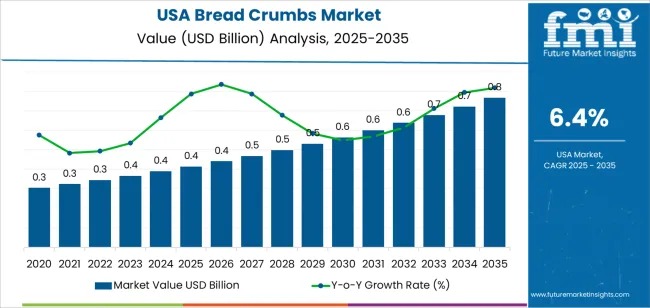

The demand for bread crumbs in the United States continues to strengthen as manufacturers, food-service operators, and retailers scale up production of ready-to-cook, breaded, and convenience meals. The USA bread crumbs market is valued at USD 0.4 billion in 2025 and is projected to reach USD 0.8 billion by 2035, expanding at a CAGR of 6.4%. Increasing utilization across processed meat, seafood, frozen meals, and home-cooking categories underpins consistent volume growth.

Demand remains strongly aligned with the rising consumption of convenience foods, stable adoption of coating systems in industrial processing, and an expanding range of clean-label, gluten-free, and seasoned crumb varieties. Performance consistency in binding, coating, and texture enhancement keeps bread crumbs indispensable across food manufacturing and food-service channels.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-29057

Plain Bread Crumbs Lead Market Performance

Among all product categories, plain bread crumbs dominate national demand, driven by their versatility and compatibility with automated processing lines. They are widely used in industrial bakeries, meat-processing plants, frozen-food facilities, and institutional kitchens for binding, coating, and textural control.

Other product formats—panko, Italian, seasoned, and fine crumbs—continue to gain traction as consumers explore global cuisines and premium, crispier breading profiles.

Quick Stats: USA Bread Crumbs Market

- Market value (2025): USD 0.4 billion

- Forecast value (2035): USD 0.8 billion

- CAGR (2025–2035): 6.4%

- Leading product: Plain Bread Crumbs

- Top growth regions: West USA, South USA, Northeast USA

- Major suppliers: Newly Weds Foods, McCormick & Company, Gonnella Baking Co., Conagra Brands

Steady Growth Supported by Low Volatility

The Growth Rate Volatility Index remains minimal throughout the forecast period, reflecting stable end-use sectors such as processed foods, QSR menus, frozen products, and home cooking. Bread crumbs serve as an essential functional ingredient with limited price elasticity, contributing to predictable procurement cycles and consistent annual growth.

Industry expansion is further supported by controlled product diversification rather than disruptive consumption shifts. Clean-label launches, gluten-free formulations, and specialty crumb varieties contribute incremental growth without destabilizing the broader demand base.

Why Bread Crumbs Demand Is Rising in the USA

Rising consumption of breaded products—such as chicken tenders, fish fillets, patties, and ready-to-cook entrées—continues to elevate crumb utilization across retail and food-service channels. Growth is further accelerated by:

- Expansion of QSR chains and their reliance on standardized crumb coatings

- Increased household cooking, supported by easy-to-use seasoned and whole-grain variants

- Premiumization of textures, including growing interest in Japanese-style panko

- Broader retail assortment, particularly in health-oriented and gourmet categories

While alternatives like batter mixes or corn-based coatings provide some competition, bread crumbs remain the most cost-effective and versatile option across industrial-scale and home-cooking scenarios.

Regional Outlook: West USA Leads at 7.3% CAGR

Bread crumb demand demonstrates strong regional variation linked to food manufacturing clusters, restaurant density, and retail distribution networks.

West USA – CAGR 7.3%

Driven by frozen-food producers, multicultural cuisine trends, and strong restaurant penetration. Panko and seasoned crumbs see rapid adoption.

South USA – CAGR 6.6%

Supported by high consumption of breaded poultry and seafood, robust frozen chicken production, and strong household usage.

Northeast USA – CAGR 5.9%

Boosted by bakery density, institutional kitchens, and strong demand for Italian-style and seasoned crumbs.

Midwest USA – CAGR 5.1%

A hub for meat processing and frozen-food manufacturing, relying heavily on crumbs as binders and coating ingredients.

Product-Type, Flavor, and Application Insights

- By Product Type: Plain crumbs lead with 31.2%, followed by panko (27.5%) and Italian-style (18.6%).

- By Flavor: Regular/unflavored crumbs dominate at 33.4%, offering recipe flexibility.

- By End Use: Savory dishes represent the largest share at 28.9%, followed by soups (24.7%) and ready meals (19.2%).

These distribution patterns reflect the importance of predictable texture, moisture control, and binding stability across American cooking routines and industrial applications.

Competitive Landscape: Leading Companies Maintain Strong Supply Networks

The U.S. breadcrumb market is shaped by mature, capability-driven suppliers with extensive manufacturing footprints and controlled milling systems.

- Newly Weds Foods leads with 21.2% share, offering precision particle-size specifications for large processors.

- McCormick & Company continues to influence retail penetration through broad distribution of panko and seasoned variants.

- Gonnella Baking Co. supplies bakery-origin crumbs to food-service and industrial buyers seeking consistent moisture and texture.

- Conagra Brands strengthens market variety through branded crumb products suited for home cooking and processed-food applications.

Collectively, these players drive innovation in gluten-free, seasoned, and clean-label crumb formulations that support the evolving needs of frozen-food manufacturers, restaurant chains, and retail consumers.