Future Market Insights (FMI) projects the global Acetic Anhydride Market to grow steadily from USD 6.8 billion in 2025 to USD 8.9 billion by 2035, registering a 2.7% CAGR. The study highlights consistent expansion across Asia-Pacific (APAC), Europe, the United States, and Saudi Arabia, driven by rising pharmaceutical manufacturing, cellulose acetate production, and sustainable chemical processing initiatives.

Global Market Outlook: Stable, Predictable, and Strategically Expanding

According to FMI’s latest forecast, the acetic anhydride market will expand at a uniform pace over the decade, marking a 1.31× multiplier between 2025 and 2035. Annual market increments remain near USD 0.2 billion, reflecting steady demand from downstream applications including acetylation, pharmaceuticals, and cellulose-based fibers.

The first growth phase (2025–2030) registers a 1.15× increase, followed by a 1.14× gain during 2030–2035 — signaling low volatility, high predictability, and consistent end-use consumption. FMI analysts emphasize that this stable trajectory enables gradual feedstock alignment, process optimization, and sustainable capacity additions without supply shocks.

Subscribe for Year-Round Insights → Stay ahead with quarterly and annual data updates: https://www.futuremarketinsights.com/reports/sample/rep-gb-22963

Regional Insights

Asia-Pacific (APAC): Leadership Anchored in China and India

- China dominates global acetic anhydride production with a 3.6% CAGR, supported by integrated acetyl manufacturing hubs and large-scale cellulose acetate output for cigarette filters and textiles.

- India follows closely at 3.4% CAGR, fueled by API synthesis, textile-grade cellulose acetate, and increasing pharmaceutical exports.

- The region benefits from strong government support for chemical industrialization, process automation, and waste minimization technologies.

- Collectively, APAC contributes over 48% of global market volume, reinforcing its role as the world’s primary supply hub for acetic anhydride.

Europe: High-Purity Demand and Regulatory Precision

- Germany (3.1% CAGR) leads Europe’s growth through its advanced specialty coatings and high-performance polymer sectors.

- France (2.8% CAGR) benefits from increasing consumption in food-grade esters, perfumes, and fine chemical synthesis, while

- The UK (2.6% CAGR) relies heavily on imports for pharmaceutical-grade acetic anhydride used in aspirin, antibiotics, and diagnostic reagents.

- EU compliance frameworks emphasizing process sustainability and purity validation continue to shape competitive differentiation.

United States: Moderate Growth, High Specialization

The U.S. acetic anhydride market is forecast to expand at 2.3% CAGR, driven by pharmaceutical intermediates, acetate esters, and performance polymers. The nation’s focus on bio-based feedstock integration and on-site reagent generation underpins its transition toward low-carbon acetyl chemistry.

Recent capacity expansions and modernization of acetic acid production facilities are further enhancing cost efficiencies across the acetyl chain.

Saudi Arabia and Middle East: Industrial Scale and Diversification

The Kingdom of Saudi Arabia is emerging as a strategic regional producer, leveraging its feedstock advantage and petrochemical infrastructure. Ongoing investments in chemical diversification and local acetyl derivative plants are expected to strengthen regional self-sufficiency. The government’s Vision 2030 industrialization roadmap includes initiatives to advance green acetyl processing and catalyst optimization, positioning Saudi Arabia as a growing contributor to the global acetyl value chain.

Market Segmentation Highlights

| Segment | Key Share / Trend (2025) | Outlook |

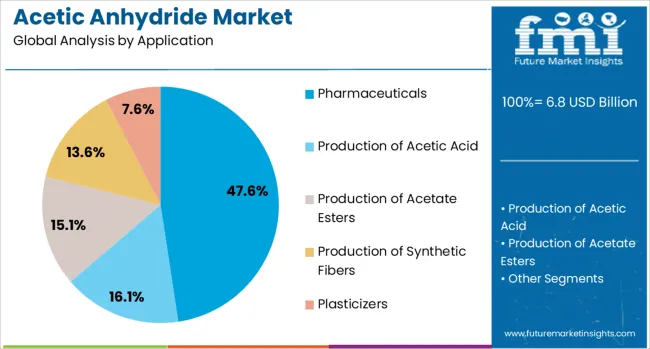

| Application | Pharmaceuticals – 47.6% | Dominant due to API synthesis (aspirin, paracetamol) |

| Purity Level | Industrial Grade – 52.3% | Preferred for large-scale chemical and textile applications |

| End Use | Textiles – 44.9% | Driven by cellulose acetate fiber production |

| Form | Liquid Form | Continues to dominate due to ease of handling in industrial processes |

Industry Dynamics

Drivers

- Expanding pharmaceutical R&D pipelines across Asia and North America.

- Heightened cellulose acetate demand in textiles, filters, and packaging.

- Growing adoption of digital process monitoring and modular acetylation units.

- Increased regulatory-driven standardization in pharmaceutical and fine chemical applications.

Restraints

- Strict regulatory controls on precursor chemicals limit flexibility.

- Safety handling and transport compliance raise operational costs.

- Supply chain fragmentation due to licensing and tracking requirements.

Trends

- Green chemistry advancements: adoption of solvent-free catalytic acetylation and reactive distillation.

- Recycling integration: closed-loop acetic acid recovery and bio-based acetyl feedstocks.

- Predictive analytics in production: real-time impurity monitoring and process automation.

Country-Level Insights (2025–2035 CAGR)

| Country | CAGR (%) | Key Drivers |

| China | 3.6 | Cellulose acetate, cigarette filters, chemical exports |

| India | 3.4 | API manufacturing, textile acetates, policy incentives |

| Germany | 3.1 | Specialty coatings, food-grade esters |

| France | 2.8 | Fine chemicals, perfumery, and cosmetics |

| UK | 2.6 | Drug intermediates, diagnostic reagents |

| USA | 2.3 | Bio-based acetylation, industrial modernization |

| Brazil | 2.0 | Emerging demand in agrochemical intermediates |

Competitive Landscape

FMI’s analysis highlights a moderately consolidated market characterized by high entry barriers, capital-intensive production, and stringent regulatory oversight. Competitive advantage is maintained through backward integration, process innovation, and regulatory compliance excellence.

- Key Differentiators: Purity control, cost leadership, and sustainable process technologies.

- Value Chain Advantage: Integrated acetic acid-to-anhydride production and data-driven manufacturing optimization.

- Future Strategies: Capacity expansions in emerging economies, technology partnerships, and adoption of renewable raw materials.

Recent Industry Developments

- April 2024 – A major North American chemical producer implemented a $0.05 per pound price adjustment for acetic anhydride, aligning with rising input costs and market dynamics.

- March 2024 – A new 1.3 million-ton acetic acid plant commenced operations in Texas, supporting the acetyl chain with one of the world’s lowest-carbon footprint facilities.

Future Outlook (2025–2035)

The acetic anhydride industry’s 2.7% CAGR outlook reflects enduring demand across pharmaceutical, textile, and specialty chemical domains. As supply chains adopt digital optimization, circular processing, and bio-based pathways, FMI expects sustained profitability and minimal volatility.

By 2035, APAC and Europe will remain the twin pillars of production and consumption, while the USA and Saudi Arabia advance as innovation and diversification centers. Strategic alignment with sustainability goals and capacity modernization will shape the next decade of the global acetic anhydride market.

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

Why Choose FMI: Empowering Decisions that Drive Real-World Outcomes: https://www.futuremarketinsights.com/why-fmi