The European Union’s polysulfide market is entering a new phase of moderate yet steady expansion, projected to rise from USD 894.6 million in 2025 to USD 1,190.6 million by 2035, at a compound annual growth rate (CAGR) of 2.9%. Despite the modest pace, the upward trajectory underscores polysulfide’s enduring relevance across aerospace, construction, coatings, and industrial processing — industries that rely on its hallmark chemical resistance, elasticity, and long-term durability.

While newer materials like polyurethane and silicone continue to compete for market share, polysulfide remains irreplaceable in high-specification applications where safety, chemical integrity, and lifecycle performance outweigh cost advantages. As Europe’s industrial base emphasizes performance reliability and compliance with stringent regulatory standards, polysulfide demand is expected to maintain its steady climb across the next decade.

Aerospace and Transportation Drive Core Consumption

At the heart of Europe’s polysulfide demand is the aerospace and transportation segment, which represents 32% of total consumption in 2025, forecasted to reach 33% by 2035. The aerospace sector’s dependence on polysulfide sealants for fuel tank integrity, fuselage sealing, and pressurized joints continues to be a major demand anchor. These sealants’ resistance to aviation fuel, flexibility under pressure, and adhesion to aluminum and composite substrates make them indispensable in ensuring aircraft safety and performance.

European aerospace giants — including Airbus, Dassault Aviation, and Leonardo — rely on certified polysulfide materials meeting stringent European Aviation Safety Agency (EASA) and OEM requirements. Every aircraft maintenance, repair, and overhaul (MRO) program in Europe contributes to recurring consumption, as polysulfide sealants must be reapplied during critical maintenance cycles.

This consistency of MRO activity — spanning both commercial and defense fleets — provides a stable and long-term base of demand, even during cyclical downturns in new aircraft production. Moreover, as the EU continues investing in aviation sustainability and fleet modernization, certified polysulfide producers are expanding partnerships to ensure supply chain resilience for aerospace materials.

Construction Sector Strengthens as a Secondary Growth Pillar

Following aerospace, construction applications remain a solid pillar of polysulfide demand across Europe. The material’s proven performance in expansion joints, insulating glass units, and waterproofing systems sustains its popularity among contractors and architects focused on longevity and weather resistance.

Construction firms across Germany, France, Italy, and the Netherlands increasingly specify polysulfide-based sealants for building envelopes, bridges, tunnels, and civil infrastructure where temperature fluctuation and chemical exposure challenge long-term integrity. The product’s flexibility and resistance to ultraviolet degradation ensure reliability across decades of service.

Manufacturers are innovating with low-VOC and solvent-free formulations to meet European Green Deal directives and the tightening emissions standards imposed by REACH and national building codes. These advancements have helped polysulfide products retain their relevance in modern green construction, ensuring compatibility with sustainability certifications such as BREEAM and LEED.

Thiokols Continue to Dominate Product Chemistry

By product chemistry, thiokol-based polysulfides lead the EU market with 58% share in 2025, expected to reach 59% by 2035. Their superior chemical and fuel resistance has secured their place as the material of choice for aerospace sealants and high-performance construction applications.

Thiokols’ high viscosity control, consistent cure rates, and customizable formulations — ranging from brushable to extrudable grades — enable precise application in confined or demanding environments. Their well-documented performance in fuel resistance testing, accelerated weathering, and mechanical flexibility has earned them long-term certification across multiple European aircraft and construction programs.

This segment’s dominance reflects the technical sophistication required in EU industries, where long qualification cycles and strict compliance protocols favor established chemistries over experimental alternatives.

Regional Outlook: Germany, Spain, and the Netherlands Lead

Within the EU, Germany remains the largest consumer, holding an estimated 24.1% market share in 2025, supported by its dual strength in aerospace manufacturing and construction engineering. The Airbus facility in Hamburg, coupled with extensive civil infrastructure projects, generates consistent demand for both aerospace and construction-grade polysulfides.

France, with Airbus headquarters in Toulouse, is another significant contributor, expected to grow at a 3.1% CAGR through 2035. The country’s integrated aerospace ecosystem, complemented by active civil construction, keeps polysulfide consumption steady.

Italy follows closely with a 3.2% CAGR, supported by its expanding aerospace component manufacturing and infrastructure development. Meanwhile, Spain and the Netherlands, each growing at 3.3% CAGR, are emerging as competitive growth centers — Spain with its Airbus final assembly lines and the Netherlands with its emphasis on aerospace component manufacturing and large-scale infrastructure projects.

The Rest of Europe segment, growing at the highest 3.4% CAGR, demonstrates increasing industrial maturity, reflecting investment in aerospace facilities and urban development across Eastern and Northern Europe.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/27232

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-27232

Supply Dynamics and Production Challenges

Despite its industrial importance, the EU polysulfide market faces persistent supply-side challenges. Production remains concentrated among a limited number of integrated chemical firms, leaving the supply chain vulnerable to feedstock price volatility and regulatory constraints.

Dependence on sulfur and alkali precursors means that fluctuations in global raw material pricing can directly affect cost structures. Additionally, compliance with stringent EU environmental and occupational safety regulations constrains production scalability. Manufacturers are therefore investing in process automation, emission control technologies, and sustainable raw material sourcing to mitigate these challenges.

Scaling up production capacity is complex and capital-intensive, as aerospace-grade polysulfides must meet strict viscosity and curing performance requirements verified through aerospace certification protocols. Recycling and reprocessing efforts remain nascent, making virgin production the dominant supply mode — a trend manufacturers are cautiously addressing through R&D in longer-lifecycle formulations and advanced curing systems.

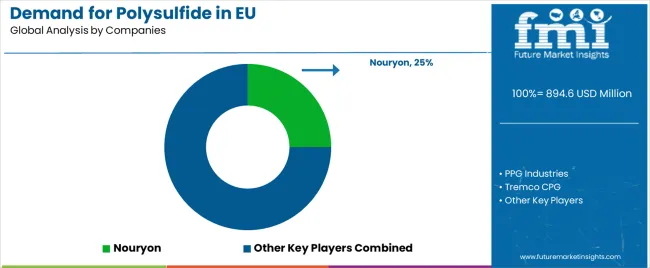

Competitive Landscape: Established Leaders and New Entrants

The European polysulfide industry is led by a mix of established multinational chemical firms and emerging regional specialists. The top three players — Nouryon, PPG Industries, and Tremco CPG — collectively command about 60% of the market, while the remainder is fragmented among regional sealant manufacturers and niche aerospace suppliers.

Nouryon, holding approximately 25% market share, anchors its leadership through its Thioplast® polysulfide brand, widely recognized in both aerospace and construction sectors. The company’s vertically integrated European production infrastructure and deep technical partnerships with major aerospace OEMs ensure a consistent supply of certified materials.

PPG Industries follows with around 20% share, leveraging its PRC-DeSoto® aerospace sealant brand, known for decades of flight-proven reliability. Its Hamburg facility plays a central role in European operations, supplying commercial and defense aerospace programs across the continent.

Tremco CPG, with roughly 15% share, remains a specialist in construction and waterproofing sealants, offering comprehensive building envelope solutions and technical service support to contractors across Europe.

Meanwhile, smaller regional manufacturers and new entrants are focusing on custom formulations and sustainable production methods to carve niches in specialty applications. These companies, often emphasizing low-emission products and innovative curing technologies, are expanding into aerospace-adjacent and renewable energy sealing markets, ensuring healthy competitive diversity.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube