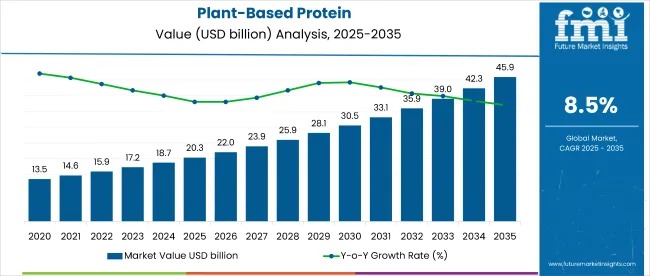

The global plant-based protein market, valued at USD 20.3 billion in 2025, is projected to reach USD 46 billion by 2035, advancing at a CAGR of 8.5%. This strong forecast reflects the worldwide shift toward sustainable, ethical, and clean-label nutrition.

Small dietary changes, increasing flexitarian lifestyles, and demand for transparent, environmentally responsible food systems are reshaping protein consumption. Plant-based proteins now contribute 1.9% of the global food & beverage market, 23.4% of the protein ingredients market, and nearly 11.8% of the functional food sector, underscoring their expanding role across applications.

Explore trends before investing – request a sample report today! https://www.futuremarketinsights.com/reports/sample/rep-gb-11442

Market Structure & Key Segment Highlights

The industry’s foundation is strengthened by rising adoption across sports nutrition, dietary supplements, bakery, beverages, ready-to-eat meals, and infant and medical nutrition. The category holds over 30% of the vegan food market and 7% of the global meat alternatives segment, driven by ongoing technological innovation and diversified product formulation.

Key 2025 Segment Leaders

- Form: Isolates lead with 41.2% share, supported by high purity, superior digestibility, and widespread use in sports nutrition and functional beverages.

- Nature: Conventional plant-based proteins command 78.3% share, favored for cost efficiency and consistent supply.

- Product Type: Soy protein holds 36.4% share, driven by its complete amino acid profile and extended use in meat analogs and dairy substitutes.

- End Use: Nutritional products represent 19.8% share, fueled by health-focused consumers and rising preventive wellness trends.

Global Market Drivers & Regulatory Influence

Growing awareness of carbon footprint reduction, animal welfare, and non-GMO, clean-label certifications is supporting product innovation. Governments across the USA, EU, India, and East Asia continue encouraging plant-forward diets through nutrition programs, sustainability policies, and support for alternative protein research. ESG-led sourcing and transparent supply chains are becoming critical pillars for competitive differentiation.

Country-Level Market Outlook

Japan remains the fastest-growing market with a projected 9.1% CAGR, benefiting from rapid advances in fermented proteins, soy-based ingredients, and senior nutrition. Germany (7.4% CAGR) and France (6.9% CAGR) maintain growth momentum driven by vegetarian populations and evolving bakery and snack formulations.

The UK, expanding at 6.3% CAGR, is seeing rising uptake of pea and wheat proteins, while the USA, projected to grow at 6.1% CAGR, leads in value contribution due to large-scale adoption across ready-to-drink beverages, functional foods, and performance nutrition.

Consumption & Distribution Patterns (2025)

Per-capita consumption varies sharply across regions:

- Japan shows strong urban demand for soy and mung bean-based proteins.

- Canada and the Netherlands purchase large volumes of isolate blends for home and institutional use.

- India demonstrates moderate uptake through soy chunks, fortified wheat blends, and lentil-based proteins.

Distribution cycles rely on dual-format storage: ambient silos for shelf-stable powders and chilled supply chains for rehydrated proteins. Malaysia, Germany, and Brazil operate mixed inventory systems, with city-level depots supporting foodservice suppliers.

Industry Trends & Challenges

Manufacturers are developing hybrid proteins by combining plant-based ingredients with precision-fermented or cultured components for improved flavor and texture. Advancements in extraction and fermentation technologies are reducing off-notes from certain plant sources.

However, price volatility of soy, peas, and fava beans—linked to climate risks and geopolitical tensions—continues to challenge cost structures. Digestibility variations and allergenicity in soy and wheat also limit formulation flexibility in sensitive consumer groups.

Competitive Landscape

The market remains moderately consolidated. Tier-1 suppliers—including Glanbia Plc, ADM, Cargill Inc., and Kerry Inc.—are strengthening global supply capability through R&D investment, sustainable extraction, and customized functional formulations. Emerging innovators like Burcon NutraScience and DuPont are advancing protein texturization and precision fermentation solutions suited for meat alternatives and dairy-free foods.

European leaders such as Roquette Frères, Cosucra Groupe Warcoing, and Royal Avebe UA leverage non-GMO sourcing advantages, while U.S.-based companies like NOW Foods, Ingredion Inc., and CHS Inc. invest in transparent supply chains and private-label partnerships.

Recent Industry Developments

- Ingredion and Lantmännen formed a long-term partnership (Nov 2024) to expand European pea protein isolate supply, focusing on innovation and high-quality ingredient delivery.

- BENEO introduced scalable hybrid and plant-protein development solutions using Meatless® texturates and faba bean protein (Nov 2024), enhancing taste, texture, and processing efficiency.