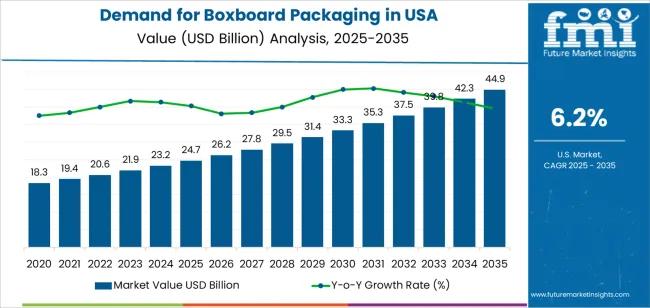

In a rapidly evolving packaging landscape, the U.S. boxboard packaging market is set to embark on a transformative growth journey over the next decade. According to the latest industry forecast, demand for boxboard packaging in the United States is projected to rise from USD 24.7 billion in 2025 to USD 44.9 billion by 2035, representing a robust compound annual growth rate (CAGR) of 6.2%.

This surge is being driven by a confluence of powerful market forces — among them, rising consumer demand for sustainable and recyclable packaging, accelerating growth in food & beverage, personal care, and e-commerce sectors, and an increasing shift toward lightweight, cost-efficient materials that offer both functional strength and visual appeal.

Sustainability and versatility: the new gold standard

Boxboard’s versatility — its ability to combine structural integrity, excellent printability, and recyclability — is making it increasingly attractive for a broad cross-section of end-use industries. In particular, the food and beverages segment stands out as the dominant end user, accounting for roughly half of total demand. Folding boxboard (FBB), prized for its lightweight yet strong construction and high-quality print surface, is projected to command about 45% of total boxboard uptake in 2025.

Against a backdrop of rising environmental awareness and regulatory pressure to reduce plastic use, many brands are choosing boxboard packaging as a way to meet sustainability commitments without compromising on functionality or shelf appeal. As meal kits, ready-to-eat foods, personal care items, premium goods, and direct-to-consumer ecommerce packages proliferate, the need for protective yet eco-friendly packaging solutions has never been greater.

From established giants to nimble newcomers: a dynamic competitive landscape

The market’s growth narrative isn’t being written by legacy manufacturers alone. While established global heavyweights — such as International Paper, WestRock, Stora Enso, Smurfit Kappa, DS Smith and Mondi Group — continue to lead thanks to their massive production capacity, global supply chains, and established brand relationships, a wave of new and regional manufacturers is entering the fray.

These newcomers are bringing fresh energy by focusing on niche segments, customization, and technological differentiation. Their value proposition includes agile production cycles, specialty boxboard grades tailored for cosmetics, pharmaceuticals, or premium consumer goods, and faster response times for smaller or regional customers. They are also exploring emerging opportunities such as high-strength recycled fiber boards, advanced coating and barrier technologies, and lighter-weight substrates — all aimed at balancing cost, performance, and environmental credentials.

For established players, this competitive pressure is prompting innovation, expansion of sustainable packaging portfolios, and a rethinking of supply-chain strategies. Investments in new manufacturing lines, optimized logistics, and upgraded finishing capabilities are underway to meet the growing demand for premium, retail-ready packaging that resonates with environmentally conscious consumers.

Technology, sustainability and market trends shaping the future

In the coming years, the boxboard market is expected not only to grow in size, but also to evolve technologically. Improvements in coating technologies, high-strength recycled fibers, and lightweighting innovations promise to enhance performance without significantly increasing costs. Meanwhile, rising interest in premium packaging — especially for cosmetics, personal care, and direct-to-consumer e-commerce — is fueling demand for boxboard designs that merge structural integrity with high-end print quality and aesthetic appeal.

Furthermore, the shift toward circular packaging models is gaining traction. As brands and retailers embrace sustainability goals, boxboard’s recyclability and potential for reusable or circular lifecycle use make it a frontrunner in replacing traditional plastics and multi-layer laminates.

A strategic moment for manufacturers and brands alike

For packaging manufacturers — both large and emerging — the next decade represents a strategic window of opportunity. Established producers have the scale and resources to invest heavily in sustainable board grades, barrier coatings, and efficient supply-chain operations. At the same time, new entrants and regional players can leverage flexibility, customization capabilities, and niche specialization to capture underserved segments and meet growing demand for eco-friendly, high-quality packaging.

For brand owners and retailers, the transformation offers a compelling path forward: to align with sustainability commitments, satisfy evolving consumer expectations for premium and environmentally responsible packaging, and benefit from cost-effective, scalable solutions that remain adaptable as market demands shift.

Conclusion: A new packaging era begins

As the U.S. boxboard packaging market heads toward nearly USD 45 billion by 2035, the stage is set for a renewed era of innovation, competition, and sustainable growth. From global leaders expanding their production footprints to nimble newcomers tailormaking boxboard for niche applications, the industry is evolving rapidly — with recyclability, performance, and design sophistication at its core.

This is not just a growth story. It is a story about transformation — of materials, of manufacturing, and of how products reach consumers. And with shifting consumer values, regulatory momentum behind sustainability, and demand for lightweight, customizable packaging soaring, few sectors are as well-positioned to ride the wave as boxboard.