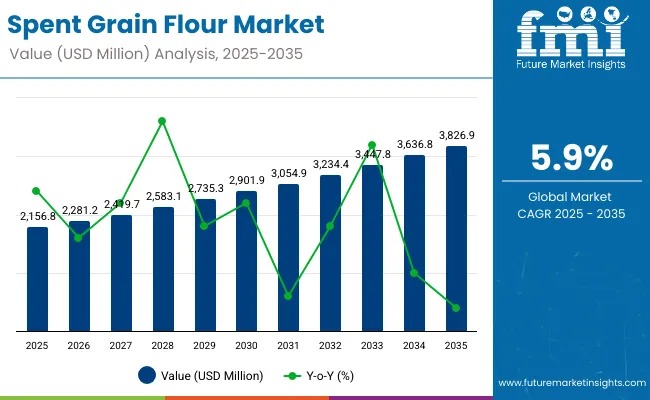

The global spent grain flour market is on a steady upward trajectory, projected to reach USD 3,826.9 million by 2035, recording an absolute increase of USD 1,670.1 million over the assessment period. Valued at USD 2,156.8 million in 2025, the industry is set to expand at a CAGR of 5.9%, driven by rising demand for upcycled food ingredients, protein-enriched formulations, and sustainable processing solutions across the globe.

Spent grain flour—derived from brewery processing—is emerging as a high-value functional ingredient due to its 18–25% protein content, abundant dietary fiber, and essential amino acids. Advanced drying and milling technologies have enabled manufacturers to transform wet spent grains into shelf-stable, nutritionally dense flour suitable for bakery, snacks, beverages, pet food, and nutraceutical applications.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-29085

Market Highlights (Last Updated: 28 Nov 2025)

- Market Value (2025): USD 2,156.8 million

- Forecast Value (2035): USD 3,826.9 million

- CAGR (2025–2035): 5.9%

- Leading Source: Barley

- Top Growth Regions: Europe, South Asia & Pacific, North America

- Key Players: ReGrained, NETZRO, Brewer’s Foods, EverGrain by AB InBev, SILO

Why Spent Grain Flour Demand Is Rising

The shift toward circular economy models and food waste reduction has accelerated global adoption of upcycled ingredients. Spent grain flour provides:

- 40–60% higher protein levels than conventional flour alternatives

- Superior water retention and texture enhancement for bakery products

- Strong alignment with sustainability mandates and clean-label trends

Government initiatives supporting protein fortification and advanced food processing technologies further strengthen market readiness. However, limited processing infrastructure in emerging markets and supply chain coordination challenges remain key restraints.

Market Outlook: 2025 to 2035

Between 2025 and 2030, the market is expected to grow from USD 2,156.8 million to USD 2,901.9 million, accounting for 44.6% of the decade’s total expansion. Growth at this stage will be shaped by rapid adoption of dried processing technologies and expanding use in bakery and snack manufacturing.

From 2030 to 2035, the market will add another USD 925 million, contributing 55.4% of the decade’s increase. This phase will witness rising demand for specialized functional ingredients, automated processing systems, and precision nutritional solutions.

Segmental Snapshot

By Source

Barley dominates with 72% share in 2025 due to its strong availability through brewing networks and superior protein-fiber profile. Wheat follows with 10%, while corn and mixed grains represent 8% and 10%, respectively.

Barley’s advantages include:

- High protein density and integrated fiber structure

- Streamlined brewery supply chains

- Reliable processing compatibility across applications

By Processing Method

Dried processing accounts for 60% share in 2025, driven by shelf-stability requirements and global demand for long-lasting functional ingredients. Wet-milled and roasted methods each hold 15%, while fermented processes represent 10%, benefiting from probiotic and digestibility enhancements.

By Application

Bakery products lead with 35% share, followed by snack products at 18%, beverages at 12%, animal feed at 15%, and pet food at 8%. Nutraceuticals and functional ingredients together account for 12%.

Country-Wise Growth Insights

Leading country growth rates through 2035 include:

- India: 7.0%

- UK: 6.4%

- Germany: 5.8%

- China: 5.7%

- USA: 5.5%

- France: 5.4%

- Brazil: 2.9%

India Leads Global Expansion

India shows the strongest momentum, driven by food processing sector expansion, bakery industry growth, and supportive government policies. Bakery products alone account for 40% of India’s demand, while animal feed and snack applications make up 25% and 20%, respectively.

Europe: Deeply Integrated Market

Europe’s market will rise from USD 740.4 million in 2025 to USD 1,316.6 million by 2035. Germany leads with 20% market share, followed by the UK (16%), France (14%), Italy (10%), and Spain (8%). BENELUX and Nordic regions show rising adoption due to innovation-driven food systems.

USA: Innovation-Driven Market

The United States continues to advance high-protein bakery and snack development using spent grain flour, supported by strong brewery partnerships and stringent product quality standards.

Key Drivers, Restraints & Trends

Drivers

- Rising global emphasis on food waste reduction and upcycling

- Protein fortification programs across major markets

- Technological advancements in drying and ingredient standardization

Restraints

- Sophisticated processing requirements

- Supply chain complexity due to varying brewery capacities

- High investment needs for advanced drying systems

Trends

- Asia-Pacific emerging as a fast-growing adoption hub

- Automation and precision processing accelerating global competitiveness

- Increasing collaborations between breweries and food manufacturers

About the Report

This press release highlights critical market insights, growth forecasts, segment performance, and regional trends shaping the global spent grain flour landscape through 2035.