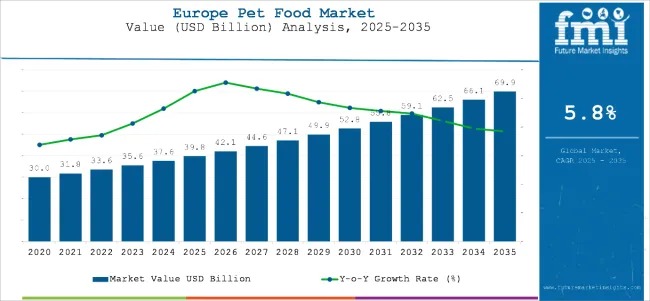

The Europe pet food market is set for strong expansion, driven by rising pet adoption, premium nutrition, and clean-label innovation. The industry is valued at USD 39.8 billion in 2025 and projected to reach USD 69.9 billion by 2035, expanding at a healthy 5.8% CAGR as consumers increasingly view pets as family members and invest in safe, high-quality diets.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-16645

Rising Humanization of Pets Fuels Premium Nutrition Shift

Pet owners across Europe are increasingly choosing organic, grain-free, fortified, and breed-specific formulations. Strong interest in digestive health, immune support, and high-protein diets is accelerating innovation in functional and tailored pet food products. Increasing disposable incomes, awareness of pet wellness, and premium care spending further highlight this shift toward nutritious and science-backed formulations.

However, high price points of organic and premium products may hinder adoption in cost-sensitive markets. Additionally, the region’s strict regulatory landscape, especially around labeling and ingredient compliance, creates operational challenges for manufacturers.

Sustainable Packaging, Digital Retail, and Alternative Proteins Drive Opportunities

Sustainability is no longer optional—bio-based and recyclable packaging materials are gaining preference among European pet owners. Online retail, direct-to-consumer (D2C) subscriptions, and personalization platforms are reshaping buying behavior. Meanwhile, insect-based and plant-based pet food, along with DNA-driven and microbiome-specific diets, represent key opportunities for long-term growth.

Notable opportunity drivers:

- Biodegradable packaging and carbon-neutral manufacturing

- AI-enabled pet nutrition apps

- Subscription-based premium deliveries

- Personalized veterinary diets

- Insect, plant, and lab-grown protein adoption

Regional Insights: Per Capita Consumption Highlights Market Maturity

Smaller countries with high pet density and premium feeding habits dominate per capita consumption.

- Ireland: 44 kg per capita annually

- Portugal & Hungary: 35 kg & 34 kg driven by urban premium retail growth

- France & Germany: 25 kg & 22 kg due to highly regulated, quality-driven markets

Strong Governance Supports Transparency and Safety

EU regulations govern product safety, labeling, and ingredient sourcing, safeguarding pet welfare and consumer trust.

Major regulatory standards include:

- Regulation (EC) No. 178/2002 – traceability and ingredient sourcing

- Regulation (EC) No. 767/2009 – labeling, additives, claims

- Regulation (EU) No. 183/2005 – hygiene and operational compliance

Additionally, the FEDIAF Code of Good Labelling Practice standardizes consumer communication to prevent misleading claims.

Country Growth Outlook (2025 to 2035)

| Country | CAGR |

| Germany | 4.8% |

| UK | 4.6% |

| France | 4.4% |

| Italy | 4.2% |

| Spain | 4.1% |

Germany drives the regional market with high demand for premium functional nutrition, while the UK leads in gourmet and natural ingredient adoption. France shows strong growth in therapeutic diets, Italy in organic clean-label products, and Spain in single-serve and convenient formats.

Segment Insights

By Nature: Conventional Leads with Accessibility

- Conventional pet food: 68% share in 2025 due to affordability, brand trust, and access.

- Organic pet food: Accelerating rapidly with growing preference for chemical-free, allergen-safe ingredients.

By Product Type: Dry Food Dominates

- Dry food holds 38% market share, backed by convenience, dental benefits, and shelf stability.

- Wet food accounts for 15% share, supported by hydration needs and older pet suitability.

Competitive Landscape

Multinational producers dominate with advanced R&D, sustainability commitments, and veterinary partnerships. Premium brands offering personalized and natural products continue to gain market traction.

Market Share by Leading Companies

- Mars Incorporated – 24%

- Nestlé Purina PetCare – 21%

- Colgate-Palmolive (Hill’s Pet Nutrition) – 16%

- Affinity Petcare SA – 11%

- Canagan Group – 9%

- Others – 19%

Key Strategic Priorities Across Top Players

- Biodegradable packaging investments

- Expansion in functional health-focused diets

- Raw, grain-free, and high-meat recipes

- AI-based customer engagement and subscription models