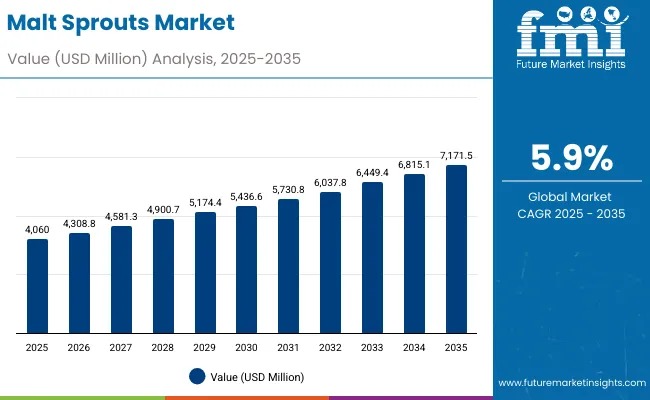

The global malt sprouts market is set for robust expansion, projected to climb from USD 4,060.0 million in 2025 to USD 7,171.5 million by 2035, reflecting a strong CAGR of 5.9%. The decade-long rise of USD 3,111.5 million underscores the role of nutritional feed ingredients in shaping modern food, feed, and agricultural ecosystems worldwide.

Growth is fueled by advanced feed formulations, greater adoption of natural protein-rich ingredients, and the shift toward automated feed processing across livestock and food manufacturing sectors. Between 2025 and 2030, the market will add USD 1.38 billion, contributing 44.3% of total decade growth, while 2030–2035 will account for the remaining 55.7%, driven by wider application integration and high-value product innovations.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-28649

Demand Strengthens Across Feed, Food & Industrial Applications

Malt sprouts—nutrient-dense rootlets separated during barley malting—continue to gain traction as manufacturers push for cost-efficient, high-performance feed inputs. With naturally elevated protein levels (20–25%), B-complex vitamins, and digestible fibers, malt sprouts have become integral to global livestock nutrition, bakery formulations, and fermentation processes.

2025 Market Structure Highlights

- Source Share: Barley dominates with ~85%, followed by wheat (~8%) and rye (~4%).

- Application Share: Animal feed leads at ~70%, food industry at ~15%, and biofuel/industrial use at ~7%.

- Regional Leaders: Europe, South Asia & Pacific, and North America steer market adoption.

- Top Companies: Cargill, Malteurop Groupe, GrainCorp, Viking Malt, Axereal.

High-Growth Regions Drive Market Acceleration

China leads with a 6.4% CAGR, supported by livestock expansion, government-backed feed modernization, and rapidly advancing agricultural infrastructure. The UK (6.2%), France (5.9%), India (5.7%), and the USA (5.6%) follow, each leveraging feed enhancement programs, processing advancements, and sustainability-oriented production systems. Germany maintains a stable 5.3% CAGR, while Brazil’s 2.4% growth reflects incremental modernization.

Why the Market is Growing: Three Core Drivers

- Rising Demand for High-Performance Feed Ingredients

Livestock producers prioritize protein-rich, digestible feed materials capable of improving productivity by 15–25%, increasing reliance on malt sprouts in poultry, dairy, and ruminant nutrition. - Global Agricultural Modernization Programs

Governments across Asia, Europe, and North America are investing in feed quality enhancements, animal nutrition training, and sustainability-focused regulations—further strengthening adoption. - Technological Advancements in Processing

Improved drying, grinding, pelleting, and extraction technologies ensure nutrient retention and consistent quality, reducing dependence on conventional protein sources.

Barley Remains the Dominant Source Segment

The barley segment accounts for 85% of 2025 revenue, supported by:

- High protein content and superior digestibility

- Compatibility with advanced processing systems

- Strong global availability and established malting infrastructure

- Proven performance across ruminant and monogastric diets

This dominance is expected to hold through 2035, as barley-based systems continue to outperform alternatives in efficiency, cost-effectiveness, and nutritional density.

Animal Feed Application Leads Global Adoption

With 70% market share, the animal feed segment stands as the industry’s backbone. Rising livestock production, demand for natural ingredients, and growing preference for performance-driven feed formulations sustain long-term growth. The food industry (15%) benefits from malt sprouts’ functional profile in bakery and snack processing, while biofuel and industrial uses (7%) continue their steady rise.

Regional Outlook: Europe Maintains Market Leadership

Europe’s malt sprouts market is projected to grow from USD 1,386.2 million (2025) to USD 2,455.3 million (2035) at a 5.9% CAGR.

- Germany leads with 20% share, supported by advanced feed processing technologies.

- UK follows at 16%, driven by sustainable farming incentives.

- France maintains a 14% share, supported by strong dairy and cattle sectors.

- Italy and Spain collectively account for 18% with growing feed innovation.

Competitive Landscape: Moderately Consolidated with Tech-Driven Expansion

Cargill, Malteurop Groupe, and GrainCorp collectively hold 25–35% market share, benefitting from established malting capacities and integrated logistics. Regional players remain competitive through:

- Localized feed processing

- Application-specific formulations

- Faster delivery cycles to agricultural hubs

Partnerships between feed technologists, agricultural cooperatives, and malt processors are expected to intensify as producers target advanced protein ingredients and automated feed systems.