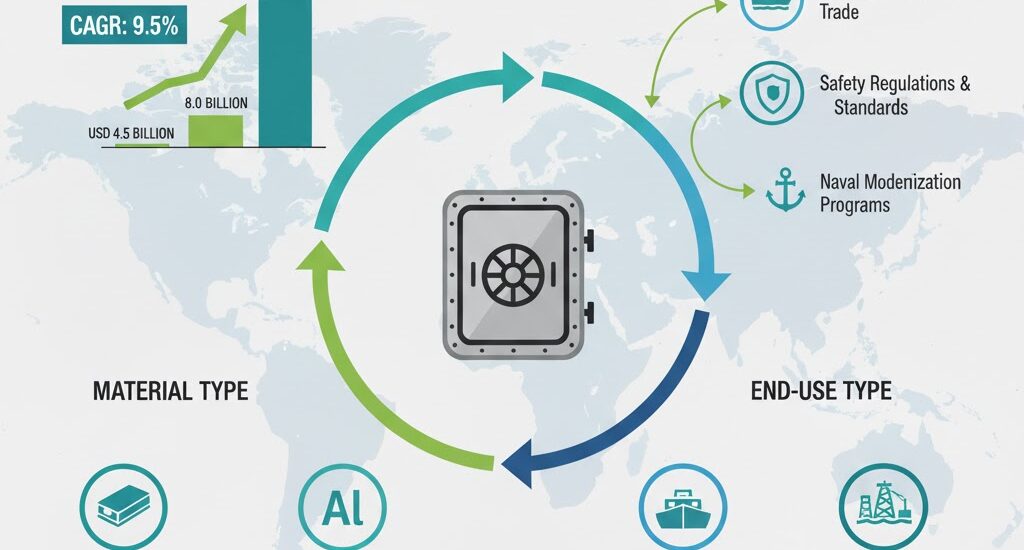

The global watertight door market is projected to rise from USD 858.7 million in 2025 to USD 1.6 billion by 2035, expanding at a steady CAGR of 6.2%, according to the latest analysis. Growing shipyard investments, stricter SOLAS compliance, and class society mandates under DNV, ABS, and Lloyd’s Register are reshaping procurement cycles and accelerating demand for automation-ready, corrosion-resistant watertight door systems.

Across APAC, Europe, the USA, and Saudi Arabia, naval and offshore sectors are re-engineering safety infrastructure. Shipyards are increasingly specifying watertight doors early in the vessel design process, integrating them with onboard automation and remote monitoring systems to enhance survivability and reduce operational downtime.

Get access to comprehensive data tables and detailed market insights – request your sample report today!

https://www.futuremarketinsights.com/reports/sample/rep-gb-8629

Key Market Highlights

• Market Value (2025): USD 858.7 million

• Forecast Value (2035): USD 1.6 billion

• CAGR (2025-2035): 6.2%

• Top Segment: Sliding Doors (≈65% share by 2025)

• Leading Application: Oil & Chemical Tankers (≈18% share by 2025)

• Fastest-Growing Country: China (7.9% CAGR)

Safety Standards Fuel Market Modernization

Since January 2024, the International Maritime Organization (IMO) has strengthened global watertight integrity requirements, mandating detailed door operation logs, remote closure testing, and fail-safe functionality-especially in passenger and offshore support vessels.

Classification societies such as DNV, ABS, ClassNK, and Bureau Veritas have followed suit, requiring tighter specifications on actuation systems, hydraulic integrity, and sensor redundancy. This is pushing shipbuilders to adopt pre-certified door systems that integrate diagnostic sensors, remote control panels, and condition-based monitoring.

“Watertight doors are now a critical component of digital ship safety ecosystems,” said a senior analyst at Future Market Insights. “Automation, predictive maintenance, and real-time door status monitoring are becoming standard features as shipyards aim for operational resilience and compliance efficiency.”

Semi-Annual Market Performance Snapshot

Performance analysis between H1 2024 and H2 2025 highlights consistent expansion:

• H1 (2024-2034): 5.5% CAGR

• H2 (2024-2034): 6.1% CAGR

• H1 (2025-2035): 5.9% CAGR

• H2 (2025-2035): 6.5% CAGR

The second half of 2025 shows the strongest acceleration, reflecting ramp-ups in offshore energy projects and shipyard orders, particularly in China, South Korea, and the United States.

Sliding Doors Dominate with 65% Market Share

Sliding watertight doors are the industry’s top choice, accounting for roughly 65% of global demand in 2025. Their space-efficient, mechanically sealed design ensures reliability in tight shipboard spaces.

Manufacturers such as Epiroc, Wärtsilä, and Kongsberg are advancing corrosion-proof sliding systems with automated actuation, remote operation, and fail-safe locking mechanisms. These systems are now standard in naval vessels, offshore rigs, and LNG carriers, supporting higher safety margins and reduced maintenance intervals.

Sliding doors are also favored in engine rooms, cargo holds, and bulkheads due to their rapid closing capabilities during emergency flooding scenarios.

Oil & Chemical Tankers Secure 18% Market Share

Oil and chemical tankers represent a key end-use category, holding an estimated 18% market share by 2025. These vessels demand watertight doors with superior chemical resistance, pressure tolerance, and mechanical strength to prevent cross-contamination and protect cargo integrity.

Industry leaders such as ABB, MAN Energy Solutions, and Konecranes are developing customized sealing solutions for tanker operators, ensuring compliance with environmental regulations and reducing maintenance downtime.

Rising global trade in petroleum and specialty chemicals, coupled with expanding tanker fleets in China, India, and the Middle East, is reinforcing demand for robust watertight systems.

Offshore Expansion and FPSO Growth to Fuel Demand

The increasing deployment of Floating Production Storage and Offloading (FPSO) vessels offers a major growth opportunity. FPSOs are emerging as cost-effective alternatives to port-based infrastructure, minimizing capital expenditure while enhancing production flexibility.

Countries such as Indonesia, Malaysia, and Australia are leading in floating terminal installations, with more than 60 units currently in operation. New regasification and liquefaction terminal projects are further boosting the use of advanced watertight systems in offshore environments.

Marine Tourism and Naval Investments Add Momentum

The steady rise in coastal and marine tourism is indirectly driving vessel demand, particularly for cruise ships, yachts, and ferries. Europe remains the largest hub, with over 200 million tourists annually along the Mediterranean coastline. As passenger vessels expand, compliance with watertight integrity standards under SOLAS Chapter II-1 becomes a key procurement driver.

Simultaneously, global naval modernization programs-including those in the U.S., Japan, India, and Saudi Arabia-are increasing demand for watertight doors designed for combat vessels and patrol ships, enhancing flood survivability and damage control.

Regional Insights

• China (7.9% CAGR): Fastest-growing market, driven by record shipbuilding output and IMO-aligned safety investments.

• India (6.9% CAGR): Expanding ship repair and coastal defense programs strengthen long-term demand.

• Italy & Japan (6.7% and 6.3% CAGR): Sustained cruise and tanker orders enhance market resilience.

• United States (6.2% CAGR): Growth supported by modernization of naval fleets and offshore energy investments.

• Saudi Arabia: Shipyard expansions and localized marine manufacturing under Vision 2030 initiatives accelerate adoption.

Purchase Full Report for Detailed Insights

For access to full forecasts, regional breakouts, company share analysis, and emerging trend assessments, you can purchase the complete report here: Buy Full Report – https://www.futuremarketinsights.com/checkout/8629

Market Structure and Competitive Landscape

The watertight door market remains moderately consolidated, with Tier 1 companies such as MML Marine, Westmoor Engineering, Ocean Group, and AdvanTec commanding 8-10% of global revenue. These leaders are characterized by large-scale production capabilities, global distribution networks, and continuous R&D investment.

Tier 2 players, including regional OEMs and niche suppliers, focus on tailored solutions for ship repair, retrofitting, and small vessel manufacturing. Although less formalized, these companies cater effectively to localized demand across Asia and Europe.

Recent Industry Developments

• June 2024 – MML Marine (Scotland): Introduced high-efficiency watertight doors featuring next-gen sealing systems for enhanced flood protection.

• August 2024 – IMS Marine Solutions (Saudi Arabia): Launched modular watertight doors with rapid-installation design to optimize yard turnaround time.

• October 2024 – BAIER Marine (USA): Unveiled smart watertight doors with integrated IoT sensors and automated flood-response capability.

• December 2024 – Westmoor Engineering (UK): Released corrosion-resistant door systems for offshore rigs, tackling durability challenges in harsh environments.

Key Companies

• MML Marine

• IMS Marine Solutions

• BAIER Marine

• Westmoor Engineering

• Ocean Group

• AdvanTec Manufacturing (Diamond Sea Glaze)

• Zhiyou Marine & Offshore Equipment (China)

• Walz & Krenzer, Inc. (USA)

• Schoenrock Hydraulik GmbH (Germany)

• Advanced Pneumatic Marine GmbH (Norway)

These manufacturers are prioritizing sensor-integrated systems, lightweight alloys, and hydraulic efficiency to meet evolving regulatory expectations and sustainability goals.

Outlook: From Compliance to Smart Safety

As shipbuilding becomes increasingly digitized, watertight door manufacturers are shifting from compliance-driven production to smart safety ecosystems. Integration with shipboard control networks, AI diagnostics, and predictive maintenance algorithms is redefining reliability standards.

With APAC, Europe, the USA, and Saudi Arabia expanding shipyard capacities and offshore investments, watertight door adoption is expected to surge through 2035, positioning the sector as a core enabler of maritime safety and sustainable fleet modernization.

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.