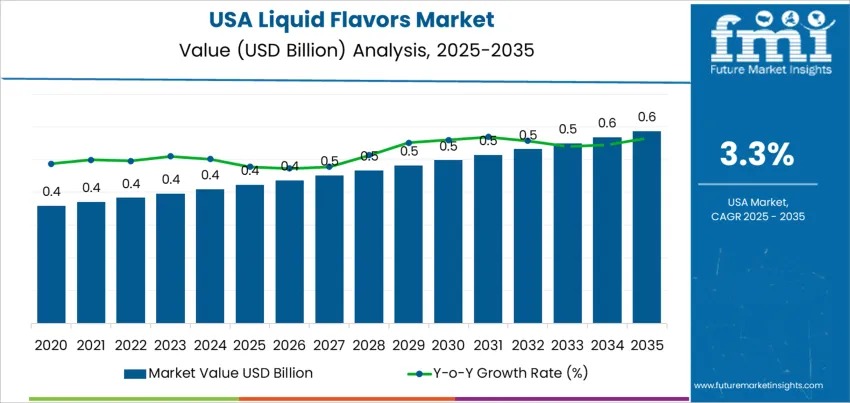

The demand for liquid flavors in the USA continues to expand steadily, supported by evolving consumer taste expectations and formulation-driven innovation across food, beverage, and wellness categories. Valued at USD 0.4 billion in 2025, the USA liquid flavors market is forecast to reach USD 0.6 billion by 2035, reflecting a compound annual growth rate (CAGR) of 3.3% over the decade. While the category shows signs of maturity in traditional applications, targeted growth in clean-label, functional, and plant-based segments is sustaining long-term demand.

Liquid flavor concentrates remain integral to modern food manufacturing due to their ability to deliver consistent taste, easy dispersion, and formulation flexibility. Rising usage across packaged foods, functional beverages, dairy products, bakery fillings, and confectionery highlights their role in maintaining sensory quality while supporting reduced sugar, fortified, and reformulated product lines.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-29517

Market dynamics increasingly reflect the shift toward recognizable ingredients and reduced artificial additives. Manufacturers are prioritizing natural and organic liquid flavors to align with clean-label positioning, particularly in ready-to-drink beverages, flavored waters, protein shakes, and plant-based dairy alternatives. These systems also address technical challenges such as sweetness modulation, off-note masking in plant proteins, and flavor stability across refrigerated and shelf-stable formats.

From a lifecycle perspective, the U.S. liquid flavors industry is approaching saturation in legacy segments such as carbonated soft drinks, conventional confectionery, and mainstream dairy. High penetration levels and established supplier relationships limit rapid volume expansion. However, innovation-led niches continue to offset maturity pressures. Functional beverages, nutraceutical syrups, low-sugar formulations, and premium café-style drinks are driving replacement demand and incremental value growth.

Quick Stats: USA Liquid Flavors Demand

- Market Value (2025): USD 0.4 billion

- Forecast Value (2035): USD 0.6 billion

- Forecast CAGR (2025–2035): 3.3%

- Leading Product Type: Organic liquid flavors

- High-Growth Regions: West USA, South USA, Northeast USA

Product and Application Trends Shaping Demand

Organic liquid flavors account for an estimated 50% share, reflecting strong consumer alignment with USDA-certified inputs and transparent labeling. Artificial flavors retain a 45% share, primarily due to cost efficiency and shelf-life advantages in mass-market beverages and candies. Natural flavors represent a smaller but strategic 5%, concentrated in premium and health-oriented products where sourcing constraints and pricing remain key challenges.

Beverages dominate application demand with a 39% share, driven by frequent reformulation in flavored water, energy drinks, teas, and nutrition beverages. Pharmaceuticals follow at 20%, where liquid flavors improve palatability and patient compliance. Personal care and cosmetics contribute 19%, while food applications such as sauces, bakery fillings, and dairy alternatives hold 12%. Animal feed accounts for the remaining 10%, focused on palatability enhancement.

From a formulation standpoint, oil-soluble liquid flavors lead with 40%, favored in fat-based foods, nutraceutical oils, and lip care. Alcohol-based formats represent 36%, valued for aroma retention and extract concentration, while water-soluble flavors hold 24%, supporting instant beverage mixes and rapid dispersion systems.

Regional Performance Highlights

Regional adoption patterns reflect differences in manufacturing density, consumer preferences, and innovation intensity.

- West USA leads with a 3.8% CAGR, driven by beverage startups, functional drinks, and organic-certified formulations in states such as California and Washington.

- South USA follows at 3.4% CAGR, supported by large-scale beverage, confectionery, and private-label production in Texas, Georgia, and Florida.

- Northeast USA records 3.1% CAGR, shaped by premium beverage launches, café culture, and seasonal bakery innovation.

- Midwest USA, growing at 2.7% CAGR, reflects stable demand from mainstream dairy, convenience foods, and nationally distributed brands emphasizing consistency and shelf stability.

Competitive Landscape and Strategic Focus

The U.S. liquid flavors market is moderately consolidated, with competition centered on regulatory compliance, formulation expertise, and scalable supply capabilities. International Flavors & Fragrances Inc. leads with an estimated 30.3% share, supported by extensive sensory libraries and long-term partnerships with multinational food and beverage brands.

Other prominent suppliers include Gold Coast Ingredients, known for customized formulations; Nature’s Flavors, Inc., specializing in organic and clean-label solutions; Takasago International Corporation, leveraging aroma chemistry and regional innovation hubs; and McCormick & Company, Inc., which integrates spice-derived flavor systems into both sweet and savory applications. Across the board, supplier strategies emphasize documentation-ready ingredients, stability improvements, and support for reduced-sugar and plant-based reformulation programs.

Outlook

Looking ahead, growth in the USA liquid flavors market will remain incremental but resilient. While saturation limits rapid expansion in traditional categories, sustained innovation in health-focused beverages, functional nutrition, and clean-label foods will continue to create demand for advanced liquid flavor systems. As taste expectations evolve alongside wellness and transparency trends, liquid flavors will remain a critical component of product differentiation in the U.S. food and beverage industry.