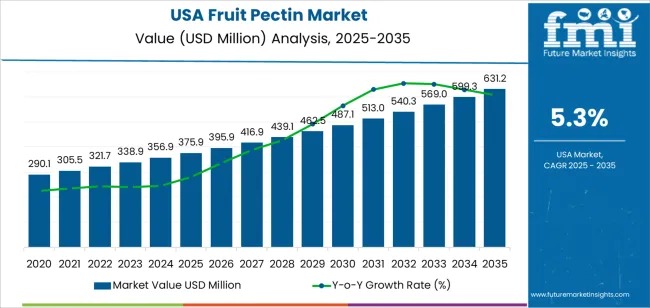

The USA fruit pectin demand is valued at USD 375.9 million in 2025 and is forecasted to reach USD 631.2 million by 2035, reflecting a steady CAGR of 5.3%. The growth is primarily driven by pectin’s role as a natural gelling, stabilising, and thickening agent across food processing, nutritional products, and specialised dietary formulations. Increased consumer preference for clean-label ingredients, wider adoption of plant-derived hydrocolloids, and ongoing innovation in functional foods are key factors supporting the market.

Fruit pectin’s versatility makes it an essential component in beverages, confectionery, and nutritional applications requiring consistent texture, viscosity control, and product stability. Its natural origin aligns with the growing demand for minimally processed, plant-based functional ingredients, which continues to strengthen its adoption across the United States.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-28841

Food Supplements Lead Consumption

Among applications, food supplements account for the largest share, with manufacturers incorporating pectin into fibre-enriched products, gummies, and chewable supplements. Pectin’s ability to form uniform matrices enhances digestibility, controlled-release properties, and stability for active ingredients. Its use in digestive health supplements and plant-based formulations reflects the growing consumer inclination toward functional nutrition and clean-label solutions.

Bakery toppings and fillings hold a significant share at 22.1%, leveraging pectin for heat-stable gels and consistent viscosity. Beverages represent 17.4% of the market, particularly in juice blends and functional drinks requiring suspension control. Dairy and frozen products contribute 14.2%, while pharmaceuticals hold 10%, utilizing pectin for controlled-release applications.

Market Dynamics and Growth Drivers

The demand for fruit pectin in the USA is primarily driven by:

- Rising preference for clean-label, plant-based ingredients.

- Expansion of reduced-sugar and functional food products.

- Steady use in jams, jellies, bakery fillings, and beverages for texture and stability.

- Availability of domestic fruit-processing by-products such as citrus and apple peels.

However, the market faces constraints, including raw-material seasonality, dependence on fruit by-products, and higher cost relative to synthetic alternatives. Some formulators may also encounter challenges when reformulating existing recipes to include pectin.

Regional Insights

Market growth varies across regions, reflecting production capacity, innovation, and consumer preferences:

- West (6.1% CAGR): Strong demand driven by fruit-based food production, functional beverages, and specialty products in California, Washington, and Oregon. Clean-label preferences and co-manufacturing support further reinforce adoption.

- South (5.5% CAGR): Demand stems from robust confectionery production and fruit-processing activities in Texas, Florida, and Georgia, particularly for gummies, fruit chews, and dairy-fruit blends.

- Northeast (4.9% CAGR): Established jams, jellies, bakery fillings, and artisanal preserves in New York, New Jersey, and Pennsylvania fuel demand, with beverage applications using pectin to stabilize fruit inclusions.

- Midwest (4.3% CAGR): Large-scale food processing, dairy, and bakery operations in Illinois, Minnesota, Wisconsin, and Ohio support steady, consistent growth.

End-User and Form Insights

The healthcare sector accounts for 42.3% of demand, primarily for dietary supplements and controlled-release formulations. Food and beverage manufacturers contribute 37.2%, leveraging pectin in jams, beverages, dairy, and functional foods. The personal-care and cosmetic industry represents 20.5%, using pectin as a natural stabilizer in gels, creams, and emulsions.

By form, original dry pectin dominates with 61.2% share, preferred for longer shelf life, consistent hydration, and ease of handling in large-scale production. Liquid pectin holds 38.8%, catering to rapid dispersion and specific textural needs.

Competitive Landscape

The USA fruit pectin market is concentrated among a few leading suppliers:

- CP Kelco – Leading with ~25.2% market share, known for consistent gel strength and reliable supply.

- Cargill Inc. – Offers standardized pectin grades for jams, beverages, and plant-based applications.

- Devson Impex Pvt. Ltd. – Cost-efficient sourcing and distribution for bakery and confectionery.

- Nestlé S.A. and Danone S.A. – Internal formulation expertise influencing broader market adoption.

Competition focuses on gelation consistency, viscosity control, thermal stability, clean-label compliance, and year-round supply reliability. The increasing focus on reduced-sugar, plant-based, and functional foods ensures continued, steady demand for pectin in the USA.

Conclusion

As the United States continues to embrace natural, functional ingredients, fruit pectin remains a critical component across supplements, bakery, beverages, dairy, and pharmaceuticals. Market growth through 2035 will be supported by clean-label initiatives, plant-based product expansion, and steady industrial adoption, making fruit pectin a reliable segment for investors and manufacturers alike.