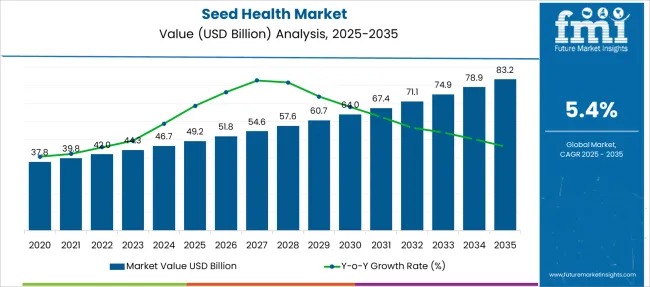

The global seed health market is entering a decade of sustained expansion as agriculture faces mounting pressure to deliver higher yields, resilient crops, and environmentally responsible practices. Valued at USD 49.2 billion in 2025, the market is projected to reach USD 83.2 billion by 2035, registering a compound annual growth rate (CAGR) of 5.4% over the forecast period. This growth reflects the rising strategic importance of seed health solutions as foundational inputs for global food security.

Seed health products play a critical role in ensuring disease-free germination, protecting crops from soil- and seed-borne pathogens, and enhancing early-stage plant vigor. With climate variability, declining arable land, and stricter regulations on chemical inputs reshaping farming systems worldwide, seed health technologies are increasingly viewed as cost-effective, high-impact interventions that deliver both agronomic and environmental benefits.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-11681

At the core of this momentum is a structural shift toward sustainable agriculture. Farmers, regulators, and food companies are aligning around practices that reduce chemical dependence while maintaining productivity. Advances in seed treatment formulations, precision delivery mechanisms, and biological innovations are accelerating adoption across both developed and emerging agricultural economies.

Market Snapshot Highlights

In 2025, the seed health market is characterized by strong segmental concentration and regional diversity. Key metrics underline the sector’s scale and stability:

- Industry value (2025): USD 49.2 billion

- Forecast value (2035): USD 83.2 billion

- Forecast CAGR (2025–2035): 5.4%

- Leading segment: Biological seed treatment, accounting for 48.6% of revenue

- High-growth regions: North America, Asia-Pacific, and Europe

Biological Seed Treatments Lead the Market

Biological seed treatments represent the largest and fastest-growing segment, driven by regulatory restrictions on synthetic chemicals and rising demand for residue-free food. By 2025, biological solutions are expected to contribute 48.6% of total market revenue, reflecting their central role in modern agronomy.

These treatments leverage beneficial microbes and naturally derived compounds to strengthen plant immunity, improve nutrient uptake, and enhance resistance to soil-borne diseases. Unlike conventional chemical treatments, biological options support soil health and align with integrated pest management systems, making them increasingly attractive to both large-scale commercial farms and organic producers.

As sustainability becomes embedded in agricultural policy frameworks and supply chain standards, biological seed treatments are transitioning from niche alternatives to mainstream solutions.

Grains Dominate Crop Type Demand

By crop type, grains account for an estimated 44.2% of total market revenue in 2025, maintaining their leadership position. Wheat, rice, and maize remain the backbone of global food systems, and their large-scale cultivation makes them particularly vulnerable to seed-borne pathogens and early-stage fungal infections.

The economic significance of grain exports, combined with climate-induced stress and yield volatility, has intensified the need for robust seed health interventions. As growers adopt advanced agronomic practices to safeguard productivity, demand for grain-specific seed health solutions continues to strengthen.

B2C Distribution Gains Momentum

From a distribution perspective, the B2C channel holds around 42.5% of market revenue in 2025, emerging as the dominant route to market. Direct purchasing by individual farmers, smallholder growers, and local distributors is increasing, supported by improved digital connectivity and farmer-focused e-commerce platforms.

Mobile agriculture applications, online advisory tools, and transparent pricing models are reshaping purchasing behavior. As convenience, customization, and brand trust become decisive factors, the B2C model is expected to play an even larger role in the seed health value chain.

Regional Dynamics Shape Growth Trajectories

North America continues to lead the global seed health market, supported by advanced seed testing infrastructure and sustained investment in research and development. Many of the world’s leading seed health companies are headquartered in the region, driving continuous innovation and global technology transfer.

Europe represents an attractive growth market, fueled by strong demand for organic food, stringent environmental regulations, and a highly developed agricultural ecosystem. Meanwhile, Asia-Pacific is witnessing rapid expansion due to rising food safety concerns, increasing adoption of sustainable farming practices, and growing awareness of seed-borne disease management among farmers.

Competitive Landscape and Outlook

The competitive landscape includes global and regional players such as BASF, Syngenta, Bayer, Monsanto, DuPont, Sumitomo Chemical, Novozymes, Nufarm, and Valent USA, among others. Companies are prioritizing innovation, biological product development, and expanded distribution networks to strengthen their market positions.

Looking ahead, the seed health market is poised to benefit from increased seed substitution rates, wider adoption of hybrid and genetically improved seeds, and growing regulatory support for non-chemical crop protection. As agriculture balances productivity with sustainability, seed health solutions will remain a critical, low-cost lever for ensuring resilient and profitable farming systems worldwide.