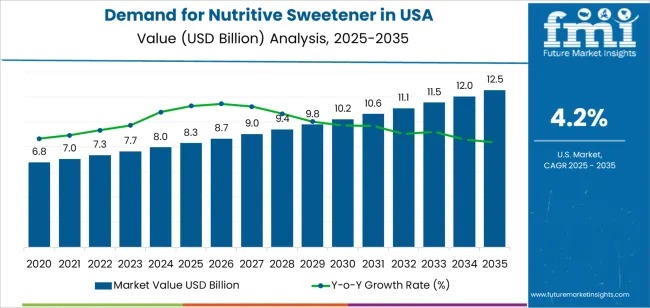

The demand for nutritive sweeteners in the USA is set for significant expansion, projected to reach USD 12.5 billion by 2035, up from USD 8.3 billion in 2025, according to recent market estimates. The market is expected to grow at a CAGR of 4.20%, driven by strong consumer interest in healthier sweetening solutions, cleaner labels, and improved taste profiles across food and beverage applications.

Nutritive sweeteners—such as sucrose, fructose, glucose, honey, and sugar alcohols—continue to play a crucial role in the country’s food manufacturing ecosystem. While consumers are reducing sugar intake, they remain highly unwilling to compromise on taste, texture, and overall sensory experience. This dynamic is encouraging manufacturers to adopt modern nutritive sweeteners that deliver balanced sweetness along with functional benefits like moisture retention, browning, and mouthfeel enhancement.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-28702

Market Snapshot

- 2025 Market Value: USD 8.3 Billion

- 2035 Forecast Value: USD 12.5 Billion

- CAGR (2025–2035): 4.20%

- Leading Product Type: Fructose (38% share)

- Top Nature Segment: Organic (65% share)

- Largest End Use: Food Processing (30% share)

- Leading Region: West (4.8% CAGR)

- Key Players: Tate & Lyle, Cargill Inc., Showa Sangyo, Japan Corn Starch Co., COFCO International

Steady Growth Driven by Reformulation and Health-Focused Consumption

Between 2025 and 2030, demand for nutritive sweeteners is expected to grow moderately, adding USD 1.5 billion—a rise of nearly 18%. This period marks steady reformulation activity, especially in beverages, bakery, and confectionery, where manufacturers are seeking healthier, lower-calorie options without altering taste.

From 2030 to 2035, growth accelerates, adding another USD 2.7 billion, underpinned by rising preference for natural sweeteners, increased use of organic ingredients, and emerging sugar-reduction technologies that improve sweetness profiles while reducing caloric density.

What’s Driving Demand?

The U.S. nutritive sweeteners market is expanding because food and beverage manufacturers still rely heavily on these sweeteners for performance and cost efficiency. Key drivers include:

- The need for sweetness, browning, and bulk in processed foods

- Rapid expansion of functional foods and beverages

- Heightened awareness of clean-label and natural sweetening sources

- Increasing consumer desire for reduced-sugar products without artificial additives

As lifestyle diseases linked to sugar consumption rise, consumers and brands are shifting toward fructose, honey, organic sugar, and advanced sugar alcohols that support healthier formulation.

Segment Analysis: Why Fructose Leads the Market

Fructose holds a 38% share, making it the largest product type in the U.S. This dominance is fueled by its high sweetness intensity, cost efficiency, and ability to enhance flavor in beverages, bakery, dairy, and ready-to-eat meals. High-fructose corn syrup (HFCS) remains a mainstay in large-scale formulation due to its stability and functional versatility.

Organic Sweeteners Take the Lead

Organic sweeteners account for 65% of total demand, driven by shifting consumer preferences toward sustainable, transparent, and additive-free ingredients. The growth of organic food manufacturing—especially premium snacks and beverages—is accelerating their adoption.

Food Processing Sector Remains the Largest End User

Food processing represents 30% of total demand, as sweeteners remain indispensable for flavor, texture, and cost management. Innovation in ready-to-eat formats and health-positioned beverages continues to push sweetener usage upward.

Store-Based Retail Dominates Distribution

With 45% share, retail stores remain the leading channel due to convenience, wide assortments, and rising consumer interest in at-home usage of organic and specialty sweeteners.

Regional Outlook: West Leads in Growth

The West region leads with a 4.8% CAGR, fueled by strong adoption of clean-label, organic, and plant-based foods. States such as California and Washington continue to set nationwide trends in health and wellness.

The South follows at 4.3% CAGR, supported by the region’s expanding food manufacturing sector. The Northeast posts 3.8% CAGR, while the Midwest trails at 3.3%, sustained by steady uptake in food production and consumer wellness priorities.

Competitive Landscape

Tate & Lyle commands approximately 34.3% market share, reinforcing its leadership in sweetening solutions across major food categories. Other influential players—Cargill Inc., Showa Sangyo, Japan Corn Starch Co., and COFCO International—continue to strengthen U.S. supply capabilities with advanced sweetener technologies, new formulations, and region-specific innovation pipelines.

While rising regulatory pressure around sugar reduction and competition from non-nutritive sweeteners present challenges, nutritive sweeteners remain indispensable for many applications that require full sweetness, bulk, and texture integrity.