The global Aerospace Lightning Strike Protection Market is poised for steady expansion, rising from USD 3.1 billion in 2025 to USD 5.5 billion by 2035, achieving a compound annual growth rate (CAGR) of 5.9% over the forecast period. This growth trajectory reflects a structurally resilient market underpinned by the accelerating adoption of composite airframe materials, increasing aircraft production rates, and tightening global aviation safety standards.

Rolling CAGR analysis across three overlapping five-year periods highlights the market’s stability and long-term reliability. The market is projected to grow from USD 3.1 billion to USD 4.1 billion between 2025 and 2030 at a rolling CAGR of approximately 5.8%, followed by expansion from USD 3.5 billion to USD 4.9 billion between 2027 and 2032 at around 6.0%. From 2030 to 2035, the market maintains momentum, advancing from USD 4.1 billion to USD 5.5 billion at roughly 6.1% CAGR. The consistency of these growth rates signals low volatility and a dependable, regulation-driven demand pattern.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-23272

Composite Airframes Reshaping Lightning Protection Requirements

The rapid shift toward carbon fiber reinforced polymer (CFRP) and hybrid composite structures in narrow-body, wide-body, regional, and next-generation aircraft is fundamentally transforming lightning strike protection strategies. Unlike traditional metallic airframes, composite materials lack natural electrical conductivity, increasing vulnerability to thermal and electrical damage during lightning events. As a result, aircraft manufacturers are embedding conductive meshes, expanded metal foils, and nano-enhanced coatings directly into fuselage, wing, nacelle, and tail structures.

By 2025, fixed-wing aircraft are expected to account for 72.0% of global market revenue, driven by strong commercial aircraft deliveries, business jet programs, and rising integration of composite-intensive structures. These platforms represent the highest concentration of advanced avionics and electrically sensitive systems, elevating the necessity for reliable lightning current dissipation pathways.

Line-Fit Installations Become the Industry Standard

Line-fit installations are projected to command 64.0% of total market share by 2025, reflecting the industry’s preference for embedding lightning strike protection solutions during aircraft manufacturing rather than post-delivery modification. Integrating conductive layers at the production stage delivers superior bonding integrity, predictable performance, and lower lifetime ownership costs.

Aircraft OEMs are increasingly co-curing expanded metal foils and conductive meshes within composite layups, enabling compliance with airworthiness certification standards while minimizing structural weight penalties. Rising global aircraft backlogs and production rate increases are further reinforcing the dominance of line-fit solutions.

Lightning Protection Applications Lead Market Demand

Within application segments, direct lightning protection systems dominate, holding an estimated 50.0% market share in 2025. Protecting flight-critical systems-including avionics, fuel tanks, flight control surfaces, and electrical power architecture-has become a non-negotiable design requirement.

The increasing electrification of onboard systems, including more-electric and hybrid-electric aircraft architectures, is intensifying the need for application-specific protection technologies. Advanced diverter strips, conductive surface treatments, and embedded grounding networks are now core design elements rather than optional enhancements.

Commercial Aviation Anchors Global Demand

Commercial aviation represents approximately 62% of total demand, supported by global fleet expansion, rising air passenger traffic, and mandatory compliance with stringent lightning protection and electromagnetic interference (EMI) standards. Military aviation contributes 28% of market value, driven by high-performance mission requirements, high-altitude operations, and sensitive payload protection. General aviation, accounting for 10%, is gaining traction due to growing use of business jets and regional aircraft with composite-rich structures.

Technology Evolution Shifting Market Value Dynamics

Material and system innovation is reshaping competitive positioning across the market. The transition from traditional heavy metal shielding to lightweight conductive meshes, graphene-enabled films, interwoven fiber architectures, and nano-coatings is delivering higher conductivity with minimal impact on structural flexibility and aircraft weight.

Manufacturers are deploying sensor-enhanced protection systems that enable real-time lightning event detection and predictive structural monitoring. Digital twin simulations and virtual strike modeling are accelerating certification cycles and shortening development timelines. Co-development partnerships between OEMs and material suppliers are becoming central to achieving customized, geometry-specific protection designs.

Regional Growth Accelerates in Asia and Strategic European Hubs

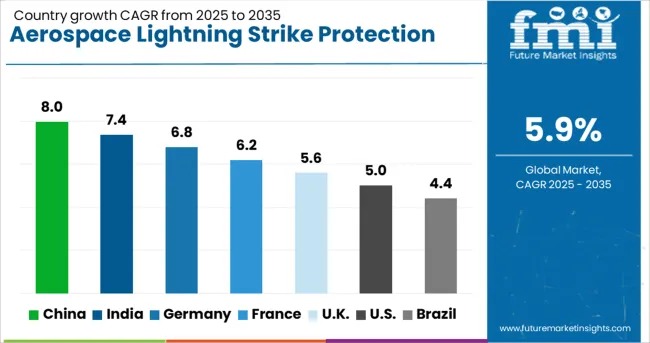

Growth remains geographically diversified, with strong momentum across Asia and Europe. China is projected to expand at an 8.0% CAGR, fueled by domestic aircraft manufacturing clusters and expanded use of conductive foils and films in composite fuselages. India follows at 7.4% CAGR, supported by indigenous aircraft programs and integration of lightning protection layers across new-generation airframes. Germany, with 6.8% CAGR, continues to lead innovation in carbon-based conductive prepregs and hybrid metal-fiber screening systems.

The United States, growing at 5.0% CAGR, benefits from strong OEM integration, regulatory updates, and defense-driven demand. The United Kingdom is advancing at 5.6% CAGR, with rising adoption across fixed-wing, rotorcraft, and advanced air mobility platforms.

Personalize Your Experience: Ask for Customization to Meet Your Requirements

https://www.futuremarketinsights.com/customization-available/rep-gb-23272

Certification Complexity Remains the Primary Market Constraint

Despite strong fundamentals, certification and retrofit complexity continue to constrain full-scale adoption in legacy fleets. Full-airframe lightning testing, high-voltage simulation, and compliance documentation remain cost-intensive and time-consuming. Structural modification requirements and limited field repairability can delay retrofit timelines, particularly among cost-sensitive regional operators. However, these barriers are steadily being mitigated through material advancements and modular system designs.

Competitive Landscape Strengthened by Materials Innovation and OEM Collaboration

Market competition is intensifying as suppliers invest in next-generation technologies and OEM partnerships. Key industry participants include LORD Corporation (Parker Hannifin), Henkel, Arconic, Hollingsworth & Vose Company, Wallner Tooling/EXPAC, Lightning Diversion System, Boeing, and Dexmet Corporation.

Over the last two years, the market has witnessed the introduction of lighter, composite-compatible conductive systems, expansion of retrofit programs, and deployment of smart, sensor-enabled protection architectures. These developments are reinforcing the strategic role of lightning strike protection as a cornerstone of aircraft safety, durability, and regulatory compliance.

Why Choose FMI: Empowering Decisions that Drive Real-World Outcomes: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.