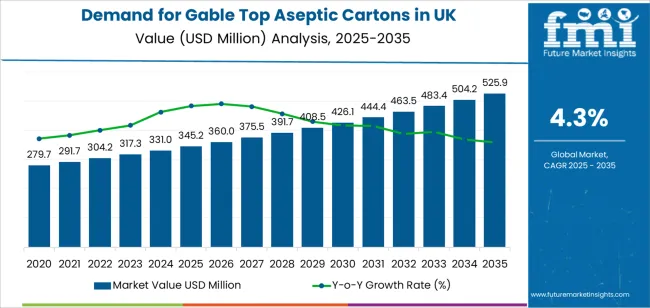

The market for gable-top aseptic cartons in the United Kingdom is poised for substantial expansion over the next decade, offering a rich landscape of opportunity for both well-established players and ambitious new entrants. According to recent projections, demand is forecast to rise from USD 345.2 million in 2025 to USD 525.9 million by 2035 — a remarkable 50.3% increase and a compound annual growth rate (CAGR) of 4.3%. This growth signals a significant shift in the liquid-food packaging sector, as food and beverage manufacturers deepen their commitment to shelf-life protection, food safety, and sustainable packaging solutions.

Why the Surge — Food Safety, Shelf-Life and Innovation

The expanding demand is largely driven by a rising need for extended shelf life of dairy products, as well as growing adoption of aseptic packaging across juice beverages, ready-to-drink drinks, plant-based beverages, soups, and broths. For legacy dairy producers and newer beverage brands alike, aseptic cartons offer a reliable way to preserve freshness, meet stringent food-safety regulations, and deliver convenience to consumers. As sterilization and barrier-coating technologies advance, aseptic cartons are increasingly becoming a key enabler for modern food production systems.

Simultaneously, shifting consumer preferences — for products that are safe, long-lasting without refrigeration, portable, and environmentally responsible — add further impetus to the market. The pressure for packaging solutions that combine safety, quality, and sustainability makes aseptic cartons a compelling option for both legacy brands and disruptive newcomers.

Leaders and Challengers: A Growing Competitive Landscape

Major multinationals such as Tetra Laval, SIG Group, Elopak, Amcor, and Stora Enso continue to dominate the UK aseptic-carton market, leveraging their global manufacturing scale, deep experience with food safety requirements, and established distribution networks. Their proven technologies and strong brand equity make them natural partners for large-scale dairy and beverage producers.

At the same time, this market surge opens doors for smaller and newer manufacturers, particularly those investing in next-generation barrier coatings, bio-based carton materials, and aluminium-free constructions. With the growing complexity of food-safety regulations and rising demand for specialized packaging solutions, newer players can differentiate themselves by offering agility, customization, and environmentally conscious innovations — particularly in rapidly evolving segments such as plant-based beverages, organic drinks, and niche ready-to-drink products.

Regional Dynamics & Emerging Hotspots

While demand is increasing across the UK as a whole, regions such as England lead the charge with an estimated CAGR of 4.5%, reflecting the concentration of advanced food-processing infrastructure, technology-savvy beverage manufacturers, and investment capital. Scotland, Wales, and Northern Ireland follow closely — each offering growing potential as modernization gains traction even outside traditionally dominant processing hubs. This geographic spread broadens the opportunity base beyond conventional dairy strongholds, allowing supply-chain diversification and regional production partnerships to flourish.

Innovation — The Key to Future Success

The coming decade will be shaped by integration of advanced preservation technologies and quality-monitoring systems. Suppliers and food companies are investing heavily in automated sterilization, real-time quality monitoring, and barrier enhancement systems — innovations that not only improve shelf-life but also bolster consumer trust and regulatory compliance. As these advanced systems become more accessible, even smaller manufacturers will have the chance to adopt high-performance aseptic packaging without prohibitive investment costs.

For emerging providers, the pathway to success lies in specialization — whether via bio-based materials, aluminium-free cartons, barrier-enhanced solutions, or bespoke packaging formats for niche applications. Those who can demonstrate performance, reliability, and sustainability will be well-positioned to capture market share as demand broadens from traditional dairy to juices, plant-based milks, and value-added beverages.

Why Both Established and New Players Should Take Notice

-

For established giants: The forecasted growth represents an opportunity to further expand market share, deepen technology leadership, and strengthen distribution networks across UK regions. With increasing demand for sophisticated packaging solutions, proven suppliers are likely to consolidate their positions with long-term contracts with large dairy and beverage manufacturers.

-

For new or smaller manufacturers: The evolving regulatory landscape, growing demand for sustainability, and rising popularity of niche beverages offer a fertile ground to enter the market. By embracing innovation — from novel barrier coatings to eco-friendly carton materials — they can carve out strong market niches and offer agile, customizable solutions to food and beverage producers.

Looking Ahead

As the UK moves toward a future defined by food-safety excellence, sustainability demands, and consumer-driven convenience, aseptic carton packaging is set to become an increasingly central feature of the packaging ecosystem. Both established leaders and ambitious newcomers stand to benefit — whether by scaling up legacy operations, launching new product lines, or introducing disruptive packaging technologies. The next decade promises to transform how liquid foods are packaged, preserved, and consumed in the UK.