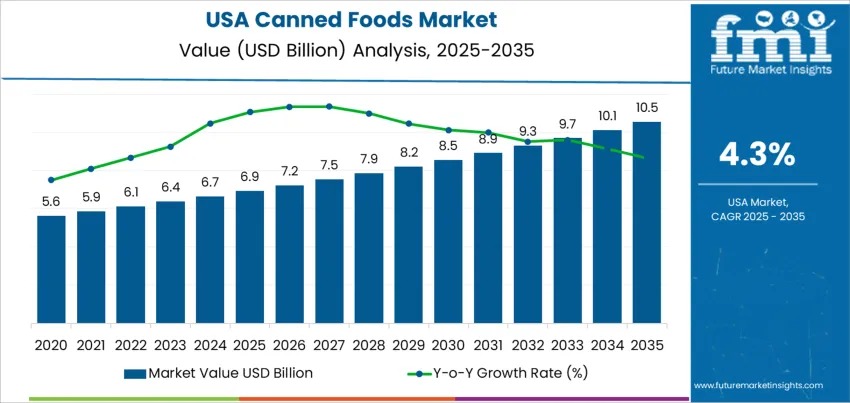

The demand for canned foods in the USA continues to demonstrate structural resilience, supported by affordability, long shelf life, and consistent relevance across household, institutional, and emergency-preparedness use cases. Valued at USD 6.9 billion in 2025, the USA canned foods market is forecast to reach USD 10.5 billion by 2035, expanding at a compound annual growth rate (CAGR) of 4.3%. Growth is anchored in rising consumption of convenient packaged foods, steady penetration in budget-focused retail, and improvements in processing technologies that enhance nutrient retention and sensory quality.

Canned foods remain a dependable category during periods of economic uncertainty, when households prioritize price stability, reduced food waste, and pantry stocking. Products such as canned fruits, vegetables, beans, soups, and ready meals deliver predictable nutrition and storage efficiency without refrigeration. These characteristics sustain demand across diverse income groups and geographic regions, reinforcing the category’s role as a core staple in American food consumption.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-29502

Convenience, Stability, and Reformulation Drive Category Growth

The sustained relevance of canned foods is closely linked to evolving consumer lifestyles. Busy households, single-person dwellings, students, and older consumers continue to favor products requiring minimal preparation. At the same time, manufacturers are actively addressing historic perception challenges through clean-label positioning, reduced sodium and sugar formulations, and improved retort processes that preserve flavor, color, and texture.

Canned fruits and vegetables represent the leading product type, benefiting from high household usage frequency and broad availability through grocery chains, club stores, and discount retailers. Stable pricing and year-round accessibility make these products attractive alternatives to fresh produce during seasonal price fluctuations or supply disruptions.

Quick Market Snapshot – USA Canned Foods Demand

- Market value (2025): USD 6.9 billion

- Forecast value (2035): USD 10.5 billion

- Forecast CAGR (2025–2035): 4.3%

- Leading product type: Canned fruits and vegetables

- Key regions: West USA, South USA, Northeast USA

Product, Label, and Channel Dynamics Shape Demand

By product category, canned fruits and vegetables account for approximately 37.5% of demand, supported by household cooking versatility and institutional use. Canned ready meals follow at 31.0%, reflecting demand for heat-and-serve options that support predictable meal planning. Beans, soups, sauces, and broths together account for 28.0%, reinforcing the pantry-staple nature of the category, while canned meat and seafood hold a smaller 3.5% share due to selective purchasing behavior.

From a labeling perspective, organic canned foods represent about 54.0% of demand, driven by consumer preference for ingredient transparency and reduced additives. Conventional products retain a 46.0% share, remaining essential for value-driven buyers and large-scale procurement programs. Advancements in canning technology continue to narrow the perceived quality gap between organic and conventional offerings.

Distribution remains dominated by supermarkets and hypermarkets (42.0%), which support bulk purchasing and high product rotation. E-commerce channels account for 33.0%, benefiting from subscription models, bundled deliveries, and low spoilage risk during transport. Other physical channels, including institutional supply, contribute 19.0%, while convenience stores serve niche and emergency needs.

Regional Demand Patterns Highlight Structural Strength

Demand is concentrated in the West, South, and Northeast, supported by large distribution networks and established reliance on ready-to-eat staples. The West USA leads growth at 4.9% CAGR, driven by diverse cuisine preferences, organic product uptake, and emergency-readiness habits. The South USA follows at 4.4% CAGR, supported by value-focused purchasing, larger household sizes, and integration of canned ingredients into regional cooking styles.

The Northeast USA grows at 3.9% CAGR, where convenience-oriented consumption in urban centers supports demand for soups, broths, and ready meals, particularly during winter months. The Midwest USA records a steady 3.4% CAGR, reflecting traditional consumption patterns, strong private-label manufacturing, and club-store driven volumes.

Competitive Landscape Anchored in Scale and Reliability

The USA canned foods market remains moderately consolidated, with competition centered on cost-efficient production, national distribution reach, and consistent product availability. Conagra Brands, Inc. holds an estimated 31.8% share, supported by a broad portfolio of canned meals, vegetables, and beans distributed across major retail formats. Campbell Soup Company maintains strong brand loyalty through its canned soups and meal-based offerings, while Del Monte Foods, Inc. is a key supplier of canned fruits and vegetables to both retail and institutional buyers.

Kraft Heinz Company participates through sauces and meal solutions that combine shelf stability with familiar flavor profiles, and Bonduelle SA serves premium and specialty segments with imported canned vegetables and legumes. Across the competitive landscape, priorities include recyclable metal packaging, BPA-free linings, private-label expansion, and regional produce sourcing initiatives.

Outlook: A Resilient, Evolving Staple Category

While competition from fresh and frozen foods moderates expansion in certain segments, canned foods continue to deliver unmatched advantages in shelf life, affordability, and waste reduction. Ongoing reformulation, sustainable packaging investments, and product innovation are expected to sustain demand through 2035. As consumers balance convenience, cost control, and nutrition, canned foods remain firmly positioned as a resilient cornerstone of the U.S. food system.

Key Players in USA Canned Foods Demand

Conagra Brands, Inc. | Campbell Soup Company | Del Monte Foods, Inc. | Kraft Heinz Company | Bonduelle SA