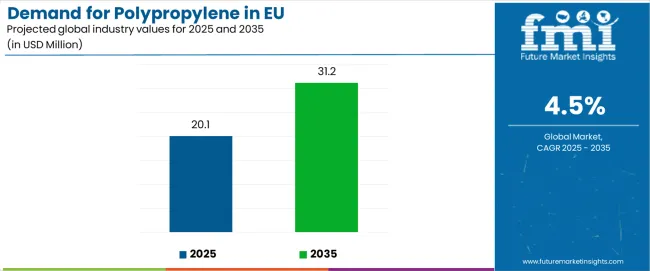

The demand for polypropylene (PP) in the European Union is forecast to expand from USD 20.1 million in 2025 to USD 31.2 million by 2035, advancing at a CAGR of 4.5%. This growth underscores polypropylene’s vital role in Europe’s packaging, automotive, and industrial manufacturing sectors. However, the market outlook remains closely tied to regulatory developments, circular economy initiatives, and the evolving landscape of material innovation.

As both established petrochemical giants and emerging regional players invest in technological integration, feedstock efficiency, and recycling infrastructure, the European polypropylene market is undergoing structural transformation aimed at resilience, sustainability, and innovation.

Demand Drivers: Lightweight Performance Meets Circular Innovation

Polypropylene’s versatile performance characteristics—from stiffness and impact strength to heat and chemical resistance—make it indispensable for packaging converters, automotive component manufacturers, and industrial molders across the EU.

The polymer’s low weight-to-strength ratio, chemical inertness, and cost efficiency continue to drive adoption in high-volume applications, while recyclability advantages enhance its long-term appeal in an era increasingly defined by sustainability mandates.

Advanced polypropylene grades—such as clarified random copolymers, high-melt-strength (HMS) variants, and recycled-content formulations—are becoming essential for packaging converters and OEMs seeking compliance with EU directives on recycled content and extended producer responsibility (EPR).

As sustainability becomes a central purchasing criterion, PP producers are embracing circular design principles and forming partnerships with recycling and waste management firms to secure recycled resin streams that meet quality and regulatory standards.

Industry Challenges: Feedstock Volatility and Regulatory Pressure

Despite steady growth prospects, feedstock volatility and regulatory constraints remain defining challenges. Polypropylene’s production depends heavily on propylene, a derivative of crude oil and natural gas, making the industry vulnerable to oil market fluctuations.

Manufacturers like LyondellBasell and TotalEnergies face pressure to balance raw material costs while maintaining competitiveness in downstream applications where cost pass-through is limited. Similarly, currency fluctuations within the Eurozone influence both import-dependent nations and exporters, adding complexity to pricing and profit management.

Additionally, substitution risks from bioplastics, recycled polymers, and advanced composites could reshape demand patterns, particularly as the EU accelerates its plastic waste reduction goals. Policies enforcing non-recycled plastic taxation and recycled content quotas will play a decisive role in determining future growth trajectories.

Segmental Overview: Packaging Dominates, Homo-Polymer Leads

By product type, Homo-Polymer (HP) remains the largest segment, accounting for 58% of total EU polypropylene demand in 2025. Its dominance is attributed to excellent stiffness, high heat resistance, and cost-effective processing—key properties for rigid packaging, automotive parts, and fiber products.

While HP will maintain its leadership, its share is expected to slightly decline to 56% by 2035, as copolymers and thermoplastic polyolefins (TPOs) gain ground in applications requiring enhanced toughness or transparency.

In terms of application, packaging holds a 35% market share in 2025, reaffirming its status as the largest consumer segment. This share will remain resilient despite a gradual shift toward recycled and biodegradable alternatives. The segment’s growth is supported by innovations in mono-material packaging, lightweighting technologies, and clarified PP grades that enhance transparency and recyclability.

Regional Insights: Diverse Growth Across the EU

The Rest of Europe region leads EU polypropylene demand, expanding at a CAGR of 5.0%, supported by growing manufacturing capacity and investments in packaging and automotive sectors. Spain follows at 4.6% CAGR, driven by food packaging exports and expanding automotive assembly.

The Netherlands, a key petrochemical and logistics hub, grows at 4.5%, leveraging advanced polymer facilities and integrated supply chains. France and Italy maintain steady expansion at 4.4% and 4.3%, respectively, supported by robust packaging, healthcare, and automotive industries.

Germany, representing Europe’s largest polymer market, grows at 4.2% CAGR, backed by mature automotive and industrial sectors, extensive polymer conversion infrastructure, and advanced recycling initiatives.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/27229

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-27229

Established and Emerging Manufacturers: Competing Through Innovation

The competitive landscape is dominated by integrated petrochemical producers and regional compounders competing on efficiency, performance, and sustainability.

Borealis, with a market share of approximately 9%, leads through circular polypropylene initiatives and mechanical and chemical recycling projects. Its Borstar catalyst technology enables advanced grade development for packaging and automotive applications.

LyondellBasell holds 8% of the market, leveraging its Spheripol process technology and large-scale European facilities to produce specialized resins optimized for automotive, industrial, and consumer goods sectors.

TotalEnergies, with a 6.5% share, integrates upstream feedstock operations with downstream polymer production, ensuring supply chain resilience and consistent quality.

SABIC, at 5.5%, continues to expand through advanced technical compound development and partnerships with automotive OEMs. Its focus on lightweighting and high-performance applications supports electric vehicle adoption and recyclable material integration.

Emerging regional players and compounders are also gaining ground by adopting circular economy business models. Firms in Poland, Czech Republic, and Spain are expanding compounding and recycling capacities to serve local converters and comply with EU’s Green Deal objectives.

Circular Economy Infrastructure and Technological Transformation

The EU’s polypropylene market is transitioning from a linear consumption model to a circular economy system anchored by recycling infrastructure, advanced sorting, and chemical upcycling.

Mechanical and chemical recycling technologies are enabling polymer producers to reintroduce post-consumer waste into the production cycle. Companies are developing compatibilizer-enhanced recycling processes and solvent-based purification systems to achieve food-grade recycled polypropylene.

These advances not only reduce environmental impact but also support brand owners and converters seeking to meet EPR and recycled-content mandates without sacrificing product performance or processing consistency.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube