Future Market Insights (FMI) projects that the global wine fining agent market is on track to nearly double in size by 2035, expanding from USD 794.6 million in 2025 to USD 1,450.1 million by 2035, registering a CAGR of 6.2%. This consistent growth reflects a global shift toward premium, allergen-free, and sustainable wine production, with strong momentum coming from the APAC, European, U.S., and Saudi Arabian markets.

Wine fining agents play a vital role in ensuring clarity, stability, and sensory quality in wines, removing unwanted proteins, phenolics, and tannins that can impact flavor or appearance. As winemakers emphasize clean-label and vegan formulations, plant-based and clay-derived fining agents are reshaping global oenological practices.

Market Snapshot: Data-Driven Overview (2025–2035)

| Metric | Value |

| Market Value (2025) | USD 794.6 Million |

| Forecast Value (2035) | USD 1,450.1 Million |

| CAGR (2025–2035) | 6.2% |

| Leading Form Segment (2025) | Liquid – 61.3% Market Share |

| Leading Type (2025) | Protein-Based Agents – 57.8% Market Share |

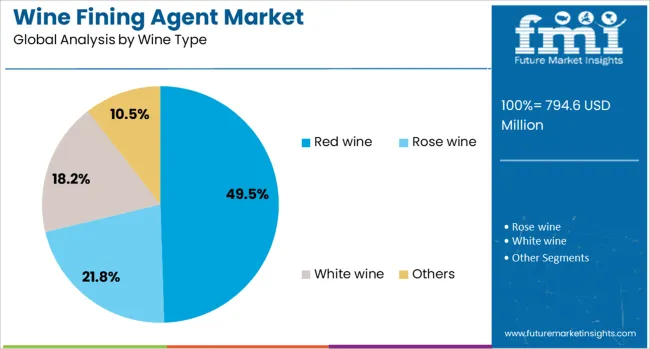

| Top Wine Type | Red Wine – 49.5% Market Share |

| Key Growth Regions | North America, Europe, APAC, Saudi Arabia |

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates: https://www.futuremarketinsights.com/reports/sample/rep-gb-23084

Global Growth Dynamics: Clarity Meets Sustainability

The market’s first five-year phase (2025–2030) will see a growth multiplier of 1.35x, lifting total value to USD 1,073.4 million. The second phase (2030–2035) contributes USD 376.7 million, or 57.5% of the decade’s incremental gains, signaling accelerated adoption of vegan and allergen-free solutions as global standards tighten.

Wineries across the world are shifting from traditional animal-derived clarifiers like casein and isinglass to plant-protein, bentonite, silica, and PVPP-based alternatives, enhancing both wine quality and sustainability credentials.

Segmental Insights

- Form: Liquid Fining Agents Lead with 61.3% Market Share

The liquid form segment remains dominant, supported by its ease of integration, uniform dispersion, and operational efficiency. Winemakers increasingly prefer liquid agents for their faster dissolution and reliable dosing, particularly in large-scale commercial operations.

Enhanced shelf stability and compatibility across wine types continue to drive adoption, particularly in high-output wineries across Europe and North America.

- Type: Protein-Based Fining Agents Capture 57.8%

Protein-based fining agents—especially plant-derived proteins—are expected to hold over half the global market. Their ability to remove haze-causing compounds and soften tannic structures makes them indispensable in premium and red wine production.

The rise of vegan-certified and allergen-reduced formulations is further driving innovation, helping producers meet stringent global labeling requirements.

- Wine Type: Red Wine Dominates with 49.5% Market Share

Red wines, which naturally contain higher tannin concentrations, remain the leading wine type segment. Fining agents are critical for balancing mouthfeel, stabilizing color, and enhancing visual appeal.

With global red wine consumption on the rise—particularly in China, the USA, and France—the demand for advanced fining agents is projected to remain robust.

Regional Analysis

APAC: China and India Lead Global Expansion

- China is projected to grow at 8.4% CAGR, driven by an expanding domestic wine sector and the widespread adoption of bentonite-based and ready-to-use formulations.

- India follows with a 7.8% CAGR, supported by boutique wineries, fruit-based wine innovation, and rising demand for organic and vegan-friendly fining agents.

Together, China and India are shaping APAC into the fastest-growing regional market, as wine culture matures and sustainability drives consumer choice.

Europe: Innovation Anchored in Tradition

- Germany (CAGR 7.1%) leads Europe’s transformation toward silica-sol and PVPP-based agents suited for white and sparkling wines.

- France (CAGR 6.5%) is modernizing traditional winemaking through precision dosing systems and plant-protein innovations, while maintaining a focus on sensory integrity.

- The United Kingdom, growing at 5.9%, is seeing widespread use of synthetic polymers and ready-to-use fining kits among small-scale wineries.

Europe continues to dominate global supply, accounting for nearly 40% of global market value, due to its advanced oenological expertise and stringent quality standards.

United States: Consistency and Clean-Label Compliance

The U.S. market, forecast to grow at 5.3% CAGR, benefits from a combination of premiumization trends and consumer preference for transparent labeling.

American wineries are transitioning from animal-protein agents toward vegan and sustainable alternatives, aligning with broader beverage clean-label movements.

Technological integration in automated clarification systems has further enhanced operational precision and product quality across California, Oregon, and Washington.

Saudi Arabia: Emerging Market for Alcohol-Free and Premium Imports

In Saudi Arabia, the demand for non-alcoholic and imported premium wines is indirectly boosting the market for fining and clarification agents used by global exporters.

With rising tourism and hospitality investments under Vision 2030, the Kingdom’s influence on regional beverage innovation is expected to grow steadily, fostering partnerships with international wine ingredient suppliers.

Need tailored insights? Request report customization to match your specific business objectives: https://www.futuremarketinsights.com/customization-available/rep-gb-23084

Key Market Drivers

- Rising Premium Wine Consumption: Increasing consumer demand for clarity and consistent quality drives fining adoption.

- Vegan & Allergen-Free Trend: Shift from egg and casein to pea protein, bentonite, and silica solutions.

- Regulatory Reinforcement: Global clarity and allergen standards, including OIV and EU norms, propel compliance-driven innovation.

- Sustainability Push: Producers pursue eco-friendly and low-residue fining processes aligned with clean-label demands.

- Technology Integration: Ready-to-use and automation-compatible fining products boost production efficiency.

Country-Level CAGR Overview (2025–2035)

| Country | CAGR |

| China | 8.4% |

| India | 7.8% |

| Germany | 7.1% |

| France | 6.5% |

| UK | 5.9% |

| USA | 5.3% |

| Brazil | 4.7% |

These growth rates reflect both mature markets (Europe, USA) embracing sustainability transitions and emerging economies (APAC) investing in modern winery infrastructure.

Market Structure and Competitive Landscape

The wine fining agent market remains moderately fragmented, with strong regional players supported by research partnerships and localized supply chains. Leading companies focus on expanding portfolios of bentonite, PVPP, activated carbon, and plant-protein formulations, catering to wineries of all scales.

Producers investing in sustainable, low-impact clarifiers and precision-engineered fining systems are positioned to capture the largest market share through 2035.

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Why Choose FMI: Empowering Decisions that Drive Real-World Outcomes: https://www.futuremarketinsights.com/why-fmi