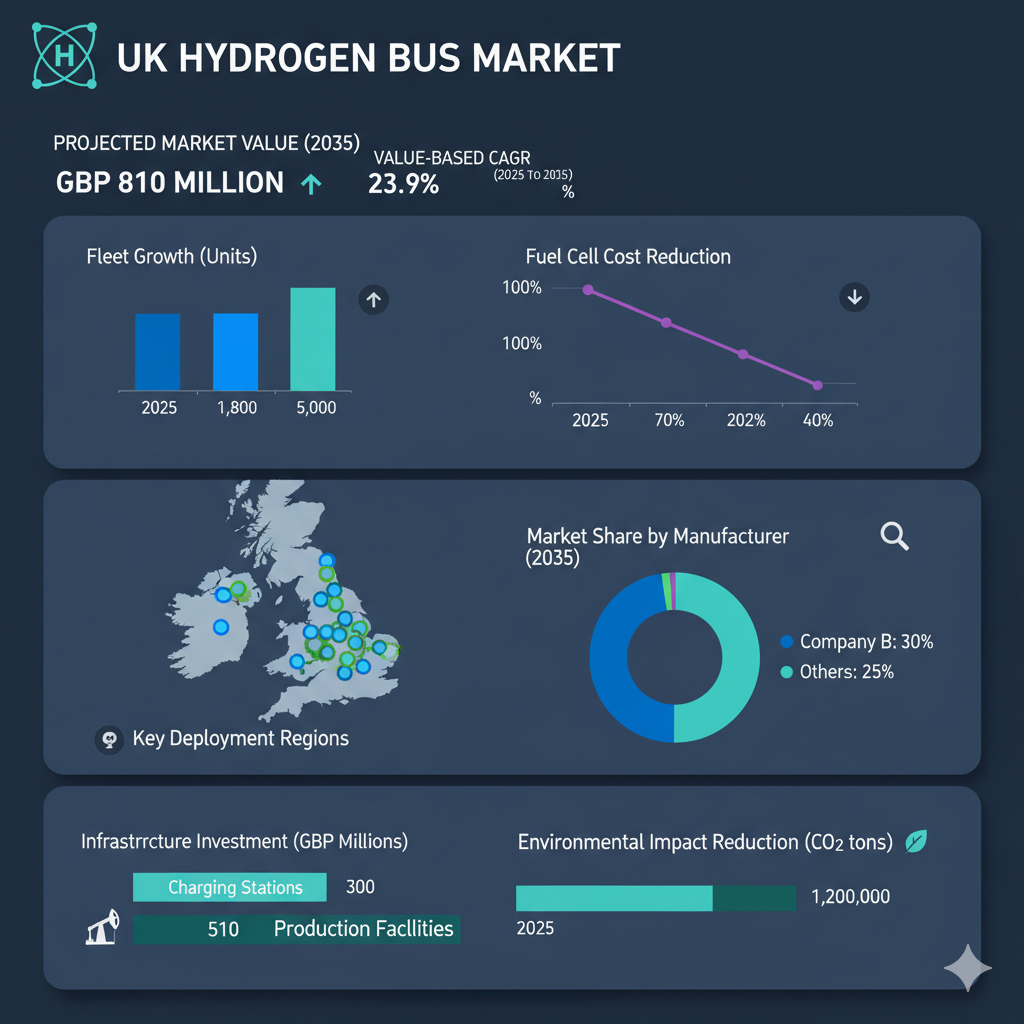

The UK’s hydrogen bus market is accelerating at break-neck speed, and both established manufacturers and new entrants are positioning themselves to ride the wave. According to the latest industry analysis, the market is forecast to grow to GBP 810 million by 2035, with a compound annual growth rate (CAGR) of 23.9 % from 2025 to 2035.

A Compelling Growth Story – and the Opportunity for Manufacturers

The shift to zero-emission transport is no longer just an aspiration—it’s a clear business imperative for the UK. With government targets to reduce carbon emissions by 68 % by 2030 and achieve net-zero by 2050, hydrogen-fuelled buses are becoming a cornerstone of the country’s sustainable public-transport strategy.

The growth is driven by three key factors: the maturity of hydrogen fuel-cell technology, rapid expansion of hydrogen refuelling infrastructure, and a supportive regulatory environment. For manufacturers—whether long-established vehicle producers or newcomers in the hydrogen mobility space—this is a pivotal moment to scale up, innovate, and capture a share of a rapidly growing market.

Strength from the Veteran Players

Global leaders such as Toyota Motor Corporation, Ballard Power Systems, and Siemens AG have long been recognized for their advancements in hydrogen fuel-cell systems and related infrastructure. These companies bring decades of technological experience, production scale, and brand credibility—qualities that transit authorities value when making procurement decisions.

They are at the forefront of advancing Proton Exchange Membrane Fuel Cell (PEMFC) technology, which dominates the current UK market. PEMFC systems are efficient, durable, and increasingly cost-effective due to large-scale R&D and manufacturing improvements. For these industry veterans, the road ahead lies in deepening collaborations with UK transit agencies, integrating their fuel-cell technologies into domestic manufacturing pipelines, and delivering turnkey hydrogen-bus systems that include fuel-cell stacks, chassis, and service infrastructure.

Emerging Players Forging New Pathways

On the domestic front, pioneering UK bus manufacturers such as Wrightbus and Alexander Dennis Limited (ADL) are spearheading the development and production of hydrogen buses while simultaneously investing in refuelling infrastructure. Their early adoption of hydrogen technology has positioned them as leaders in delivering sustainable mobility solutions tailored for the UK market.

Meanwhile, a new wave of start-ups and research-driven companies is entering the sector, developing next-generation solutions such as Solid-Oxide Fuel Cells (SOFC) and Direct-Methanol Fuel Cells (DMFC). Although still in the early stages of commercialization, these emerging technologies promise improved energy efficiency, longer operational lifespans, and simpler fuel logistics. For new manufacturers, this represents a chance to collaborate with established firms or carve out niche segments by introducing differentiated, future-ready innovations.

Technology & Infrastructure – The Twin Engines of Growth

Technological advancement remains the driving force behind the UK hydrogen bus industry. While PEMFC technology currently leads, continued R&D is expected to deliver improvements in cost, performance, and serviceability—particularly for high-capacity buses exceeding 250 kW.

At the same time, hydrogen refuelling infrastructure is expanding rapidly. Refuelling hubs in major transit cities such as London, Birmingham, and Manchester are transforming the feasibility of large-scale hydrogen-bus operations. For manufacturers, this evolution means the market is shifting from pilot projects to full-scale deployment, where consistent operations and reduced total cost of ownership will fuel even greater adoption.

What This Means for Manufacturers

- For Established Manufacturers: Leverage technological leadership and brand recognition to secure large-scale contracts. Invest in local supply chains, after-sales networks, and integrated offerings that combine vehicle manufacturing with fuelling infrastructure and maintenance services.

- For New Entrants: Focus on innovation and strategic partnerships. Collaborate with established OEMs or target emerging sub-segments such as mid-capacity buses (150-250 kW) or alternative fuel-cell chemistries to build a competitive foothold.

- For All Manufacturers: Align with UK government initiatives such as the Zero Emission Bus Regional Areas (ZEBRA) scheme, which supports hydrogen bus adoption through grants, subsidies, and infrastructure funding.