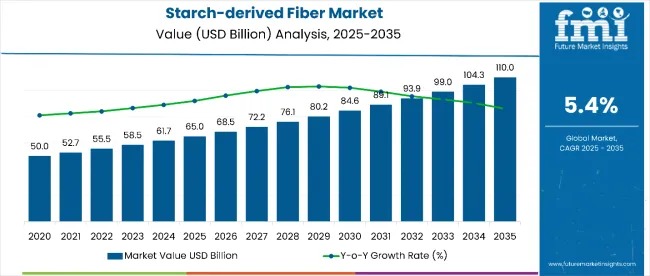

The global starch-derived fiber market, valued at USD 65.0 billion in 2025, is set to reach USD 110.0 billion by 2035, expanding at a CAGR of 5.4%. This steady upward trajectory reflects growing demand for natural, functional fiber ingredients used across food, nutraceutical, pharmaceutical, and industrial biotechnology applications. With an expected absolute dollar opportunity of USD 41.9 billion, the industry is entering a critical phase of high-value innovation and sustainable expansion.

By 2030, the market is projected to reach USD 85.0 billion, adding USD 20 billion in the first half of the decade. The remaining value uplift is forecast for 2030–2035, driven by clean-label adoption, product substitution for synthetic fibers, and a strong uptick in digestive health-focused formulations.

See How This Report Can Support Your Strategic Planning.

Request Sample Report With Complete Market Breakdowns And Growth Estimates. https://www.futuremarketinsights.com/reports/sample/rep-gb-8004

Growing interest in evidence-based nutrition and natural fiber sources positions starch-derived fiber as a preferred ingredient across functional foods, supplements, and pharmaceutical excipients. Key players—including Cargill Incorporated, Ingredion Incorporated, Dadtco Phil Africa B.V., Alliance Grain Traders Inc., Pocantico Resources, and Ixtlera—are accelerating investments in advanced biotechnology to scale production of high-purity and application-specific fiber formulations.

Market Momentum Strengthened by High-Value Applications

The starch-derived fiber industry currently represents:

- 26% of the global functional fiber ingredients market

- 18% of the specialty dietary fiber market

- 14% of the nutraceutical ingredients market

- 22% of the pharmaceutical excipient market

Its strong market share is attributed to superior digestive health benefits, clean-label compatibility, and versatility across food processing, drug delivery, and industrial biotechnology.

Continuous advancements in enzymatic modification, controlled fermentation, and extraction technologies are improving fiber bioavailability and functional efficacy. Manufacturers are also adopting sustainable sourcing models, organic certifications, and clinically validated health claims to strengthen product differentiation.

Segment Analysis: Edible/Food-Grade & Spun Form Lead Growth

- By Type – Food-Grade Segment Dominates with 67% Share

Demand is driven by rising production of functional foods, dietary supplements, and nutraceutical ingredients. Regulatory compliance and high-purity standards support expanded usage in digestive wellness formulations. - By Form – Spun Segment Commands 58% Share

Spun fibers offer uniformity and processing efficiency critical to food, pharmaceutical, and industrial applications. Their improved dispersibility and consistent performance make them the preferred choice for large-scale manufacturers.

Key Growth Drivers

- Surging Digestive Health Awareness: Consumers increasingly prioritize gut health solutions rooted in natural fibers with prebiotic benefits.

- Rapid Biotechnology Advancements: Adoption of enzymatic and fermentation systems is enhancing product purity, enabling premium-grade fiber solutions for pharmaceutical and nutraceutical clients.

- Clean-label and Sustainability Trends: Transparent sourcing, natural origins, and evidence-backed functional claims support mainstream acceptance.

- Government Support: Regulatory encouragement for functional food innovation and pharmaceutical-grade excipients is stimulating investments across emerging markets.

Country-Wise Performance: China & India Outpace Global Growth

China (CAGR 5.5%) leads the global market due to strong biotechnology infrastructure and government-backed innovation hubs across Jiangsu, Shandong, and Guangdong.

Key China metrics:

- 1.8 million tons of pharmaceutical-grade fiber produced in 2024

- 156 biotechnology facilities operating at full capacity (2023–2024)

- 68% of national production certified under international quality systems

India (CAGR 5.0%) follows with growing pharmaceutical and nutraceutical manufacturing capacity supported by clusters in Maharashtra, Gujarat, and Karnataka.

India highlights:

- 2.4 million tons processed in FY 2024

- 28% YoY growth in pharmaceutical-grade output

- 1,280 nutraceutical projects adopting Indian starch-derived fiber

Brazil (CAGR 4.2%) benefits from two-season corn harvests and cost-efficient processing, while Russia (4.0%) expands domestic capacity to improve self-reliance.

The USA (3.8%) shows stable growth driven by FDA-compliant nutraceutical and pharmaceutical demand.

Competitive Landscape

The market remains moderately consolidated, with Cargill Inc. maintaining dominant global influence through integrated biotechnology systems and extensive agricultural value chains. Other notable participants include:

- Ingredion Incorporated

- Archer Daniels Midland

- Dadtco Phil Africa B.V.

- Alliance Grain Traders Inc.

- Pocantico Resources

- Ixtlera

- HL Agro

- Viva Pharmaceutical Inc.

- Watson Inc.

High capital investment and stringent regulatory standards limit new entrants, reinforcing the competitive strength of established players.

Recent Developments

In July 2024, BENEO launched new resistant starches derived from natural corn and potato sources, supporting enhanced digestive health formulations across global nutraceutical and food sectors.

The starch-derived fiber market’s transition toward biotechnology-driven, clean-label, and clinically supported solutions underscores its long-term potential. As manufacturers align with global wellness trends and sustainable ingredient sourcing, the industry is positioned for strong and consistent growth.