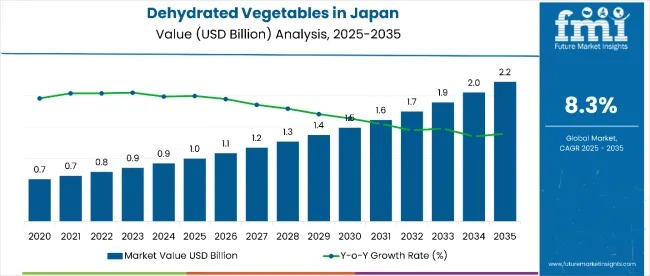

Sales of dehydrated vegetables in Japan are entering a decade of sustained expansion, supported by changing food habits, demographic shifts, and rising emphasis on convenience and nutrition. The market is estimated at USD 1 billion in 2025 and is projected to reach USD 2.2 billion by 2035, reflecting a robust compound annual growth rate (CAGR) of approximately 8.3% over the forecast period.

Dehydrated vegetables are increasingly positioned as a practical alternative to fresh produce, offering extended shelf life, reduced food waste, and ease of storage. Their adoption spans households, food manufacturers, and food service operators, aligning well with Japan’s fast-paced urban lifestyles and long-standing emergency preparedness culture.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-18264

Demand momentum is further reinforced by rising per capita consumption across diverse age groups. Health-conscious consumers value dehydrated vegetables for nutrient retention and portion control, while manufacturers and restaurants benefit from year-round availability and consistent quality. By 2025, average per capita consumption in leading regions such as Kanto, Chubu, and Kinki ranges between 2.1 kg and 2.8 kg, with projections rising sharply to 4.5–6.2 kg by 2035.

Market Size, Growth, and Consumption Outlook

Japan’s dehydrated vegetable market growth is underpinned by structural changes in food consumption. Improvements in processing technologies have narrowed the price gap with fresh vegetables. By 2025, dehydrated vegetables are priced only 25–30% higher than fresh alternatives, compared to significantly wider gaps in previous years, making them increasingly accessible to middle-income households.

Kanto remains the largest consumption hub and is expected to generate USD 795.4 million in sales by 2035, followed by Chubu (USD 567.1 million) and Kinki (USD 476.2 million). Emerging regions such as Kyushu & Okinawa (USD 272.4 million) and Tohoku (USD 155.7 million) are closing the gap, driven by lifestyle modernization and expanding retail penetration.

Segment Insights: Form and End Use

By form, powder and granules dominate with a 36% share in 2025, reflecting their versatility and ease of integration across applications. These formats are widely used for seasoning, soups, sauces, and functional foods, appealing to both households and professional kitchens.

Other forms continue to serve targeted needs:

- Minced and chopped formats support industrial food manufacturing where texture retention is required.

- Flakes provide visual appeal in snacks and specialty foods.

- Slices and cubes cater to premium and presentation-sensitive culinary applications.

By end use, food manufacturers account for 52% of total demand, making them the single largest consumption segment. Dehydrated vegetables are extensively used in snacks and savory products, soups, sauces, and infant foods, where consistency and nutritional density are critical.

Food service operators represent around 28% of consumption, driven by restaurants, hotels, and institutional catering seeking storage efficiency and cost stability. Retail channels, accounting for approximately 20%, are expanding rapidly through supermarkets, specialty stores, and online platforms offering convenient pack sizes.

Regional Growth Dynamics

While Kanto leads in absolute volume, the fastest growth is expected in emerging regions. Between 2025 and 2035:

- Tohoku is forecast to grow at a 9.2% CAGR,

- Kyushu & Okinawa at 8.8%,

- Rest of Japan at 8.5%.

These regions benefit from lower baseline consumption, increasing urbanization, and the integration of convenience foods into traditional cooking practices. In Tohoku, per capita consumption is projected to rise from 1.8 kg in 2025 to 4.1 kg by 2035, while Kyushu & Okinawa are expected to increase from 2.1 kg to 4.6 kg over the same period.

Competitive Landscape and Strategic Moves

Japan’s dehydrated vegetable sector is characterized by a mix of established food processors and specialized ingredient suppliers. Companies such as TOMIZ, MIKASA, OYAOYA, Osawa, and Kirishima Natural Foods emphasize quality consistency, nutritional retention, and application-specific product development. Their strategies increasingly focus on premiumization, organic offerings, and region-specific flavor profiles.

International participants and trading firms add scale and supply chain efficiency, particularly for commercial customers requiring reliable volumes. A notable development shaping the competitive environment occurred in May 2025, when Toyota Tsusho Foods Corporation acquired all shares of Mitsui & Co. Agri Foods Ltd. This move strengthens Toyota Tsusho Foods’ footprint in agricultural processing, including frozen and dried vegetables, and highlights ongoing consolidation in Japan’s food ingredient sector.

Outlook

Looking ahead, Japan’s dehydrated vegetable market is poised for sustained growth as convenience, health, and food security considerations converge. With rising per capita consumption, expanding regional adoption, and continued investment in processing and distribution, dehydrated vegetables are transitioning from niche ingredients to essential components of Japan’s modern food ecosystem.