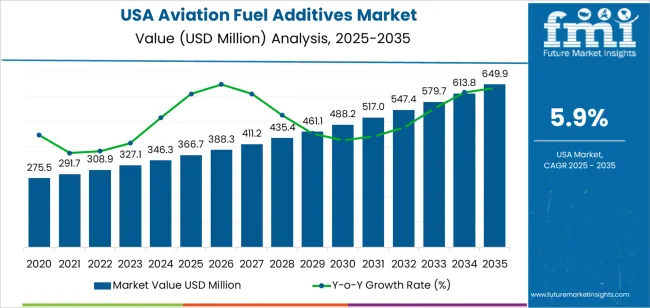

The United States aviation fuel additives market is projected to grow from an estimated USD 366.7 million in 2025 to approximately USD 649.9 million by 2035, reflecting robust industry confidence and continued aviation expansion. This growth underscores a pivotal shift toward advanced fuel performance technologies and strategic business expansions by both established and new players aiming to capture emerging opportunities in a rapidly evolving market landscape.

As the United States continues to see heightened air travel demand, commercial airline activity, and defense aviation operations, the role of fuel additives in enhancing performance, safety, and environmental compliance has never been more critical. Aviation fuel additives improve combustion efficiency, prevent corrosion, inhibit ice formation, and protect fuel systems from microbial growth—functions essential for modern aircraft performance across diverse climatic and operational conditions.

Market Dynamics: Innovation Meets Demand

The anticipated market growth is underpinned by several core dynamics. Increasing air travel, fleet modernization, stringent environmental regulations, and the rise of sustainable aviation fuels have all contributed to stronger demand for high-performance additive solutions. With jet fuel consumption steadily increasing, airlines and fuel suppliers are focusing on additives that not only boost performance but also align with environmental and regulatory mandates for cleaner aviation operations.

Industry leaders such as BASF SE, Innospec Inc., Shell plc, and Chevron Oronite Company LLC remain at the forefront of the U.S. aviation fuel additives market. These established manufacturers have long histories of delivering high-quality additive solutions that enhance fuel stability, protect engine components, and ensure compliance with rigorous aviation standards. Their broad product portfolios span corrosion inhibitors, dispersants, antioxidants, anti-icing agents, and other specialized additive chemistries designed to meet the complex needs of commercial, military, and private aviation sectors.

Yet, it is not just the stalwarts shaping the future of this space. A new wave of manufacturers is leveraging cutting-edge technologies and innovative additive formulations to challenge traditional approaches and unlock fresh avenues for business expansion. These emerging players are investing in multifunctional additive packages that combine multiple performance benefits in a single solution—streamlining fuel management and reducing operational complexity for airlines and fuel distributors alike.

Technological Innovations and Trends

One of the most notable trends in the market today is the development of advanced additive technologies that support next-generation fuels, including biofuels and synthetic aviation fuels. As the industry transitions toward lower-emission fuel alternatives, specialized additive packages are critical to ensuring compatibility, thermal stability, and performance integrity in these newer fuel formulations.

Emerging manufacturers are increasingly focusing on tailored additive solutions for sustainable aviation fuels (SAFs), which present unique chemical properties and performance requirements compared to conventional jet fuel. By innovating across fuel chemistry and additive science, these new entrants are helping stakeholders navigate the complexities of SAF adoption while contributing to broader decarbonization goals.

In addition to enabling SAF compatibility, additive developers are emphasizing multifunctionality. Modern formulations are designed to simultaneously address fuel stability, corrosion protection, microbial inhibition, and combustion optimization—driven by the need for operational efficiency and cost-effective fuel management.

Collaborative Growth: Partnerships and Strategic Alliances

Collaboration is playing an essential role in accelerating market growth. Established players are increasingly partnering with technology startups, research institutions, and global aerospace firms to co-develop next-generation additive solutions and bring them to market at scale. These strategic alliances combine deep industry expertise with agile innovation models, allowing partners to respond swiftly to evolving market demands and regulatory landscapes.

Such cooperation is not limited to product development. Many companies are also working together on pilot programs, certification initiatives, and supply chain optimization efforts that ensure additive technologies are efficiently integrated into aviation fuel infrastructure across major hubs in the United States.

Industry Outlook and Future Prospects

As the aviation sector continues its recovery and long-term expansion, the U.S. aviation fuel additives market is poised for sustained growth. The increasing complexity of aircraft engines, demands for higher fuel efficiency, and commitments to reduce emissions create fertile ground for additive innovation. Both established manufacturers and emerging challengers are actively pursuing new technologies, formulating advanced additive chemistries, and exploring commercial strategies to expand their footprint in the U.S. market.

For established companies, the focus remains on enhancing product performance, maintaining quality certifications, and offering reliable additive supply to large commercial and defense operators. For newer entrants, success hinges on differentiating through technology, agility, and the ability to address niche applications—especially in sustainable fuels and multifunctional additive packages.