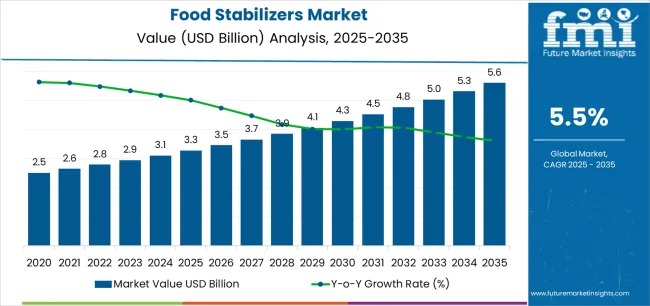

The food stabilizers market stands at the threshold of a transformative decade, reshaping the food processing and ingredient manufacturing landscape. Valued at USD 3.3 billion in 2025, the market is projected to grow to USD 5.6 billion by 2035, reflecting a robust CAGR of 5.5%, according to Future Market Insights. This growth is underpinned by increasing adoption of advanced stabilization technologies, enhanced texture standardization, and demand across confectionery, dairy, and beverage processing sectors.

Explore trends before investing – request a sample report today!

The market’s growth trajectory can be divided into two distinct phases. Between 2025 and 2030, the sector is expected to expand from USD 3.3 billion to approximately USD 4.23 billion, adding USD 0.95 billion in value. This early phase is driven by rising consumer preference for clean-label products, natural stabilizer systems, and automated quality monitoring solutions. Facilities are increasingly integrating enhanced processing capabilities as standard expectations rather than premium offerings.

From 2030 to 2035, the market is forecasted to climb from USD 4.23 billion to USD 5.6 billion, accounting for USD 1.09 billion in incremental value. Growth during this period will be fueled by plant-based stabilizer adoption, integration with traceability platforms, and seamless compatibility with existing food production infrastructure.

The market’s expansion reflects evolving operational and regulatory landscapes. Product development teams, regulatory affairs, engineering, and procurement functions must navigate complex requirements, balancing functional performance with safety documentation and regional compliance standards. European Union regulations demand proof of additive safety before market introduction, while the US relies on Generally Recognized as Safe (GRAS) designations, highlighting the importance of multi-regional regulatory strategies.

Key Market Insights

- Market Value (2025): USD 3.3 billion

- Market Forecast (2035): USD 5.6 billion

- CAGR (2025–2035): 5.5%

- Leading Ingredient: Pectin (32.8% share)

- Primary Application: Confectionery manufacturing

- Key Growth Regions: Asia Pacific, North America, Western Europe

The revenue distribution highlights evolving market dynamics. Bulk stabilizer sales currently represent 40% of revenue, while private-label and co-packing account for 22%. Foodservice, industrial, and retail branded products cover the remaining 38%. Future growth emphasizes clean-label formulations (28–32%), plant-based solutions (22–25%), functional blends (18–22%), and custom solutions (15–18%).

Market Segmentation and Trends

By ingredient, pectin-based stabilizers dominate with 32.8% market share, valued at USD 1.08 billion in 2025. These systems offer superior gelling properties, operational flexibility, and compatibility with automated manufacturing lines. Xanthan gum and carrageenan maintain specialized growth, providing extended shelf-life, suspension stability, and support for clean-label beverages and sauces.

Confectionery applications lead by end-use, with a 27.8% market share driven by texture-critical products such as gummies, marshmallows, and jellied confections. Dairy and dessert applications are witnessing premium growth, especially in Asia Pacific and Latin America, where freeze-thaw stability and syneresis control are critical.

Drivers and Restraints

- Drivers:

- Rising clean-label demand

- Growth of processed foods due to urbanization

- Innovation in texture and sensory experiences

- Restraints:

- Raw material volatility affecting supply and pricing

- Regulatory complexity limiting global standardization

Regional Highlights

India leads the market with a 6.5% CAGR, propelled by expanding food processing and dairy sectors. Urban centers such as Mumbai, Delhi, and Bangalore adopt stabilizers widely in yogurt, ice cream, and confectionery. China follows at 6.0% CAGR, with urban food facilities integrating stabilizers for efficiency and consistent product quality.

North America demonstrates steady growth, particularly in the US (2.3% CAGR), driven by mature food processing infrastructure and clean-label adoption. European markets, led by Germany (3.7%) and France (3.5%), prioritize technical excellence, premium positioning, and culinary innovation in bakery and dairy applications.

Competitive Landscape

The market is moderately consolidated, with ~20–25 credible players, where the top five account for 45–50% of revenue. Key players include:

- Cargill Incorporated

- Ingredion Incorporated

- Tate & Lyle plc

- Archer Daniels Midland Company (ADM)

- Palsgaard A/S

- DuPont de Nemours Inc.

- Kerry Group plc

- CP Kelco

- Ashland Global Holdings Inc.

- BASF SE

- Koninklijke DSM N.V.

- Nexira

- TIC Gums Inc.

- Naturex (Givaudan)

- Fiberstar Inc.

Leading companies differentiate through innovation, application expertise, clean-label portfolios, and technical service quality. Commoditization is most evident in basic gum grades, while clean-label, functional blends, and customized solutions offer margin opportunities.

Strategic Imperatives for Stakeholders

Manufacturers and processors are encouraged to:

- Design solutions beyond stabilization, integrating emulsifiers, application guides, and technical support.

- Adopt preconfigured formulations for dairy, bakery, beverages, and standardized texture profiles.

- Focus on natural sourcing, supply chain transparency, and premium positioning for health-conscious markets.

- Implement quality-by-default systems including digital batch tracking, microbiological testing, and blockchain traceability.

As the global food stabilizers market advances, stakeholders positioned to innovate, adapt to regulatory changes, and cater to evolving consumer preferences are set to reap the greatest benefits.