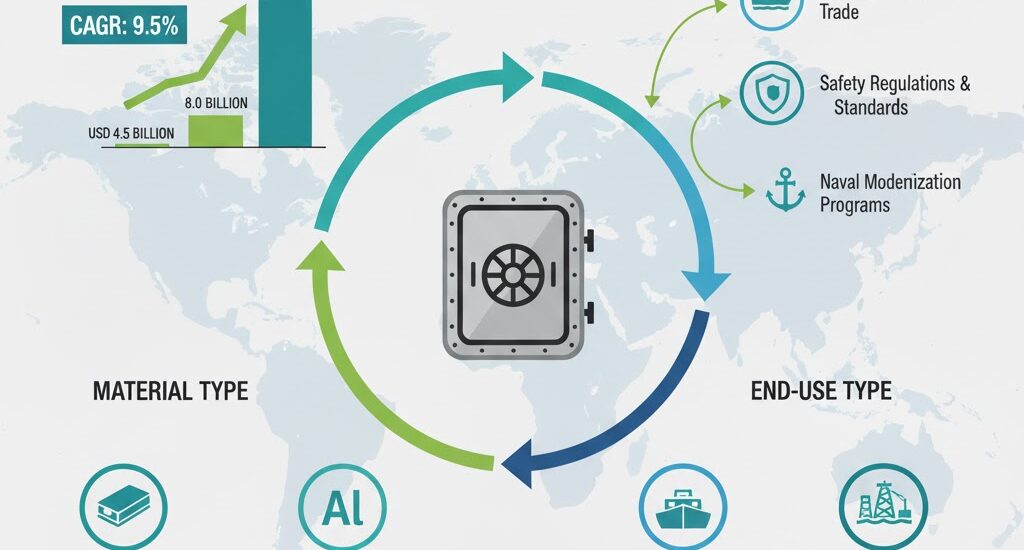

The global watertight door market is entering a period of sustained expansion, projected to grow from USD 858.7 million in 2025 to USD 1.6 billion by 2035, reflecting a CAGR of 6.2%. Rising shipbuilding activities, tightening maritime safety regulations, and accelerated adoption of automated door systems are shaping a decade of robust demand across commercial, naval, and offshore sectors.

The market is witnessing heightened specification activity at the early vessel design stage, especially for sliding and automation-ready watertight doors. Compliance with SOLAS, DNV, ABS, Lloyd’s Register, and ClassNK has become non-negotiable as shipbuilders aim to meet escalating operational safety and monitoring requirements.

Regulatory Pressure Accelerates Technology Modernization

Since January 2024, the International Maritime Organization (IMO) has reinforced regulatory scrutiny by mandating stricter reporting for door actuation cycle logs and remote closure performance—particularly for passenger vessels, offshore platforms, and polar-class ships. These upgrades are pushing shipyards to adopt pre-certified, sensor-integrated door systems capable of delivering real-time status updates, automated response mechanisms, and improved fail-safe reliability.

Simultaneously, class societies have strengthened rules governing corrosion resistance, actuation mechanisms, monitoring interfaces, and emergency manual override systems. These shifts are quickly redefining sourcing priorities and material selection across global shipyards.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates

https://www.futuremarketinsights.com/reports/sample/rep-gb-8629

Sliding Doors Lead With 65% Share as Demand Shifts Toward Automation & Space Efficiency

Sliding watertight doors are expected to retain their leadership position with approximately 65% market share in 2025. Their compact footprint, mechanical sealing efficiency, and automation compatibility have positioned them as the preferred choice for naval vessels, offshore rigs, container ships, tankers, and passenger vessels.

Manufacturers including Epiroc, Wärtsilä, and Kongsberg are advancing sliding door technologies through corrosion-proof materials, low-maintenance hydraulic and electric actuation systems, and digitally monitored sealing systems. Rapid automation in shipbuilding is further accelerating replacement and retrofit demand, especially in Asia and Western Europe.

Oil & Chemical Tankers Hold 18% Share Amid Rising Petrochemical Trade

Oil and chemical tankers are set to capture 18% of the global watertight door market by 2025, supported by rising global petrochemical logistics and high-spec safety requirements. Leading manufacturers such as ABB, MAN Energy Solutions, and Konecranes are engineering tanker-specific watertight solutions capable of withstanding chemical exposure, harsh climatic conditions, and high-pressure operational environments.

As global energy demand and specialized chemical transport routes expand, tanker fleets are increasingly adopting advanced monitoring-enabled watertight door systems to support ESG compliance, environmental protection, and accident mitigation.

Strong Regional Momentum: China Leads With 7.9% CAGR

Regional performance remains varied, with China emerging as the fastest-growing market at 7.9% CAGR (2025–2035). Growth is driven by world-leading shipbuilding volumes, modernization of naval fleets, and strategic investments in offshore exploration.

Other high-growth markets include:

- India: 6.9%

- Italy: 6.7%

- Japan: 6.3%

- United States: 6.2%

The U.S. maritime sector continues to invest heavily in fleet upgrades, offshore infrastructure, and naval modernization, while Japan’s advanced shipbuilding ecosystem is rapidly adopting automated and remote-monitored watertight systems to enhance operational resilience.

Semi-Annual Performance Trends Highlight Rising Momentum Through 2035

Semi-annual growth evaluations show a consistent upward shift in demand:

- H1 2024: 5.5%

- H2 2024: 6.1%

- H1 2025: 5.9%

- H2 2025: 6.5%

This performance indicates a 40 BPS rise across both halves of each year, reflecting expanding shipyard order books and procurement acceleration following regulatory tightening.

FPSO Developments and Coastal Tourism Fuel Market Opportunities

The expansion of Floating Production Storage and Offloading (FPSO) vessels presents a major opportunity. Indonesia currently hosts nearly 60 floating gas terminals, with new regasification and liquefaction projects emerging in Australia, Malaysia, Pakistan, and parts of Africa. FPSOs increasingly require advanced watertight doors for safety assurance, operational continuity, and storm resilience.

Meanwhile, coastal and marine tourism continues to grow, particularly across Europe, where tourist arrivals in coastal destinations exceed 200 million annually. As demand for cruise ships, yachts, ferries, and recreational vessels rises, so does the adoption of marine-grade watertight doors in new-build and retrofit applications.

Labor Shortages and Productivity Gaps Challenge Shipyards

A persistent shortage of skilled labor—especially across Europe and parts of Asia—is exerting pressure on shipyards. Markets such as China exhibit lower productivity levels, resulting in longer lead times, while Northern Europe increasingly depends on foreign labor to maintain ship repair and maintenance operations. These labor constraints may influence production timelines for watertight door installations and retrofits.

Personalize Your Experience: Ask for Customization to Meet Your Requirements

https://www.futuremarketinsights.com/customization-available/rep-gb-8629

Competitive Landscape: Tier 1 Players Capture 8–10% Global Share

Tier 1 companies, including MML Marine, Westmoor Engineering, Ocean Group, and AdvanTec, account for 8–10% of global market share. Their success is supported by wide product portfolios, global distribution networks, and strong OEM partnerships.

Tier 2 players operate locally with narrower portfolios and limited export capability, contributing to a more fragmented supply environment.

Notable Industry Developments (2024–2025)

- June 2024: MML Marine launches a high-efficiency watertight door series featuring next-gen sealing technology.

- August 2024: IMS Marine introduces modular doors for rapid installation and easier maintenance.

- October 2024: BAIER Marine unveils sensor-integrated smart watertight doors for automated flood response.

- December 2024: Westmoor Engineering debuts corrosion-resistant door systems for offshore platforms.

The watertight door market is poised for a decade of transformation, led by technology modernization, shipyard expansion, and regulatory enforcement. As safety requirements evolve and advanced monitoring technologies take center stage, procurement strategies across global shipbuilding hubs are expected to shift decisively toward pre-certified, automation-enabled watertight solutions.

Why Choose FMI: Empowering Decisions that Drive Real-World Outcomes:

https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.