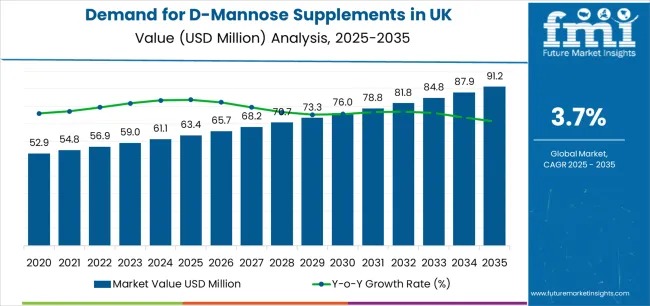

The United Kingdom’s D-mannose supplements market is on a steady upward trajectory, projected to rise from USD 63.4 million in 2025 to USD 91.2 million by 2035, marking a 3.7% CAGR. This growth—reflecting nearly 40% value expansion—is propelled by rising preference for natural health routines, preventive care habits, and strong consumer interest in science-backed supplementation. England continues to lead national uptake as digital-health adoption grows and wellness-conscious consumers shift toward cleaner, evidence-supported formulations.

Growing transparency in supplement ingredients, tighter quality control norms, and the UK’s mature wellness ecosystem are setting the stage for long-term market stability. Consumers increasingly value clinically grounded, high-purity formulations, positioning D-mannose as a preferred solution for urinary tract health and general wellness maintenance.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-28344

Premium Wellness Trends Strengthen Market Momentum

The period from 2030 to 2035 is expected to contribute USD 12.9 million in new revenue—accounting for 51% of total decade-wide growth. This acceleration stems from the rise of personalized supplementation systems, improved bioavailability technologies, and rapid expansion of digital-commerce wellness platforms.

Demand is particularly strong across England and Scotland, where advanced health infrastructure, digital wellness adoption, and higher consumer spending on preventive care amplify market penetration.

From 2020 to 2025, the market benefitted from increasing awareness of urinary tract health and broader acceptance of natural wellness principles. UK supplement manufacturers responded by strengthening formulation efficacy, ensuring regulatory compliance, and expanding consumer education—driving higher product trust and usage.

UK D-Mannose Supplements – Market Snapshot

- Market value in 2025: USD 63.4 million

- Forecast value in 2035: USD 91.2 million

- Forecast CAGR: 3.7%

- Leading product type: Capsules (48.6%)

- Strongest demand regions: England, Scotland, Wales, Northern Ireland

- Key companies: Nature’s Pure Edge, Cytoplan, Power Health, Bio-Tech Pharmacal, Health Genesis

Core Drivers Behind Growing UK Demand

- Rising Natural Wellness and Preventive Health Priorities

Consumers are increasingly opting for natural, research-supported solutions to support urinary tract health and daily wellness management.

- Strong Growth of Online Sales and Digital Health Ecosystems

With online platforms set to capture 54.2% of demand in 2025, digital commerce is reshaping access, product comparison, and buying behavior.

- Strengthening Quality Standards and Regulatory Measures

The UK’s emphasis on high formulation purity and compliance encourages adoption of supplements that meet stringent quality benchmarks.

High-Value Opportunity Pathways for Market Participants

Manufacturers and wellness brands operating in the UK can leverage multiple revenue avenues:

- Premium Wellness & Health Centres: USD 9.2–13.8 million

- E-commerce & Direct-to-Consumer Expansion: USD 7.8–11.7 million

- Bioavailability-Enhanced Formulations: USD 6.3–9.4 million

- Innovative Capsule Technologies: USD 8.1–12.2 million

- Specialty & Premium Formulations: USD 5.7–8.6 million

- Technical Support & Service Networks: USD 4.4–6.6 million

These pathways underscore a market shifting toward advanced supplementation systems that meet precision wellness and performance expectations.

Segmental Highlights

Capsules Remain the Preferred Product Format

Holding 48.6% share in 2025, capsules dominate due to their compatibility with wellness routines, reliable absorption characteristics, and consumer familiarity. They also integrate easily into existing health infrastructure, supporting widespread adoption.

Online Sales Lead the Application Landscape

With 54.2% share, online channels continue to expand due to:

- Convenience and accessibility

- Deep product information availability

- Strong penetration of wellness-focused digital retailers

- Growth of direct-to-consumer supplement brands

Digital health leadership in England and Scotland further fuels this expansion.

Regional Outlook – England at the Forefront

England is the fastest-growing market, expanding at 3.9% CAGR through 2035. The region benefits from progressive consumer wellness preferences, robust innovation clusters, and advanced digital health systems that support rapid adoption of premium formulations.

Scotland follows closely, supported by strong health infrastructure and a growing wellness-conscious population. Wales and Northern Ireland maintain steady growth as modernization of health facilities and wellness programs accelerates supplement adoption across all regions.

Competitive Landscape

Competition is characterized by specialized supplement manufacturers and natural wellness companies prioritizing product innovation, supply chain resilience, and multi-channel distribution strength. Leading brands include Nature’s Pure Edge, Cytoplan, Power Health, Bio-Tech Pharmacal, Health Genesis, Novomins, AZO Products, Vox Nutrition, Sanotact, and VITA1.

Players are increasingly focusing on bioavailability improvements, premium formulation quality, and strategic digital partnerships to strengthen national reach and customer trust.