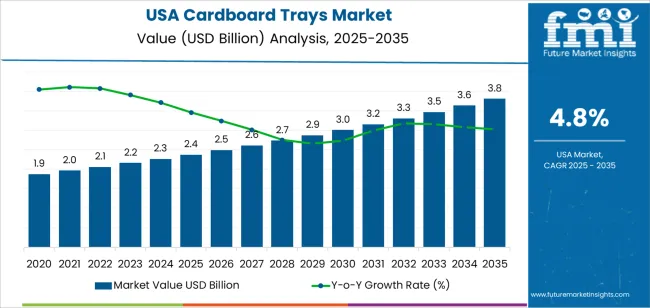

The United States cardboard trays market is experiencing a pivotal transformation, marked by robust growth, rapid technological adoption, and strategic expansion among both long-standing industry leaders and emerging manufacturers. As sustainability and efficiency become core drivers of modern packaging demand, cardboard trays are emerging as a preferred solution across multiple end-use sectors including food & beverage, retail, agriculture, personal care, and pharmaceuticals.

With the market’s valuation set to grow substantially over the next decade, industry pioneers and new entrants alike are seizing opportunities to innovate, differentiate, and scale operations across a diverse range of applications. This surge is propelled by a combination of environmental commitment, consumer expectations for eco-friendly packaging, and the logistical advantages cardboard trays offer in an increasingly digital commerce world.

Market Dynamics: Sustainability Meets Practicality

The United States cardboard trays market is forecasted to grow steadily through 2035, driven by a rising preference for packaging solutions that balance sustainability with performance. As brands seek materials that reduce reliance on plastics and align with circular economy goals, cardboard trays provide an attractive alternative thanks to their recyclability, biodegradability, and cost-efficiency. This trend is resonating with environmentally conscious consumers and businesses looking to enhance brand appeal while meeting legislative and retailer sustainability standards.

At the same time, the rapid expansion of e-commerce and demand for fresh food deliveries is escalating the need for reliable, sturdy packaging formats capable of protecting products during transit. Cardboard trays offer the ideal combination of light weight, durability, and adaptability, making them indispensable for online retail operations and distribution centers.

Leading Manufacturers Champion Innovation and Expansion

A cadre of established players remains at the forefront of the U.S. cardboard trays market, each leveraging deep industry expertise and broad manufacturing capabilities to meet evolving demand. Key companies — including Smurfit Kappa Group, Mondi Group, DS Smith Plc, WestRock Company, and International Paper Company — continue to drive growth through strategic investments in sustainable product portfolios and cutting-edge manufacturing technologies.

These organizations are adopting advanced printing solutions, improved die-cutting processes, and design innovations that enhance tray functionality, branding potential, and integration with automated packaging systems. Such advancements not only improve operational efficiencies but also allow brands to deliver compelling unboxing experiences that reinforce product identity and consumer loyalty.

Innovation is not limited to the largest incumbents. New and ambitious manufacturers are entering the market with agile approaches, emphasizing customization, rapid prototyping, and responsive design tailored to niche segments. These newer players are tapping into digital printing technologies, enabling shorter runs with high-resolution graphics that were once only feasible for large-scale orders. This democratization of innovation is helping smaller manufacturers attract clientele from local food producers, specialty retailers, and direct-to-consumer businesses seeking personalized packaging solutions.

Regional Trends Highlight Diverse Growth Patterns

Across the United States, regional demand patterns reflect distinct market characteristics. The Western states are poised for some of the highest growth, buoyed by an active packaging industry and heightened consumer demand for sustainable products. The Southern region follows closely, where a flourishing manufacturing base and distribution ecosystem underpin substantial adoption of cardboard tray solutions.

The Northeast exhibits stable but steady growth, shaped by established industrial activity and a progressive shift toward greener packaging alternatives. Meanwhile, the Midwest’s traditional manufacturing foundation shows slower yet persistent uptake as regulatory and consumer pressures gradually shift the focus toward recyclable options.

These regional nuances emphasize the importance of localized strategies for manufacturers and suppliers seeking to optimize production, distribution, and customer engagement across varied market landscapes.

Emerging Technologies and Market Opportunities

Innovation within the cardboard trays sector has accelerated with the adoption of new materials and technologies. Manufacturers are experimenting with enhanced barrier coatings and moisture-resistant treatments to extend tray application into refrigerated and chilled food categories. Hybrid designs that pair corrugated bases with fiber lids or sleeves are gaining traction, offering improved performance while maintaining recyclability.

Digital transformation is also influencing production processes. Modern die-cutting and flexible printing technologies have lowered entry barriers for custom solutions, opening doors for smaller firms and regional manufacturers to serve specialized market segments efficiently. As automation becomes more prevalent in packaging lines, trays engineered for seamless robotic handling are creating new value propositions in high-volume environments like e-commerce fulfillment centers.

Furthermore, the rising demand for mono-material and easy-to-recycle packaging formats is pushing innovation toward designs that support end-of-life recycling systems, aligning with broader industry commitments to reduce waste and enhance circularity.

Outlook and Industry Impact

The United States cardboard trays market is at an inflection point. With market value poised to rise significantly over the coming decade, both established leaders and emerging manufacturers are advancing their capabilities to capture growth opportunities. Driven by sustainability imperatives, technological innovation, and shifting consumer preferences, cardboard trays are set to become an even more integral part of the packaging landscape.

Companies that invest in sustainable materials, adopt flexible manufacturing technologies, and harness data-driven insights into consumer needs will be best positioned to lead this expanding market — delivering packaging solutions that satisfy performance requirements, reinforce brand values, and support environmental stewardship across industries.