The raw, fresh, and frozen dog food market is expected to stand out across the coming decade, driven by rising pet humanization, heightened awareness of canine health, and a growing preference for minimally processed, nutritious diets. Dog owners are increasingly treating pets as family members, prompting a shift away from conventional kibble toward food products that more closely resemble historical, biologically appropriate diets.

This evolution in consumer mindset is reshaping the premium pet food landscape. Raw, fresh, and frozen formulations made with natural proteins, vegetables, and functional ingredients are gaining acceptance as pet parents seek better digestion, improved immunity, and overall wellness for their dogs. The market is also benefiting from strong innovation in cold-chain logistics, packaging, and direct-to-consumer delivery models.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-12024

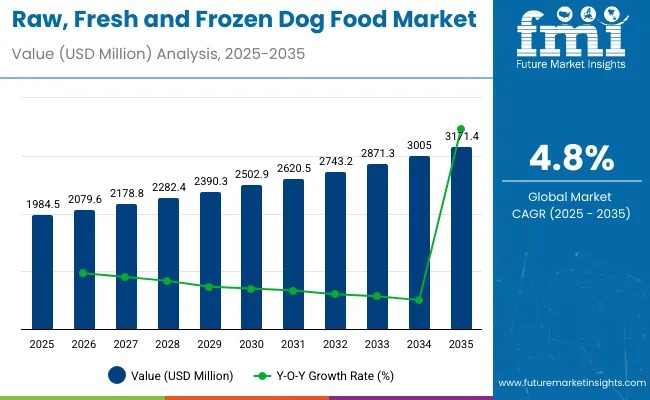

According to industry estimates, the global raw, fresh, and frozen dog food market was valued at USD 1,984.5 million in 2025 and is projected to reach USD 3,171.4 million by 2035, expanding at a steady CAGR of 4.8% over the forecast period. Growth is supported by premiumization trends, expanding e-commerce penetration, and rising acceptance of veterinarian-backed fresh feeding programs.

Trade Landscape Reflects Premiumization of Pet Nutrition

Global trade in raw, fresh, and frozen dog food continues to expand as awareness around pet nutrition rises. Countries with advanced manufacturing capabilities and strict food safety standards dominate exports. The United States, Canada, Germany, and the Netherlands lead global supply, supported by strong cold-chain infrastructure and rigorous quality control.

On the demand side, imports are rising across Japan, South Korea, Australia, and the UAE, where pet ownership is increasing faster than domestic production of premium pet food. Urban lifestyles, higher disposable incomes, and rapid growth of online pet retail platforms are making imported, high-quality dog food more accessible to consumers.

Per Capita Spending Highlights Regional Maturity Gaps

Spending patterns vary widely by region. In developed markets such as the U.S., Canada, Germany, and the UK, per capita spending on raw and fresh dog food remains high, supported by subscription-based services and direct-to-consumer brands offering human-grade meals. Products emphasizing transparency, limited ingredients, and functional health benefits resonate strongly with informed pet owners.

In contrast, emerging markets including Brazil, India, and parts of Southeast Asia are witnessing gradual adoption. While per capita spending is lower, growth momentum is building due to urbanization, increasing awareness of pet health, and the entry of local startups and imported premium brands.

Regional Market Dynamics

North America holds the largest share of the global market, driven by high pet ownership rates and strong demand for premium, additive-free products. Well-developed distribution networks, including pet specialty stores and online channels, support market expansion.

Europe shows consistent growth, led by Germany, France, and the UK, where interest in BARF (Biologically Appropriate Raw Food) diets is rising. Strict regulatory standards across the region enhance consumer trust and encourage manufacturers to maintain high-quality benchmarks.

Asia-Pacific is expected to be the fastest-growing region through 2035. Improving disposable incomes, urbanization, and Western pet care influences are accelerating demand in China, Japan, and Australia. Consumers are increasingly willing to invest in premium fresh and frozen products that align with modern pet wellness trends.

Challenges Balanced by Strong Opportunities

Despite strong growth prospects, the market faces challenges related to short shelf life, cold-chain dependency, and microbial safety concerns. Raw and frozen products require strict temperature control, increasing logistics costs and limiting retail shelf availability. Additionally, concerns around pathogens such as Salmonella and Listeria have heightened regulatory scrutiny.

However, opportunities outweigh these constraints. Key growth drivers include:

- Rising pet humanization and willingness to pay for premium nutrition

- Demand for nutritional transparency and clean-label products

- Expansion of subscription-based and customized meal plans

Advancements in vacuum sealing, freeze-drying, and sustainable protein sourcing are improving shelf life and safety, enabling broader market penetration.

Market Shifts and Future Outlook

Between 2020 and 2024, the market benefited from increased pet adoption and higher spending on premium pet care during the pandemic. From 2025 to 2035, growth will be shaped by personalized nutrition, nutrigenomics-driven diets, and AI-enabled feeding plans. Innovations such as single-serve frozen portions, functional ingredients, and smart packaging are expected to define the next phase of competition.

Segmentation Trends Strengthen Market Value

Frozen dog food dominates the market with 61.5% share in 2025, owing to extended shelf life, balanced nutrition, and enhanced safety. Small breed formulations account for 56.8% of demand, reflecting urban pet ownership trends and the need for portion-controlled, digestible diets.

Competitive Landscape Remains Innovation-Driven

The market features a mix of established brands and agile D2C players investing heavily in veterinary-backed formulations, sustainable sourcing, and cold-chain logistics. Leading companies continue to differentiate through customization, functional health benefits, and subscription convenience, while boutique brands innovate with clean-label and novel protein offerings.