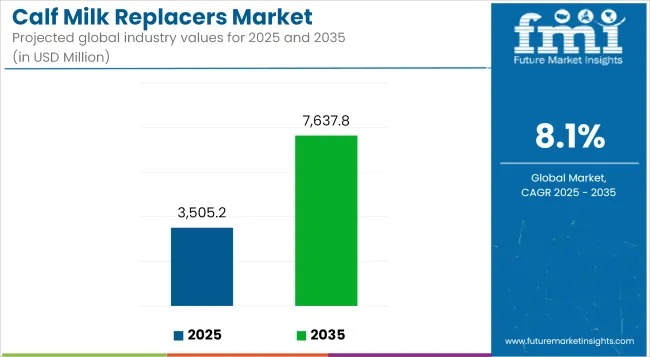

The global calf milk replacer market is entering a decisive growth phase as commercial dairy and beef producers increasingly prioritize early-life nutrition to improve lifetime animal performance and farm economics. Valued at USD 3,505.2 million in 2025, the market is projected to more than double, reaching USD 7,637.8 million by 2035, advancing at a strong compound annual growth rate (CAGR) of 8.1%. This expansion reflects a structural shift away from whole milk feeding toward scientifically formulated replacers that deliver consistent nutrition, cost efficiency, and improved herd health outcomes.

Explore trends before investing – request a sample report today!

Across developed and emerging dairy markets, calf milk replacers are being recognized not merely as substitutes for whole milk, but as strategic tools to optimize gut development, immunity, and growth velocity during the most critical stages of a calf’s life. Rising dairy productivity targets, increasing herd sizes, and ongoing farm consolidation are accelerating adoption, particularly within large-scale and automated operations where consistency and performance predictability are paramount.

Industry Value Analysis Highlights a Strong Decade of Expansion

In value terms, the calf milk replacer industry demonstrates one of the most resilient growth profiles within the animal nutrition sector. The global market is estimated at USD 3,505.2 million in 2025 and is forecast to reach USD 7,637.8 million by 2035, supported by an 8.1% value-based CAGR. Powdered formulations are expected to command close to four-fifths of total demand by 2025, owing to their extended shelf life, ease of transportation, precise dosing capabilities, and compatibility with automated feeding systems.

Medicated milk replacers continue to account for a significant share of global consumption, driven by heightened awareness of early-stage disease prevention and calf mortality reduction. However, regulatory pressure on antibiotic usage is steadily reshaping the competitive mix, opening new opportunities for non-medicated, functionally fortified alternatives.

Semi-Annual Growth Patterns Signal Accelerating Momentum

A closer look at semi-annual performance trends reveals improving revenue realization over time. From 2024 to 2034, the industry is estimated to grow at a CAGR of 7.7% in the first half (H1) and 8.3% in the second half (H2). This momentum strengthens further in the 2025 to 2035 outlook, with H1 growth at 7.9% and H2 accelerating to 8.5%.

The sequential rise of 46 basis points in H2 2025 underscores strengthening downstream demand, particularly from commercial dairy farms upgrading feeding protocols and integrating automation-friendly replacer solutions. These patterns suggest sustained investment attractiveness and predictable long-term growth for stakeholders.

Precision Nutrition and Functional Fortification Drive Product Innovation

One of the most defining trends reshaping the calf milk replacer market is the growing emphasis on precision nutrition. Scientific evidence increasingly demonstrates that nutrition during the first 30 to 45 days of life plays a decisive role in determining future milk yield, reproductive efficiency, and overall herd longevity. As a result, manufacturers are enriching replacers with targeted amino acids, vitamins, probiotics, prebiotics, nucleotides, and bovine colostrum extracts.

These bioactive additions are designed to enhance gut microbiota balance, reduce digestive disorders such as scours and bloating, and strengthen immune resilience without reliance on antibiotics. Premium replacers featuring yeast extracts, beta-glucans, and selenium chelates are gaining traction among farms focused on long-term productivity rather than short-term cost savings.

Transition Toward Whey-Based Proteins Improves Cost Stability

Volatility in skim milk powder pricing has accelerated the industry-wide transition toward whey protein concentrates (WPCs), whey protein isolates (WPIs), and hydrolyzed whey proteins. Derived from cheese manufacturing by-products, whey proteins offer superior digestibility, a favorable amino acid profile, and improved immune support for neonatal calves.

Advancements in whey processing technologies now enable the production of low-allergen, high-absorption hydrolysates, allowing manufacturers to deliver nutritionally dense formulations while reducing dependency on unstable dairy fat markets. This shift is strengthening supply chain sustainability and improving margin resilience across the value chain.

Asia-Pacific Emerges as a High-Growth Investment Hotspot

Asia-Pacific is expected to increase its share of the global calf milk replacers market from 12.6% in 2025 to 19.8% by 2030, fueled by rapid dairy intensification in China, India, Vietnam, and Southeast Asia. Unlike Western dairy systems, Asian operations often require formulations adapted to high temperatures, variable water quality, and locally available feed inputs.

Multinational players such as ADM and Charoen Pokphand Group are responding by localizing production and R&D, emphasizing plant-based protein blends, encapsulated fats, and heat-stable probiotics. Regulatory initiatives, including China’s “National Plan to Promote Calf Health and Growth 2021–2030,” are further accelerating demand for antibiotic-free, functionally enriched replacers.

Regulatory Push Accelerates Antibiotic-Free Innovation

By 2025, approximately 36.1% of calf milk replacers sold in the European Union are expected to carry antibiotic-free or medication-free claims. Tightened oversight under the European Medicines Agency’s Veterinary Medicinal Products Regulation is driving reformulation efforts across the industry.

Manufacturers are increasingly replacing medicated solutions with plant-derived immunostimulants, organic acids, essential oils, and microencapsulated probiotics. This shift is also influencing procurement policies in North America, where large cooperatives are aligning sourcing with ESG benchmarks and retailer expectations.

Automation and Liquid Replacers Gain Traction

Labor shortages and rising operational costs are accelerating the adoption of automated calf feeding systems, particularly in North America and Europe. This trend is boosting demand for liquid milk replacers and instantized powders with optimized solubility, low foam, stable viscosity, and reduced sedimentation.

Manufacturers are investing in pre-mixed liquid concentrates and automation-compatible formulations to support precision feeding, real-time intake monitoring, and improved labor efficiency. Automation-ready replacers are expected to be a major growth driver through the latter half of the decade.

Competitive Landscape Reflects Moderate Market Concentration

The global calf milk replacer market exhibits moderate concentration, with Tier 1 players such as Land O’Lakes, Cargill, Nutreco, ADM, and FrieslandCampina holding a significant share due to strong R&D capabilities, global distribution networks, and premium product portfolios. These companies are leading innovation in precision nutrition, automation compatibility, and antibiotic-free formulations.

Tier 2 players including Nukamel, Volac, and Bewital Agri focus on high-performance, region-specific solutions, while Tier 3 manufacturers play a critical role in serving price-sensitive markets with cost-effective alternatives.

Outlook: From Generic Feeding to Strategic Herd Investment

As dairy and beef producers increasingly view early-life nutrition as a long-term investment rather than a cost center, calf milk replacers are evolving into highly specialized, data-driven solutions. By 2035, the market is expected to shift decisively toward customized formulations tailored by breed, climate, production system, and growth objectives.

Strategic partnerships between animal health companies, feed manufacturers, and dairy cooperatives are likely to accelerate, positioning calf milk replacers as a cornerstone of sustainable, high-efficiency livestock production worldwide.