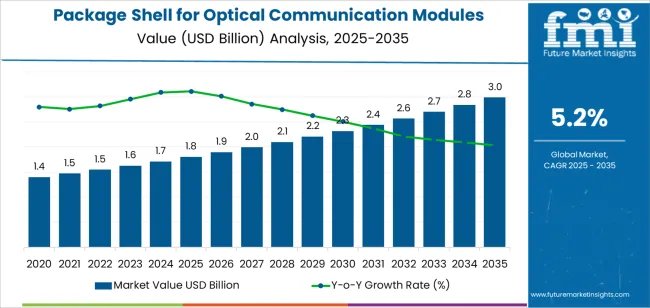

The market for package shells used in optical communication modules is on a promising growth trajectory — rising from a global value of USD 1.8 billion in 2025 to an estimated USD 3.0 billion by 2035. This robust expansion, at a compound annual growth rate (CAGR) of 5.2%, underscores the critical role of enclosures and housings that protect delicate optical transceivers in fast-evolving data and telecom infrastructures.

Package shells serve far more than a protective casing: they deliver thermal management, electromagnetic shielding, mechanical protection, and precise alignment for active optical and optoelectronic components. As demands increase for higher data-rates, miniaturization, and reliability, the importance of advanced shell design and manufacturing has never been greater.

Driving Forces: Data Centers, 5G & Cloud, and the Surge in Bandwidth

The shift toward ever-faster data transmission — propelled by 5G/6G rollouts, cloud-services proliferation, edge computing, and the deployment of hyperscale data centers — is at the heart of this growth. Increasing data consumption, the rise of smart cities, and the growing footprint of fiber-optic networks worldwide are fueling the demand for optical communication modules, and consequently, for high-performance package shells to house them.

In particular, modules rated between 100–400 Gbps are already dominating the market, accounting for 45% of total package-shell demand. Their balance of cost, performance, and reliability makes them well suited for data-center workloads, telecom backbones, and cloud infrastructure. Meanwhile, the data-center segment itself already commands roughly 30% of the market share among end-use sectors — and that share is expected to rise as cloud, storage, and streaming services expand globally.

A Diverse and Growing Ecosystem of Suppliers

The market landscape is diverse and competitive. On one end, established global suppliers — firms like Kyocera, Niterra, RF-Materials Co., LTD, EGIDE, and Ametek — continue to defend their leadership positions. With long-standing experience, mature manufacturing capacity, and broad customer bases, they remain well-positioned to meet the high-precision demands of telecom and data center operators worldwide.

On the other end, a burgeoning wave of newer entrants — many from the Asia-Pacific region — are aggressively expanding capacity, innovating in material science and production techniques, and seeking to capture growing regional demand. Companies such as Hebei Sinopack, CCTC, Hefei Shengda Electronics Technology, Jiaxing Glead Electronics (BOStar), Anhui Optispac Technology, Wuhan Fingu Electronic Technology, and a host of others are emerging as formidable players. Their efforts signify a shift toward regionalised production, cost-effective manufacturing, and tighter proximity to expanding telecom and data-center markets in Asia, particularly in countries like India and China.

This trend opens new opportunities not only for major contractors and OEMs but also for smaller, agile manufacturers aiming to carve out niches in specific geographies or specialization areas (e.g., ceramic-metal composite shells, hermetic sealing solutions, miniaturized high-density shells, plug-and-play modules).

Innovation, New Materials and Emerging Shell Technologies

Market growth is not just a function of increased volume — it’s equally driven by innovation. As optical communication modules become denser, faster, and more energy-efficient, shell manufacturers are responding with advanced materials (ceramic composites, high-conductivity metal alloys), improved manufacturing processes (precision stamping, automated assembly, hermetic sealing), and modular packaging solutions that accelerate time-to-market.

Emerging trends point toward shells designed for bandwidth classes beyond 400 Gbps, with improved thermal management and signal integrity. Meanwhile, plug-and-play or modular packaging solutions — pre-qualified, scalable assemblies that simplify integration — are gaining traction among module assemblers. Add to this the growing demand for lighter, more eco-friendly, and recyclable materials, and the picture that emerges is one of a dynamic, innovation-driven industry.

Market Outlook: Global Reach, Regional Growth Opportunities

While global demand continues to grow, certain regions show especially high growth potential. Asia-Pacific — with its expanding 5G infrastructure, data center build-out, and broadband penetration — is emerging as a key growth hub. In particular, India’s package-shell market is forecasted to advance at a CAGR of approximately 6.5%, reflecting both domestic digital infrastructure initiatives and increasing cloud/data-center investments. Other critical markets include regions such as China, Europe, North America, and Latin America, where telecom modernization, fiber-optic rollout, and enterprise data demand continue rising.

What This Means for Market Players — Established and New

For legacy manufacturers, the growth outlook reinforces the need to continue investing in R&D, expand production capacity, and innovate to stay ahead of evolving technical demands, be it higher data-rate modules, miniaturization, or thermal performance. For emerging manufacturers and new entrants, the market represents a compelling opportunity: increasing global demand, regional infrastructure build-out, and a growing appetite for cost-efficient, high-quality shells highlight clear space for expansion.

At the same time, the shifting landscape places a premium on agility, quality control, and the ability to anticipate shifting standards for optical communication modules — which, if met successfully, can differentiate ahead of competition.