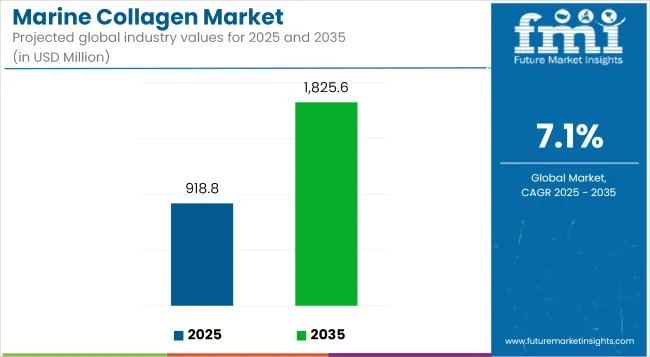

The global marine collagen market is on a strong upward trajectory, valued at USD 918.8 million in 2025 and projected to reach USD 1,825.6 million by 2035, advancing at a 7.1% CAGR. Growth is being fuelled by rising adoption of clean-label ingestibles, strong preference for pescatarian protein sources, and rapid R&D progress in high-purity peptide extraction technologies that enhance absorption and efficacy.

Clean-label wellness is reshaping the category as consumers increasingly gravitate toward collagen formats supported by traceability, sustainability, and clinically backed benefits. The market is witnessing the steady rise of recombinant and animal-free alternatives, along with the upcycling of fishery by-products—both helping manufacturers reduce environmental impact while improving margins.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-11528

Market Snapshot (2025–2035)

- Market Value 2025: USD 918.8 million

- Forecast 2035: USD 1,825.6 million

- CAGR: 7.1%

- Top Source (2025): Bones & Tendons (55.9% share)

- Leading Application: Nutraceuticals

Technology and Consumer Shifts Accelerate Adoption

Continuous advancements in enzymatic hydrolysis and deodorization have elevated product purity, driving adoption in mainstream formats such as functional powders, RTD beverages, soft chews, and cosmeceutical formulations. Marine collagen’s superior bioavailability has made it highly attractive for wellness consumers targeting joint mobility, skin health, muscle recovery, and connective tissue support.

Valorization of fish skin, bones, and scales—previously discarded as waste—is creating an efficient circular economy. Asia Pacific maintains its lead, driven by Japan, China, and South Korea, where ingestible beauty and anti-aging routines are deeply rooted.

Beyond nutraceuticals, biomedical applications are gaining momentum. Its natural compatibility and low immunogenicity make marine collagen ideal for wound dressings, surgical scaffolds, and regenerative tissue engineering. Meanwhile, regulatory pressure is pushing brands toward blockchain-enabled traceability and third-party sustainability certification.

Investment Hotspots: Animal Type and Source Analysis

Fish-Derived Collagen Retains Dominance

Fish collagen accounted for 70.6% of market value in 2025.

Key innovators include Rousselot, GELITA AG, and Nitta Gelatin Inc., each advancing high-purity peptide formulations and sustainable extraction processes.

The segment benefits from:

- Broad application versatility (powders, drinks, creams, capsules)

- Strong clinical backing

- Marketing momentum around anti-aging and mobility

Nitta Gelatin’s Japan-rooted collagen science, coupled with GELITA’s hydrolysis innovations, continues to attract health-focused consumers across Asia and North America.

Bones & Tendons Lead as Primary Extraction Sources

Bones and tendons held 55.9% share in 2025.

Global leaders such as Weishardt Group, Amicogen, and Vital Proteins rely on enzymatic hydrolysis and verified sustainable sourcing to deliver clinically trusted collagen solutions. These ingredients are increasingly used in sports nutrition, medical nutrition, and premium beauty formulations.

Key Industry Themes Shaping 2026

Rise of Animal-Free and Recombinant Collagen

Ethical consumption and environmental scrutiny are accelerating the demand for cruelty-free collagen. L’Oréal’s recombinant collagen-based Age Perfect upgrade in China underscored a major commercial breakthrough, signalling readiness for next-gen collagen innovation.

Clean-Label Transparency Drives Differentiation

Brands investing in ingredient purity, allergen-free formulations, and end-to-end transparency are gaining market share, especially in Europe and North America.

Personalization and AI-Enabled Formulations

Marine collagen is increasingly being personalized through DNA-based assessments and AI-driven nutrition profiling, improving consumer satisfaction and brand loyalty.

Country-Level Growth Insights (2025–2035 CAGR)

- United States: 4.2% — growth supported by rising demand for vegan and algae-based collagen alternatives.

- Germany: 1.4% — consumers prioritize organic, natural, and traceable collagen inputs.

- Japan: 6.3% — aging demographics drive demand for clinically validated collagen for joint and bone health.

- China: 6.0% — booming beauty sector aligned with Western beauty ideals.

- India: 7.4% — rising skincare awareness and anti-pollution solutions accelerate adoption.

Competitive Landscape and Industry Momentum

Tier-1 players such as Darling Ingredients (Rousselot), GELITA AG, and Nitta Gelatin dominate through integrated supply chains and in-house application labs. Tier-2 innovators—including bio-foundries specializing in recombinant collagen—are paving the way for cost-efficient, animal-free solutions.

Core competitive levers include:

- High-purity peptide cuts

- Low-odor extraction

- Rapid dispersibility

- QR-based batch traceability

- Expansion into joint-care, sports recovery, and medical nutrition

Capacity expansion across Asia and Latin America is also helping processors secure abundant, cost-effective feedstock from fishery by-products.

Recent Developments

- Ashland (Jan 2025): Launched collapeptyl, a marine biofunctional for advanced skin and hair health.

- GELITA: Expanded R&D in hydrolyzed marine collagen for beauty and nutraceutical sectors.

- Nitta Gelatin: Secured patents for new extraction technologies and increased production capacity across Asia and the Middle East.

Leading Companies

Ashland Inc. • Darling Ingredients Inc. • Weishardt Group • GELITA AG • Nitta Gelatin Inc. • Seagarden AS • Vital Proteins LLC • Amicogen Inc. • BHN International • Connoils LLC • Italgelatine S.p.A • COBIOSA • ETChem • Hangzhou Nutrition Biotechnology • HUM Nutrition • Titan Biotech Ltd.