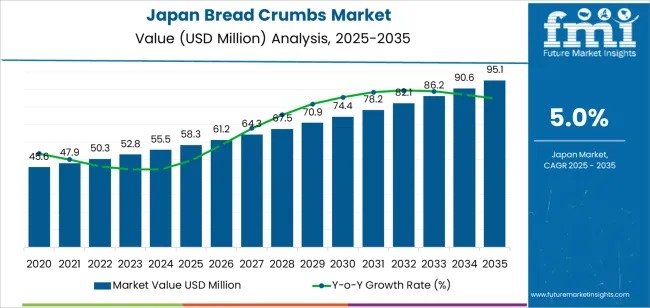

The Japan bread-crumbs market is set for steady expansion, with demand projected to rise from USD 58.3 million in 2025 to USD 95.1 million by 2035, registering a CAGR of 5.0%. Growth is reinforced by sustained use of breadcrumbs in fried foods, coated meats, frozen seafood, and ready-meal production—core components of Japan’s culinary and food-processing landscape.

Japan’s strong appetite for ready-to-cook and ready-to-eat dishes, coupled with expanding commercial kitchens and quick-service restaurant networks, continues to anchor bread-crumb consumption. Industrial processors increasingly rely on coating systems for meats, seafood, and value-added frozen food formats, supporting long-term procurement cycles. Traditional tempura preparation, bakery lines, and household fried-dish preferences further reinforce category stability.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-28954

Plain Breadcrumbs Dominate Japan’s Demand Landscape

Plain breadcrumbs remain the leading product segment due to their stable texture, uniform granulation, and predictable cooking performance. Their compatibility with Japanese home-cooking patterns—especially croquettes, patties, and soups—as well as industrial production systems makes them the preferred choice across retail and commercial channels.

Processors also prioritize attributes such as:

- Improved moisture retention

- Consistent coating adhesion

- Heat stability during frying and baking

These functional parameters shape procurement decisions for large-scale manufacturers.

Regional Growth Supported by Food-Processing Hubs

The regions of Kyushu & Okinawa, Kanto, and Kinki demonstrate the highest consumption, supported by dense clusters of frozen-food processors, cold-chain facilities, and quick-service restaurant networks. Their efficient distribution structures ensure uninterrupted supply to manufacturers and retailers.

Key Growth Regions (CAGR 2025–2035):

- Kyushu & Okinawa – 6.3%

- Kanto – 5.8%

- Kinki – 5.1%

- Chubu – 4.5%

- Tohoku – 3.9%

- Rest of Japan – 3.7%

These figures reflect strong industrial adoption of panko and related crumb varieties essential for coated proteins, ready meals, and bento components.

Why Demand Is Rising: Functional Relevance Drives Market Stability

Japan’s bread-crumbs segment exhibits a stable growth profile shaped by consistent usage across households and food-service operators. Panko remains deeply rooted in Japanese cuisine, while processors continue to scale production of coated meats, breaded seafood, and value-added frozen dishes.

Key Demand Drivers:

- High consumption of tonkatsu, ebi fry, croquettes, and katsu-based formats

- Expansion of convenience-store hot counters and chilled bento lines

- Growth of frozen seafood and meat categories requiring freeze-stable coatings

- Strong reliance on panko in nationwide restaurant chains

- Rising consumer interest in meal kits and home-frying formats

Innovation in low-oil-absorption panko, premium crumb variants, and bakery-derived textures is also shaping procurement strategies in major food-processing locations.

Market Constraints: Household Shifts and Product Alternatives

Despite wide adoption, certain structural factors moderate volume growth. Japan’s shrinking household sizes and reduced frequency of home frying limit residential crumb purchases, particularly among elderly consumers and single-person households.

Additional restraints include:

- Competition from tempura batter and karaage coatings

- Fluctuations in wheat prices influencing production costs

- Requirement for texture consistency across industrial production lines

These constraints create a predictable but controlled growth outlook for the category.

Product, Flavor, and Application Insights

Product Type Share:

- Plain breadcrumbs: 31.2%

- Panko: 27.5%

- Italian: 18.6%

- Seasoned: 13.9%

- French: 8.8%

Flavor Preference:

Unflavored/regular crumbs lead with 33.4%, reflecting Japan’s emphasis on seasoning flexibility in home and commercial kitchens.

End-Use Distribution:

- Savory dishes: 28.9% (largest share)

- Soups: 24.7%

- Prepared/ready meals: 19.2%

- Meat, poultry & seafood: 15.4%

- Patties: 11.8%

This segmentation highlights strong integration of crumbs in daily meal preparation, industrial food manufacturing, and protein-coating systems.

Competitive Landscape: Established Players Sustain Market Reliability

Japan’s bread-crumbs market is led by long-standing suppliers offering controlled granulation, stable texture, advanced milling, and nationwide distribution networks.

Key Players Include:

- Newly Weds Foods (Japan)

- Nisshin Seifun Group

- Nippn Corporation

- Showa Sangyo

- Yamazaki Baking

These companies serve industrial processors, commercial kitchens, bakeries, and frozen-meal producers with plain, panko-style, and specialized crumb variants tailored to performance requirements.

Outlook Through 2035: Resilient, Consistent, and Function-Driven

Japan’s bread-crumbs market is expected to maintain steady long-term growth as coating systems remain integral to Japanese cooking traditions and food-processing workflows. Expansion of frozen foods, restaurant chains, and bento-meal formats—combined with innovation in premium panko grades—positions the category for sustained demand over the next decade.