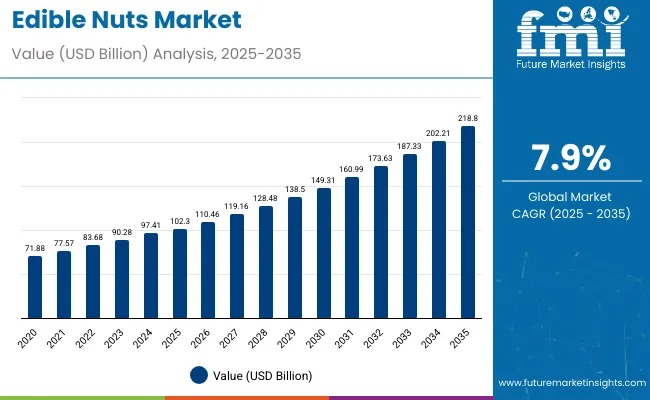

The global edible nuts market is set to witness strong acceleration, with the industry valued at USD 102.3 billion in 2025 and projected to reach USD 218.8 billion by 2035, expanding at a CAGR of 7.9%. The sector is poised to add an absolute dollar opportunity of USD 116.5 billion, driven by evolving consumer diets, clean-label demand, sustainability initiatives, and product innovation reshaping snacking and ingredient applications.

The growth trajectory indicates that by 2030, the market will reach USD 155.5 billion, recording USD 53.2 billion in value creation in the first five years. The remaining decade will generate USD 63.4 billion, reflecting a slightly back-loaded growth pattern influenced by technological advances in processing, organic certifications, and adoption of premium formulations.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-1530

Key Market Highlights

• Market Value (2025): USD 102.3 billion

• Forecast Value (2035): USD 218.8 billion

• Forecast CAGR: 7.9%

• Highest Segment Share: Store-Based Retailing (75%)

• Key Growth Regions: North America, Europe, Asia Pacific

• Leading Players: Olam International Ltd, Archer Daniels Midland Company, Blue Diamond Growers, Mariani Nut Company, The Wonderful Company LLC

What Is Fueling Growth?

Edible nuts offer a compelling nutritional profile with high plant proteins, healthy fats, antioxidants, and essential minerals, making them a preferred choice among health-focused consumers and premium food manufacturers. Emerging diet patterns-Mediterranean, vegan, and flexitarian-are boosting demand for natural, minimally processed, and functional products.

Growing disposable incomes, global e-commerce accessibility, and procurement advancements in sustainable agriculture are opening new channels for value-added innovations, particularly in organic, flavored, roasted, and cold-pressed nut formats.

Market Share in Parent Industries

Nutritional density and clean-label positioning enable edible nuts to dominate complementary markets:

• Healthy snacks

• Plant-based protein

• Premium food ingredients

• Natural ingredient applications

• Organic foods

Their culinary versatility supports adoption in confectionery, bakery, beverages, cereal mixes, gourmet cuisine, and ready-to-eat applications.

Segmental Snapshot

By Product Type

Almonds lead with a 30% share, driven by superior protein content, antioxidant value, and diverse use in snacking, baking, and ingredient manufacturing. Manufacturers are enhancing shelf stability, certifications, and traceability, advancing premium nut formulations across retail and food service channels.

By Distribution Channel

Store-based retailing commands 75% of the market, facilitating consumer trust through physical inspection, promotions, specialty assortments, and in-store education. Growth is reinforced by expansion in health food chains and premium grocery formats.

Supply Challenges and Price Sensitivities

Despite strong demand, the industry faces climate dependency, raw material cost fluctuations, and sustainability compliance burdens. Nut prices range widely, contributing to supply volatility, while certification processes add sourcing costs in premium markets. These challenges emphasize supply chain resilience, processing innovation, and diversified sourcing strategies.

Regional Market Insights

• UK: Highest projected CAGR of 8.4%, fueled by health-conscious snacking and organic adoption.

• Germany: Strong growth supported by sustainability-led certifications and premium retail expansion.

• India: Rapid adoption due to cultural consumption, rising disposable incomes, and e-commerce penetration.

• Brazil: Expansion driven by domestic production advantages and export potential.

• France: Moderate growth in gourmet applications and Mediterranean diet adoption.

• USA: Steady growth, reflecting market maturity and established consumption patterns.

• China: Constrained growth due to price sensitivity and traditional consumption habits.

Competitive Landscape

The market is moderately consolidated with Olam International Ltd holding ~15% share, followed by ADM and Blue Diamond Growers. Companies differentiate through:

• Vertical sourcing integration

• Sustainable farming investments

• Flavor and format innovations

• Premium brand positioning & direct-to-consumer strategies

Entry barriers remain significant due to traceability, processing technology, and food safety standards, rewarding integrated producers and certified premium brands.