The global wheat gluten market is projected to expand from USD 16.6 billion in 2025 to USD 39.7 billion by 2035, registering a strong CAGR of 9.1%. This remarkable growth reflects accelerating consumer interest in plant-based food products, the increasing preference for whole grain bread, and the versatile functional role of wheat gluten as a binding, texturizing, and elasticity-enhancing ingredient across multiple food categories.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-9769

Demand is further boosted by wheat gluten’s ability to enhance product quality in vegan meat substitutes and convenience foods. Producers are increasingly leveraging wheat gluten to improve elasticity, moisture retention, and structural integrity in bakery products and meat analogs, cementing its status as a high-value functional ingredient.

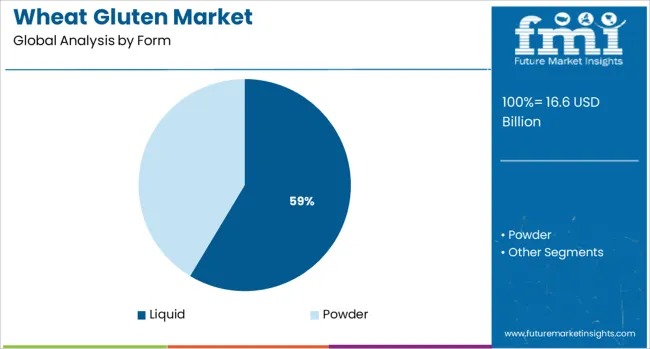

Liquid Wheat Gluten Dominates with 58.6% Market Share

Liquid wheat gluten is expected to account for 58.6% of the market in 2025, driven by strong use in industrial food processing. Its cost-efficiency and ease of incorporation into formulations-especially bread, meat analogs, and processed snacks-position it as the go-to form for large-scale manufacturers.

Key Advantages of Liquid Wheat Gluten

• Simplifies mixing and food formulation processes

• Enhances dough elasticity and water retention

• Reduces processing time and improves consistency

• Widely applicable in plant-based meat production

Its growing application in vegan meat alternatives significantly strengthens its market trajectory, particularly among brands targeting high-protein, clean-label, and nutrient-dense products.

Whole Grain Bread Leads End-Use Applications at 32.9%

The whole grain bread segment is forecast to command 32.9% of total demand in 2025 as consumers increasingly seek nutrient-rich alternatives to refined white bread. Wheat gluten provides essential structural support to whole grain doughs, improving volume, elasticity, and shelf life-key factors influencing consumer purchase decisions.

This aligns with rising global consumption of foods high in fiber, complex carbohydrates, and plant-based protein, keeping whole grain bakery products at the forefront of demand.

Plant-Based Diets Propel Market Growth

The shift toward vegan and flexitarian diets is a major catalyst for the wheat gluten market. According to The Vegan Society (2024):

• 44% of consumers globally tried vegan meat substitutes

• 81% consumed plant-based milk alternatives

• 48% consumed dairy-alternative products

With wheat gluten increasingly used as a protein-rich meat alternative, this trend underscores long-term market expansion driven by ethical consumerism, lactose intolerance, and environmental sustainability.

Market Challenges: Increasing Gluten-Free Adoption

Health concerns surrounding gluten sensitivity and celiac disease are expected to marginally restrain growth. Consumption of gluten can trigger reactions linked to gliadin, causing symptoms such as bloating, muscle pain, fatigue, nausea, and abdominal discomfort. Despite these challenges, innovation in gluten extraction and heightened awareness of plant-based nutrition continue to support market expansion.

Regional Insights

North America Leads Demand

North America is projected to maintain its leadership, supported by a rapidly expanding vegan population. In January 2025, 629,000 people worldwide participated in Veganuary, with significant adoption in the U.S. and Canada. High consumption of meat alternatives and protein-rich diets among athletes further strengthens demand for wheat gluten across the region.

Asia Pacific Emerging as a Fast-Growing Market

Asia Pacific ranks second due to growing preference for regenerative, plant-based nutrition in India and China. Rising cases of lifestyle diseases such as diabetes-affecting 8.7% of adults aged 20-70 years in India (WHO)-are pushing consumers toward healthier food options, elevating demand for wheat gluten in everyday diets.

Competitive Landscape

The wheat gluten market is characterized by strong competition with companies expanding portfolios through R&D, acquisitions, and high-value product innovation. Major players include:

Crespel & Deiters GmbH, Pioneer Industries Limited, Anhui Ante Food, Ardent Mills LLC, MGP Ingredients, Anhui Ruifuxiang, Z & F Sungold Corporation, Royal Ingredients Group, Tereos, Shandong Qufeng, Kroener Staerke, Cargill Inc., AB Amilina, and others.

Strategic priorities include:

• Expansion into plant-based meat ingredients

• Advanced gluten extraction technologies

• Focus on clean-label formulations

• Collaboration with bakery and vegan brands to optimize protein applications