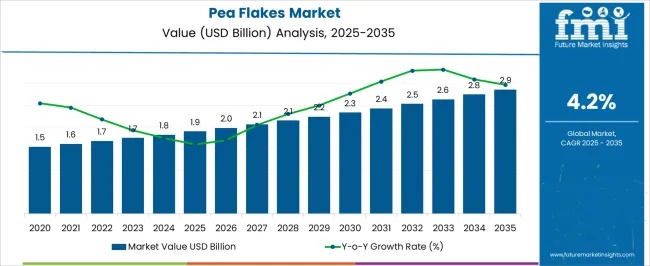

The global pea flakes market, valued at USD 1.9 billion in 2025, is projected to reach USD 2.9 billion by 2035, expanding at a CAGR of 4.2%, according to the latest industry assessment. Demand continues to strengthen as consumers prioritize plant-based proteins, clean-label ingredients, and nutrient-dense foods. Additionally, the pet food sector’s rising requirement for high-protein, digestible ingredients is pushing pea flakes into mainstream formulations across the globe.

In 2025, yellow pea flakes accounted for 70% of the market, solidifying their position as the leading type, while food processing applications made up 50% of overall demand. The Asia-Pacific region, led by Japan at 4.6% CAGR, remains the fastest-growing market due to strong interest in functional and protein-rich foods.

See How This Report Can Support Your Strategic Planning.

Request Sample Report With Complete Market Breakdowns And Growth Estimates. https://www.futuremarketinsights.com/reports/sample/rep-gb-8000

Strong Demand Backed by Nutritional and Functional Benefits

Pea flakes are increasingly recognized for their high protein, fiber, and micronutrient profile, strengthening their use across health-focused snacks, cereals, soups, and ready meals. As clean-label trends intensify, manufacturers continue integrating pea flakes to meet rising expectations for natural, allergen-free, and minimally processed ingredients.

The market also benefits from strong traction in pet nutrition, where pea flakes serve as a sustainable, digestible, and protein-dense addition to premium pet foods. This dual appeal across human and animal nutrition continues to widen the market’s footprint.

Market Position Within Parent Industries

Pea flakes now represent:

- 6.2% of the plant-based protein market

- 7.8% of the pulse ingredients market

- 3.4% of the functional food ingredients segment

- 4.6% of the plant-based food market

- 5.1% of snack ingredients demand

These shares highlight pea flakes’ growing strategic role across multiple high-growth ingredient categories.

Segment-Level Insights

By Nature – Conventional Pea Flakes Hold 75% Share

Cost-effectiveness, large-scale supply, and suitability for commercial feed applications keep conventional pea flakes dominant.

Key drivers include:

- Lower production and sourcing expenses

- Strong adoption in livestock, poultry, and aqua feed

- Higher scalability for mass-market demand

- Widespread use across Asia, Latin America, and Eastern Europe

By Type – Yellow Peas Lead with 70% Share

Yellow pea flakes remain favored for their superior protein content and digestibility, making them a staple in plant-based and fortified food formulations.

By End-User – Food Processing Captures 50% Share

This segment’s leadership is driven by extensive application in:

- Healthy snacks

- Soups and instant dishes

- Baked goods

- Functional food blends

By Packaging – Pouches Dominate with 40% Share

Pouches continue to gain traction due to ease of handling, cost efficiency, and compatibility with retail and e-commerce channels.

By Channel – Online Retailers Hold 30% Share

Growth in e-commerce, direct-to-consumer models, and health-focused digital retail is accelerating online purchases of pea flakes.

Country-Level Highlights

Japan (4.6% CAGR) – Strongest global growth, driven by functional foods, aging population needs, and clean-label adoption.

USA (4.5% CAGR) – Largest global consumer; rising fitness trends and organic food interest drive momentum.

Germany (4.2% CAGR) – Sustainability leadership supports steady expansion.

France (4.1% CAGR) – Growing interest in natural, protein-rich plant-based foods.

United Kingdom (3.8% CAGR) – Veganism and nutritional awareness fuel demand despite slower growth.

Competitive Landscape

The pea flakes market is moderately fragmented, with key players including Garden Valley Foods, JR Farm, Gemef Industries (Sotexpro), BP Milling, Green Foods LLP, and PE Levona. Companies are expanding production capacity, refining pricing strategies, and forming partnerships with food and pet food manufacturers to strengthen their global presence.

Recent industry developments include:

- Danone’s Alpro launching a child-focused plant-based line in 2025 to address rising parental demand for healthier options.

- Nutiva Inc. enhancing its organic and non-GMO product portfolio, positioning itself as a leader in clean-label, plant-based ingredients.