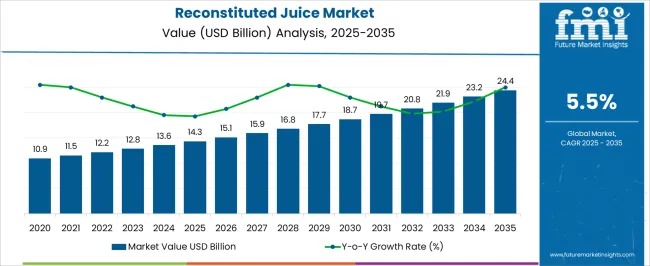

The global reconstituted juice market is set for steady expansion, with the industry valued at USD 14.3 billion in 2025 and forecast to reach USD 24.6 billion by 2035, registering a healthy CAGR of 5.5%. Demand continues to accelerate as consumers seek shelf-stable, nutritious, and affordable beverages, supported by growing urbanization and evolving dietary habits.

Rising health awareness, coupled with significant advancements in food processing and aseptic packaging, is strengthening the market’s long-term outlook. Manufacturers are increasingly turning to high-quality concentrates and water-purification technologies to retain flavor, nutrition, and safety—critical drivers of consumer acceptance across both retail and foodservice sectors.

See How This Report Can Support Your Strategic Planning. Request Sample Report With Complete Market Breakdowns And Growth Estimates. https://www.futuremarketinsights.com/reports/sample/rep-gb-8001

Market Overview and Segment Insights

Shorter supply chains, cost-effective production methods, and wider distribution networks have made reconstituted juice a preferred choice for households, retailers, and institutional buyers. In 2025, the conventional category will dominate with a 72% share, supported by affordability and easier sourcing. Organic juices, while still niche, are growing in premium retail channels.

Key Segment Highlights

By Nature

- Conventional reconstituted juice: 72% share in 2025

- Organic gaining traction in Europe and North America

- Certification challenges slow organic scale-up

- Expansion of premium wellness retail supports growth

By Ingredient

Fruit-based formulations command a 67% market share, with citrus, apple, and blended fruit juices leading consumer preference. Vegetables and exotic fruit blends are increasingly adopted in functional and detox beverages.

By End Use

Retail/household consumption remains dominant at 66% share in 2025. Hotels, restaurants, and catering (HoReCa) are expanding usage through juice cocktails, smoothies, and wellness drinks. Food manufacturers continue to rely on reconstituted juice for yogurts, confectionery, and ready-to-drink mixes.

By Packaging

Tetra Pak formats lead the category with a 42% share, favored for long shelf life and logistical convenience. Bottles (PET, glass) are gaining traction in premium juice lines, while bulk formats cater to industrial users. Sustainable packaging is emerging as a major differentiator.

By Distribution Channel

Indirect/B2C channels—including supermarkets, hypermarkets, specialty stores, and e-retail—account for 58% of total sales. Online subscription models geared toward functional and vitamin-enriched beverages continue rapid adoption.

Top Market Trends

- Rising demand for affordable, inflation-resistant juice options

- Increased adoption of vitamin-fortified and low-sugar formulations

- Growth in exotic fruit blends, targeting millennials and urban consumers

- Expansion of on-the-go, single-serve packaging formats

Market Challenges

- Perceived lower quality compared with fresh or NFC juices

- Regulatory pushback on sugar content and preservatives

- Seasonal inconsistency in fruit concentrate sourcing

- Heightened competition from organic, cold-pressed, and NFC juices

Country-Wise Performance

United States

The U.S. market will grow at 4.9% CAGR, driven by strong retail penetration and widespread use of imported fruit concentrates. Private-label expansion in mass retail continues to boost affordability and accessibility.

United Kingdom

Expected to grow at 4.6% CAGR, driven by increasing preference for low-sugar, clean-label beverages and higher adoption of recyclable packaging formats.

Germany

Germany’s market will expand at 4.8% CAGR, supported by robust demand for organic and reduced-sugar juice lines. Local processors leverage EU-sourced concentrates and cold-filled packaging technologies.

France

Predicted CAGR of 4.7%, supported by demand for premium fruit blends, botanical extracts, and probiotic-infused juices. Cafés and breakfast chains drive significant consumption.

Japan

Japan will grow at 4.4% CAGR, backed by the popularity of single-serve packs, fortified juices, and a strong vending retail infrastructure.

Competitive Landscape

The market is moderately consolidated, led by players such as PepsiCo Ltd., Citrosuco S.A., Citrus World Inc., The Daily Juice Company, and Louis Dreyfus Company B.V. Companies are increasingly focusing on:

- Functional, clean-label, and reduced-sugar innovations

- Sustainable concentrate sourcing and carbon-neutral operations

- Private-label partnerships and global supply chain optimization

Recent news indicates stronger demand for PepsiCo’s long-shelf-life beverages, while AGRANA continues expanding its clean-label and natural ingredient portfolio to meet Europe’s sustainability and health-oriented requirements.