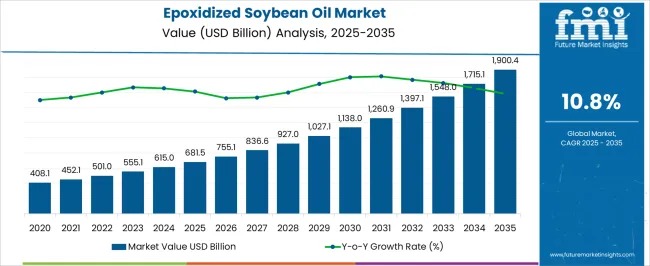

The global epoxidized soybean oil market is poised for substantial expansion, accelerating from an estimated USD 681.5 billion in 2025 to USD 1,900.4 billion by 2035, reflecting a strong CAGR of 10.8%. This surge is driven by widespread regulatory support for bio-based plasticizers, rapid industrial integration, and expanding use across PVC applications, packaging, and automotive components.

Over the next decade, ESBO will continue gaining traction as industries shift toward safer, renewable, and environmentally compliant chemical solutions. Early growth from 2025–2028 is supported by regulatory pressure favoring phthalate-free additives, while the period from 2029–2032 marks peak acceleration driven by technological advancements, industrial diversification, and growing global demand. Although slight moderation is observed in 2033–2034 due to supply constraints, long-term momentum remains robust, reinforced by rising PVC consumption and sustainable materials adoption.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-25891

Quick Market Stats

- Market Value (2025): USD 681.5 billion

- Market Value (2035): USD 1,900.4 billion

- Forecast CAGR: 10.8%

- Leading Raw Material (2025): Soybean oil (58.6%)

- Key Growth Regions: North America, Asia-Pacific, Europe

- Major Players: CHS Inc., Cargill, Nan Ya Plastics, Adeka Corporation, Valtris, Galata Chemicals, Hairma Chemicals, SHANDONG LONGKOU LONGDA CHEMICAL INDUSTRY CO., Inbra Industries

Why the Epoxidized Soybean Oil Market Is Growing

Epoxidized soybean oil is witnessing strong demand due to its wide application base and alignment with global sustainability goals. As a non-toxic, biodegradable, and renewable plasticizer alternative, ESBO offers flexibility, thermal stability, and regulatory compliance across sectors including PVC, automotive, coatings, and food packaging.

Key growth drivers include:

- Rising substitution of phthalate-based plasticizers

- Expansion of packaged food and beverage manufacturing

- Increasing adoption in medical-grade PVC applications

- Regulatory pressure favoring bio-based and low-migration plasticizers

- Technological enhancements improving purity, stability, and processing performance

Industries seeking reduced carbon footprints and safer chemical inputs are increasingly integrating ESBO into polymer stabilization, coatings, and flexible packaging films.

Market Structure and Segmental Highlights

By Raw Material

The soybean oil segment will dominate with 58.6% share in 2025, supported by its abundant availability, cost-efficiency, and high unsaturated fatty acid content that enhances epoxidation efficiency and product performance.

By Application

The plasticizers segment is projected to lead with 41.9% share in 2025, driven by rising demand for flexible PVC in construction, automotive interiors, medical devices, and packaging films.

By End-Use Industry

The food & beverages segment will command 57.9% market share in 2025 due to its crucial role in food-contact materials, shelf-life extension, and compliance with global safety standards.

Growth Outlook by Country (2025–2035 CAGR)

- China: 14.6%

- India: 13.5%

- Germany: 12.4%

- France: 11.3%

- UK: 10.3%

- USA: 9.2%

- Brazil: 8.1%

China and India dominate through large-scale polymer use and expanding manufacturing bases, while European and U.S. markets prioritize high-purity ESBO grades compliant with stringent regulatory frameworks.

Regional Insights

China:

Strong demand in plastics, stabilizers, and coatings, boosted by R&D, technology partnerships, and rapid urban development.

India:

Growing usage in flexible PVC, construction materials, and automotive applications, supported by expanding production capacity and sustainability initiatives.

Germany:

High adoption in automotive interiors, electrical insulation, and advanced coating systems, aligned with EU environmental standards.

United Kingdom:

Demand driven by flexible plastics, coatings, and industrial applications, supported by innovation in high-performance ESBO grades.

United States:

Steady demand across PVC stabilization, adhesives, packaging films, and automotive components, backed by high-purity manufacturing and regulatory compliance.

Competitive Landscape

Market competitiveness centers around product purity, epoxide content, and application versatility. Leading companies focus on R&D, sustainable feedstock sourcing, and global regulatory alignment. Key strategies include:

- High-purity ESBO grades with optimized thermal stability

- Bio-based production processes to meet sustainability goals

- Partnerships with PVC and polymer manufacturers

- Application-specific formulations for packaging, automotive, and construction sectors

Prominent players such as CHS Inc., Cargill, Valtris, and Nan Ya Plastics are expanding portfolios with specialized ESBO grades tailored for flexible PVC, coatings, and food-contact applications.