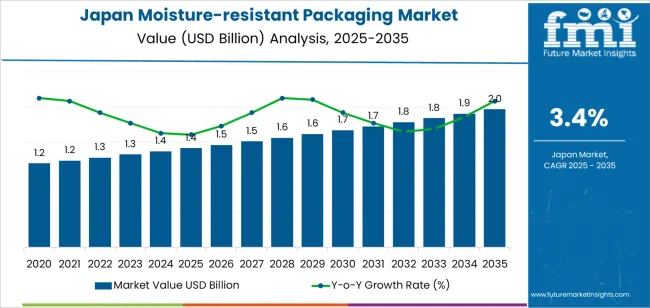

The moisture-resistant packaging market in Japan is entering a dynamic period of growth and transformation, driven by evolving consumer expectations, technological advancements, and strategic moves by both established and emerging players. Valued at approximately USD 1.4 billion in 2025 and projected to expand to USD 2.0 billion by 2035, the market is poised to capitalize on rising demand across food, pharmaceutical, consumer goods, and industrial applications.

As manufacturers and brands across industries seek better ways to protect products from humidity, condensation, and environmental exposure, moisture-resistant packaging solutions are becoming an essential component of Japan’s broader packaging ecosystem. This growth is supported by increasing production volumes, longer supply chains, and the relentless push for quality assurance — all of which have underscored the importance of advanced barrier technologies.

Meeting Diverse Industry Needs Through Advanced Solutions

In Japan’s humid climate, moisture can significantly compromise the quality and shelf life of products ranging from packaged foods to personal care items. In response, manufacturers are deploying barrier films, multilayer laminates, coated materials, and innovative sealing techniques that provide reliable moisture protection while aligning with sustainability goals.

One of the most notable trends in the market is the growing adoption of bags and pouches, which currently account for a significant share of moisture-resistant packaging formats. Their lightweight nature, versatility, and compatibility with resealable closures make them ideal for everyday consumer products — especially in the rapidly expanding ready-to-eat food segment. These formats also support efficient logistics and storage, making them attractive to both brand owners and retailers.

The adoption of plastic materials remains robust, accounting for a leading portion of market demand due to their superior moisture barrier properties, adaptability to high-speed production, and cost-effective performance. However, the market is witnessing a paradigm shift as sustainability and circular economy goals encourage manufacturers to explore recyclable plastics, coated paperboard, and bio-based alternatives that reduce environmental impact without compromising functionality.

Established Leaders and Emerging Innovators Shape the Competitive Landscape

At the forefront of this evolution are several global and regional packaging manufacturers who have built strong positions through innovation, collaboration, and strategic investment. Leading firms offering moisture-resistant solutions include renowned packaging conglomerates with extensive global footprints and technical expertise. These companies bring to market a range of flexible films, high-barrier laminates, and moisture-protective cartons tailored to Japan’s exacting quality standards and consumer preferences.

These established players are not only scaling production of high-performance solutions but also integrating sustainability into their product portfolios — a response to both regulatory focus on materials reduction and rising consumer demand for eco-friendly packaging.

In parallel, new and emerging manufacturers are injecting fresh competitive energy into the market. These nimble firms are often at the cutting edge of technology, introducing niche innovations such as humidity-sensing films, active barrier coatings, and modular packaging platforms that enhance moisture resistance while boosting recyclability. Collaborations between start-ups and traditional manufacturers are becoming more common, enabling rapid piloting and scaling of next-generation materials.

Regional Growth and Market Dynamics

While moisture-resistant packaging demand is robust across Japan, certain regions are experiencing particularly strong momentum. The Kyushu & Okinawa area is emerging as a growth hotspot, buoyed by increased production activities in the food and pharmaceutical sectors and heightened awareness of product quality standards among consumers. Metropolitan hubs such as the Kanto and Kinki regions continue to drive demand, supported by dense industrial clusters, logistics infrastructure, and strong retail consumption.

Smaller and semi-urban regions are also contributing to the overall growth picture as local manufacturers adopt advanced packaging solutions to compete more effectively in both domestic and export markets.

Challenges and Opportunities Ahead

Despite positive momentum, the market faces notable challenges. High costs associated with barrier materials and specialized production processes can be a barrier for smaller brands. Additionally, balancing performance with environmental responsibility remains a critical hurdle, as regulations tighten and consumer expectations for sustainability increase.

Nevertheless, industry experts see substantial opportunities on the horizon. The growth of e-commerce — including direct-to-consumer delivery models — is expanding the need for moisture-resistant packaging that can withstand variable transit and storage conditions. Likewise, segments such as frozen foods, premium personal care products, and high-barrier pharmaceuticals are expected to drive above-average demand for innovative packaging formats.

Advancements in materials science, digital manufacturing, and smart packaging technologies also promise new avenues for differentiation. For example, films embedded with moisture indicators, biodegradable high-barrier coatings, and modular packaging designs that simplify recycling all represent areas where forward-thinking manufacturers can gain competitive advantage.

Looking Forward

As Japan’s packaging industry continues to evolve, the moisture-resistant segment stands out as a strategic growth area that blends performance with innovation and sustainability. With both established giants and innovative newcomers working to meet diverse market needs, the stage is set for a decade of progressive transformation that delivers value to manufacturers, brands, and consumers alike.