping how manufacturers approach sealant formulation and application. With the rise of automated dispensing systems and AI-enabled quality control platforms, solar module producers — both veterans and newcomers — are finding new ways to integrate silicone sealants into their production lines with greater efficiency, repeatability, and minimal waste.

Opportunities for Established Players and New Entrants

Long-standing industry leaders with robust R&D capabilities are actively broadening their portfolios to capture this growth. Well-known chemical conglomerates are expanding regional manufacturing footprints to reduce lead times and tailor solutions for specific environmental conditions — from tropical climates to high-latitude freeze-thaw cycles. These companies continue to invest in specialized silicone blends that excel in adhesion, thermal cycling resistance, and weatherproofing — all critical to ensuring module longevity and return on investment for solar asset owners.

At the same time, emerging manufacturers and innovative startups are capitalizing on niche opportunities created by rapid solar adoption. These newer players are carving out competitive advantages through flexible, cost-effective sealant solutions, and by partnering with module assemblers to co-develop products tuned to unique market demands. Strategic collaborations between sealant innovators and solar module producers are increasingly common, fostering new technologies that enhance module reliability while reducing installation complexity.

Emerging players are also pushing forward with sustainable initiatives — developing low-VOC, halogen-free sealant options that resonate with environmentally conscious customers and align with global clean-energy commitments.

To access the complete data tables and in-depth insights, request a sample report here

Regional Trends Driving Demand

Asia Pacific remains at the forefront of this market’s expansion, reflecting extensive solar capacity additions in countries such as China and India. High growth in these regions is underpinned by favorable policy frameworks, ambitious renewable targets, and increasing private-sector investment in solar infrastructure — all of which boost demand for high-performance sealing materials.

In Europe, robust decarbonization commitments continue to stimulate demand, while technologically mature markets in North America sustain steady growth through both utility and residential solar deployment. Across these regions, a combination of government incentives, technology modernization, and advancing module designs contribute to a resilient and growing market demand for silicone sealants.

Key Market Segments and Innovation Foci

The market is diversified across several key segments, including dealcoholized silicone sealants, which are widely adopted due to their superior performance in bonding and weather resistance. Residential solar systems, in particular, account for a large portion of sealant demand as homeowners increasingly adopt rooftop installations to reduce energy costs and carbon footprints.

Commercial and industrial solar projects also represent significant demand centers, as businesses pursue sustainability goals and energy independence. Product innovations catering to these segments emphasize long-term performance, compatibility with automated application systems, and improved resistance to environmental stressors.

Outlook and Future Prospects

With the global economy accelerating its pivot toward renewable energy, the outlook for silicone sealants in solar applications is positive. Between now and 2035, market growth is expected to remain robust, underpinned by ongoing solar capacity expansion, regulatory support for clean energy, and continuous material advancements.

Both well-established chemical manufacturers and agile newcomers stand to benefit from this growth — whether by enlarging existing production capabilities, entering new geographic markets, or offering differentiated technologies that address evolving customer needs. As solar technologies become more sophisticated and widespread, silicone sealants will remain a critical enabler of module performance and longevity, reinforcing their strategic importance within the solar value chain.