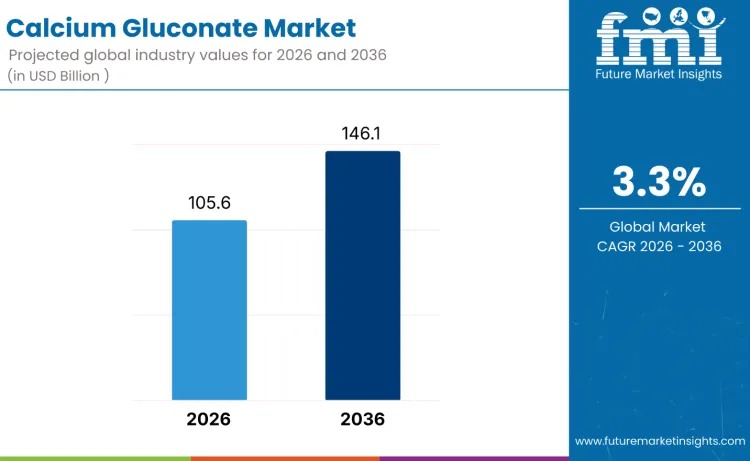

The global calcium gluconate market is entering a steady expansion phase as healthcare systems, food manufacturers, and nutraceutical brands increasingly prioritize safe, bioavailable calcium sources. Valued at USD 105.6 billion in 2026, the market is forecast to reach USD 146.1 billion by 2036, reflecting a consistent 3.3% compound annual growth rate. This growth trajectory mirrors rising calcium deficiency worldwide, greater awareness of bone and cardiovascular health, and expanding fortification initiatives across both developed and emerging economies.

Pharmaceutical applications continue to anchor demand, with calcium gluconate widely used in intravenous therapies for hypocalcemia, cardiac stabilization, and magnesium toxicity management. Its favorable safety profile, high solubility, and predictable absorption make it a preferred calcium salt in clinical and emergency care settings. At the same time, food and beverage manufacturers are adopting calcium gluconate for dairy fortification, plant-based beverages, functional drinks, and infant nutrition products due to its clean-label positioning and allergen-free nature.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-1275

Beyond pharmaceuticals, the nutraceutical segment is expanding steadily as consumers embrace preventive wellness. Demand is rising for bone health supplements, prenatal formulations, and geriatric nutrition products, particularly in markets with aging populations. The shift toward vegan and lactose-free diets further strengthens adoption, positioning calcium gluconate as a non-dairy, highly bioavailable alternative to traditional calcium sources. These trends are reinforcing long-term consumption across supplements, fortified foods, and medical nutrition.

Quick Stats: Calcium Gluconate Market (2026–2036)

- Market Value (2026): USD 105.6 billion

- Forecast Value (2036): USD 146.1 billion

- Forecast CAGR: 3.3%

- Leading Grade: Pharmaceutical grade

- Leading Application: Pharmaceuticals

- Key Growth Regions: India, USA, China

From a segmentation perspective, pharmaceutical-grade calcium gluconate accounts for approximately 40% of global demand, making it the dominant grade segment. This reflects its extensive use in IV therapies, electrolyte correction, and high-purity supplement formulations. Food-grade calcium gluconate supports beverage fortification, dairy alternatives, cereals, and functional snacks, while technical-grade material serves agriculture, animal feed, and industrial applications where purity thresholds are lower.

In terms of form, powder remains the preferred format, representing nearly 62% of global demand. Powdered calcium gluconate offers superior stability, longer shelf life, and ease of incorporation into tablets, capsules, functional foods, and feed blends. Liquid forms are widely used in beverage fortification and syrup formulations, while injectable forms are essential for hospital-based infusion therapies and emergency care.

Application-wise, pharmaceuticals lead with around 40% share of total demand. Rising IV therapy usage, aging populations, and increasing diagnosis of calcium-related disorders continue to support this dominance. Food and beverage applications are expanding steadily through fortified dairy, plant-based drinks, and ready-to-drink nutrition. Nutraceuticals benefit from strong growth in bone health, maternal care, and senior nutrition, while agriculture and animal feed applications contribute incremental volume through mineral enrichment and livestock health programs.

Despite its positive outlook, the calcium gluconate market faces challenges. Competition from lower-cost substitutes such as calcium carbonate and calcium citrate pressures pricing, particularly in food and supplement applications. Strict regulatory requirements for pharmaceutical-grade material add complexity, increasing compliance costs and limiting rapid capacity expansion. However, these constraints are balanced by emerging opportunities in enhanced absorption formulations, microencapsulation technologies, and vegan-certified ingredient lines. New delivery formats—including gummies, effervescent powders, and liquid shots—are expected to broaden consumer adoption through 2036.

Geographically, demand growth varies by country. India leads with a 5.1% CAGR, driven by expanding hospital usage, rapid supplement adoption, and government-backed food fortification programs. The United States follows at 4.8%, supported by strong clinical demand and clean-label fortification in plant-based beverages. China records 4.0% growth as fortified foods and injectable therapies scale nationwide, while the UK grows at 4.5% on the back of dietary supplements and nutrient enrichment initiatives. Japan’s mature healthcare sector delivers stable growth of around 2.5%, supported by an aging population and consistent pharmaceutical consumption.

The competitive landscape remains focused on purity assurance, regulatory compliance, and supply reliability. Leading players including BASF SE, Koninklijke DSM N.V., Jungbunzlauer Suisse AG, Roquette Frères, GlaxoSmithKline plc, and Global Calcium Pvt Ltd continue to strengthen their positions through high-quality production, diversified calcium salt portfolios, and close collaboration with pharmaceutical and nutrition brands. As preventive healthcare and fortified nutrition gain further momentum, calcium gluconate is expected to retain its role as a cornerstone ingredient across medical, food, and nutraceutical applications worldwide.