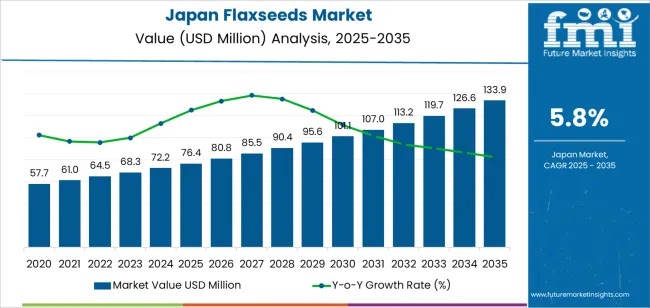

Japan’s flaxseeds demand is projected to rise from USD 76.4 million in 2025 to USD 133.9 million by 2035, advancing at a CAGR of 5.8%, according to new industry estimates. Growth is driven by the integration of plant-based, fibre‐rich ingredients into bakery items, functional foods, cereals, and supplements—supported by evolving consumer health priorities and strong adoption across Japan’s major food-processing regions.

Growing interest in omega-3 fatty acids, dietary fibre, and natural oil-rich ingredients continues to reshape product development strategies across food manufacturers, supplement producers, and health-food retailers. Japan’s high import dependency further positions global suppliers as essential partners in ensuring supply stability, quality assurance, and formulation consistency.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-28994

Whole Flaxseed Leads Market Preference

Whole flaxseed remains the most widely used product type due to its versatility across bakery formulations, cereal mixes, snacks, and home-cooking applications. Long shelf life, minimal processing requirements, and strong compatibility with industrial operations underpin its dominant share.

Its widespread availability in supermarkets, health-food stores, and online retail channels further supports routine household usage and expanding incorporation into wellness-oriented product lines.

Regional Leaders: Kyushu & Okinawa, Kanto, and Kinki

Japan’s flaxseeds demand is geographically concentrated in regions that possess strong food-processing ecosystems, robust retail networks, and efficient import channels.

Top Regions by Utilization:

- Kyushu & Okinawa (7.2% CAGR) – Leading adoption driven by functional-food manufacturers and strong port-linked import availability.

- Kanto (6.6% CAGR) – Highest retail concentration and major hub for supplement, bakery, and beverage formulation.

- Kinki (5.8% CAGR) – Strong bakery presence and rapid expansion of plant-based nutrition trends.

Food processors across these regions increasingly incorporate flaxseeds into cereals, crackers, fortified snacks, and blended nutrition solutions, shaping sustained market expansion.

Early vs. Late Growth Curve: Japan’s Demand Outlook Through 2035

From 2025–2029, demand is propelled by functional-food innovation, home-use adoption, and bakery manufacturers adding flaxseed-based ingredients into fibre-enriched formulations. Stable import availability and increasing consumer familiarity support predictable market progression.

Between 2030–2035, growth transitions into a mature phase as major manufacturers solidify product lines. Expansion is driven by improvements in milling technologies, stabilized ground-flax formats, and integration into fortified beverages and nutraceutical blends. While growth remains robust, category expansion becomes more incremental, reflecting deeper integration into mainstream health-focused diets.

Market Drivers and Restraints

Key Growth Drivers

- Rising consumer shift toward plant-based and nutrition-dense ingredients

- Increased use of flaxseeds in bakery items, cereals, health snacks, and smoothies

- Strong alignment with preventive-health, clean-label, and balanced-diet trends

- Expansion of functional beverages and supplement formulations using flaxseed oil and powder

Challenges Tempering Growth

- Price sensitivity due to import dependence and supply-chain volatility

- Limited public familiarity with how to incorporate flaxseeds in daily diets

- Competition from alternative superfood seeds such as chia and hemp

These factors influence purchase behaviour across retail and foodservice environments, modulating the pace of mass adoption.

Product & End-Use Insights

Product Preferences:

- Whole Flaxseed – 55.2% share: Long shelf life, nutrient protection, minimal oxidation.

- Ground Flaxseed – 44.8% share: Preferred for digestibility and ease of blending in smoothies, supplements, and baked foods.

Leading End-Use Segments:

- Dietary Supplements – 30.4% share

- Food Applications – 26.3%

- Pet Food – 25.7%

- Other Commercial Uses – 17.6%

Across human and pet nutrition, flaxseed’s fatty-acid profile, fibre concentration, and natural oil content form core attributes driving formulation choices.

Competitive Landscape: ADM, Cargill, and TA Foods Lead Supply

The Japan flaxseeds market is shaped by a concentrated group of global suppliers ensuring rigorous quality standards, verified nutrient profiles, and stable import flows.

Key Players Include:

- Archer Daniels Midland (ADM)

- Cargill Incorporated

- TA Foods Ltd.

- Richardson International Limited

- Johnson Seeds

ADM holds the leading market share, supported by controlled seed-cleaning operations, traceable supply channels, and consistent microbial and moisture control. Cargill and TA Foods strengthen competition through stable omega-3 content, cold-milled formats, and specialized seed grades suited for bakery, supplement, and functional-food applications.

Japan’s Flaxseed Demand Outlook

Japan’s flaxseed demand will continue to strengthen through 2035 as plant-based diets gain momentum, functional-food pipelines expand, and wellness-focused consumers increasingly select omega-3–rich ingredients. Improved distribution networks, digital retail channels, and a rising focus on clean-label ingredients will further solidify market direction.