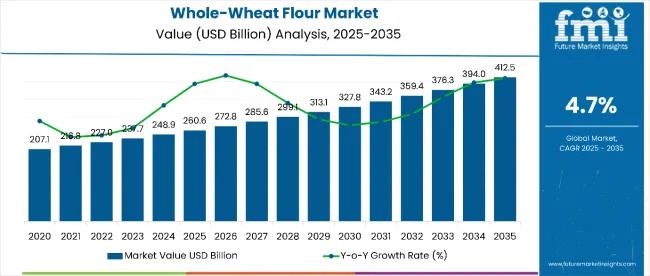

The global whole-wheat flour market continues its upward trajectory, forecasted at USD 260.57 billion in 2025 and projected to reach USD 412.46 billion by 2035, reflecting a 4.7% CAGR. The category’s growth is driven by consumers increasingly favoring high-fiber, nutritious, and clean-label ingredients over refined flour options due to rising health concerns and the popularity of whole grains in daily diets.

North America currently leads market revenue, driven by the mature bakery sector in the United States. Meanwhile, the Asia Pacific region is expected to record the fastest growth at 5.2% CAGR, led by rapidly expanding consumption in China and India. Daily staple usage and the increasing penetration of whole-wheat bread and bakery formats continue to sustain segment leadership.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-9617

Health Awareness Fuels Market Adoption

Whole-wheat flour, rich in bran and germ, is gaining traction as consumers adopt healthier carbohydrate sources. Awareness around lifestyle diseases such as diabetes, obesity, and digestive disorders is directly driving consumption in both urban and semi-urban markets. Consumers are consciously switching to fiber-dense flour options that offer better nutritional value than refined flour.

Price sensitivity and the comparatively shorter shelf life of whole-wheat flour pose challenges to mass adoption. However, advances in packaging technology, growing fortification initiatives, and education-led marketing are expected to help overcome these limitations over the next decade.

Bakery Products Drive Consumption Growth

Busy lifestyles and the rising demand for convenient, nutrient-rich ready-to-eat products are key drivers of market expansion. Whole-wheat bread, tortillas, biscuits, rolls, and ready-to-cook mixes are emerging as daily dietary staples. Quick service restaurants (QSRs), industrial bakeries, and specialty bakeries are increasingly adopting whole grain formulations to meet wellness-focused consumer expectations.

Emerging Growth Trends Supporting Industry Expansion

Manufacturers are shifting toward organic wheat sourcing, micronutrient fortification, precision milling technologies, and sustainable packaging to enhance product performance. Government-backed food fortification programs in South Asia, the Middle East, and parts of Africa are further boosting adoption.

The retail distribution landscape is rapidly advancing beyond B2B channels. Modern supermarkets now allocate branded shelf zones to whole-wheat flour, while e-commerce platforms continue to accelerate adoption in Tier I and Tier II cities. Urban consumers benefit from improved product visibility, digital accessibility, and premium packaging with clear nutritional labeling.

Consumption Patterns and Market Behavior

- The U.S. leads in per-capita adoption due to strong bakery consumption patterns.

- India’s household usage continues to grow due to its staple role as chakki atta.

- Institutional procurement, including public food programs, significantly contributes to demand in regions such as Southeast Asia and North Africa.

Infrastructure, Packaging, and Sales Channel Insights

Packaging Trends: Bags Lead with 49% Market Share

Bags dominate the market due to their cost-efficiency, moisture protection, and versatility for both small household packs and bulk commercial formats. The category benefits from strong branding potential and ongoing development of recyclable and biodegradable materials, which further support consumer appeal.

Sales Channels: B2B/Direct Sales Hold 69.4% Share

Direct procurement by bakeries, food processing units, and foodservice operators drives the dominance of this segment. Commercial buyers secure consistent supply, competitive pricing, and standardized quality specifications. Specialty bakeries and large food manufacturers are expected to strengthen long-term contractual demand through 2035.

Key Market Forces

- Growing global population and changing dietary habits increase the need for nutritious food staples.

- Rapid urbanization fuels demand for convenient, ready-to-cook products made from whole-wheat flour.

- Market leadership is concentrated, with top-tier producers holding a 65% share owing to advanced milling capacity, broad distribution, and technological investments.

Country Insights Without Table

- USA: Holds the top position in North America, supported by a large bakery sector and rising demand for multifunctional, health-enriched wheat flour ingredients.

- China: Dominates the Asian market due to a strong staple-food base (noodles, buns, dumplings), growing processed food demand, and government-backed modernization in wheat agriculture.

- UK: Drives European growth due to premium consumer preferences for wholemeal flour and expanding adoption of organic and sustainably sourced ingredients.

Key Manufacturers

The King Arthur Flour Company, Gold Medal, Bob’s Red Mill Natural Foods, Stone Ground, Georgia Organics, Heartland Mill Inc., Wheat Montana, Anson Mills, Siemer Milling Company, Hodgson Mills, Lindsey Mills, Ardent Mills, General Mills, Conagra Mills, Wiking Rogers Mills, Kishan Exports, Sunrise Flour Mill, Belize Inc., Natural Way Mills.