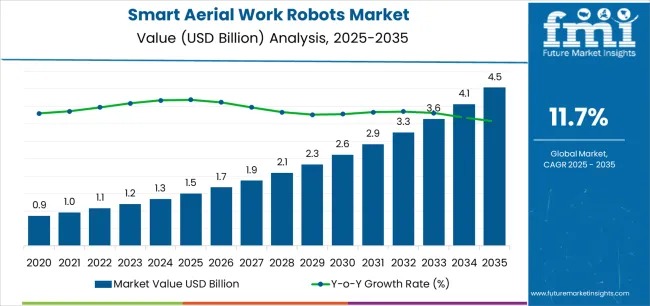

The global Smart Aerial Work Robots Market is entering a decade of accelerated growth, projected to surge from USD 1.5 billion in 2025 to USD 4.6 billion by 2035, registering a robust CAGR of 11.7%. With industry-wide digitalization and inspection automation gaining priority, aerial work robots are becoming indispensable tools for power utilities, renewable energy operators, and infrastructure asset owners seeking safer, faster, and more accurate operational oversight.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates:

https://www.futuremarketinsights.com/reports/sample/rep-gb-27937

This growth is anchored in strong performance across robot types, with multirotor aerial work robots leading the market at 56.5% share, attributed to their exceptional stability, multi-sensor payload compatibility, and suitability for critical inspection tasks across power lines, wind turbines, and industrial facilities. Their ability to deliver high-resolution visual and thermal data, combined with autonomous flight capabilities, positions them as the preferred choice among operators seeking repeatable and reliable inspection cycles.

Market Growth Accelerators (2025–2035)

Between 2030 and 2035, the market will add USD 2.26 billion in new revenue, representing nearly 62% of the decade’s total expansion. This period will witness:

- Large-scale adoption of AI-powered defect detection

- Integration with asset management and digital twin platforms

- Transition from manual to fully autonomous inspection workflows

- Increased deployment across national grids, wind farms, and large industrial facilities

As industries strengthen predictive maintenance strategies, the demand for aerial robots with greater intelligence, versatility, and real-time data capabilities will continue to rise.

Robot Type Performance: Multirotor Systems Remain at the Core

- Multirotor Aerial Work Robots (56.5% share)

These platforms dominate due to:

- Exceptional flight stability

- 96–98% consistent data capture reliability

- Compatibility with thermal cameras, LiDAR, and advanced optical sensors

- Seamless integration with SCADA and asset management systems

They are essential for large-scale transmission inspections, supporting utilities in minimizing downtime and improving grid reliability.

- Robotic Arm Aerial Work Robots (25.4% share)

Designed for contact-based tasks, these robots support:

- Building façade operations

- High-rise maintenance

- Precision manipulation where non-contact robots fall short

Rising automation in construction maintenance continues to fuel adoption.

- Crawler-Type Aerial Robots (12.3% share)

Ideal for:

- Wind turbine blade inspection

- Confined space activity

- Vertical surface navigation with magnetic or adhesion systems

Their utility is increasing as wind farm capacity expands worldwide.

- Airbag and Other Emerging Formats (5.8% combined share)

These novel systems address niche inspection environments such as:

- Tunnel interiors

- Bridges

- Enclosed structures

- Marine and telecom assets

Their adaptability positions them for steady long-term growth.

Application Insights: Power Infrastructure Leads with 45% Share

Power line and transmission inspections represent the largest application segment due to:

- Aging grid infrastructure

- High outage prevention requirements

- Vegetation risk assessment

- Thermal hotspot detection

- Strict regulatory compliance standards

The segment shows the fastest CAGR at 12.8%, supported by grid modernization initiatives in East Asia, South Asia Pacific, Europe, and North America.

Regional Growth Patterns

East Asia and South Asia Pacific – Fastest Expansion

China (15.7% CAGR) and India (14.6% CAGR) lead global adoption, driven by:

- Large-scale grid expansion

- High renewable energy penetration

- Government-led smart infrastructure initiatives

North America & Europe – Stable, Technology-Led Growth

The United States (11.1% CAGR) and Germany (13.4% CAGR) maintain steady growth due to:

- Strict safety regulations

- Mature industrial automation ecosystems

- Investment in autonomous inspection technologies

Strategic Priorities for Market Participants

Operators and vendors aiming to gain competitive advantage must prioritize:

- Autonomy-first design philosophy for reduced manual intervention

- Full-stack solutions: robots + workflow software + analytics

- Outcome-focused pricing models, enabling inspection-as-a-service

- Robust safety features such as automated obstacle avoidance

- Digital integration readiness, enabling predictive analytics and real-time reporting

The shift toward turnkey, data-driven inspection ecosystems underscores the importance of delivering complete, standardized workflows that reduce operational complexity.

Get data that aligns with your strategic priorities — ask for report customization today:

https://www.futuremarketinsights.com/customization-available/rep-gb-27937

Related Reports

Transformer Monitoring System Market – https://www.futuremarketinsights.com/reports/transformer-monitoring-system-market

Sulphur Recovery Technology Market – https://www.futuremarketinsights.com/reports/sulphur-recovery-technology-market

Marine Fuel Injection System Market – https://www.futuremarketinsights.com/reports/marine-fuel-injection-system-market

Have a specific Requirements and Need Assistant on Report Pricing or Limited Budget please contact us – sales@futuremarketinsights.com

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

Why FMI: https://www.futuremarketinsights.com/why-fmi

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube