The demand for potassium sulfate in the European Union is poised for steady expansion, advancing from USD 1.3 million in 2025 to USD 1.7 million by 2035, registering a CAGR of 2.9%. Although modest in pace, the market’s fundamentals point toward a resilient and economically logical trajectory, driven by high-value crop cultivation, sustainable farming practices, and precision agriculture adoption.

Potassium sulfate’s role in European agriculture is increasingly being defined by efficiency, sustainability, and profitability. For high-value crops — including vegetables, fruits, and vineyards — the mineral’s chloride-free composition offers a distinct agronomic advantage, ensuring yield quality and consistency. As EU agriculture shifts toward sustainability and organic standards, potassium sulfate’s compatibility with environmentally responsible production is cementing its position as a preferred input.

Efficiency, ROI, and Sustainability Drive Market Adoption

Farmers in Europe are gradually prioritizing return on investment (ROI) and operational efficiency when choosing fertilizers. Potassium sulfate, while costlier than commodity-grade alternatives, provides measurable gains in nutrient balance, crop size, and yield quality — factors that directly enhance revenue per hectare. These efficiency improvements make the input economically justified for premium horticulture and greenhouse cultivation.

The total cost of ownership in this sector extends beyond simple purchase price. Modern European farms incorporate fertigation and precision dosing systems, where potassium sulfate’s solubility and compatibility are crucial. Its use reduces water consumption, prevents over-fertilization, and enhances nutrient absorption — enabling long-term cost control and sustainability. For producers in Spain, Italy, and the Netherlands, these operational efficiencies translate to significant savings and improved environmental compliance.

Additionally, potassium sulfate aligns with Europe’s energy efficiency goals by minimizing irrigation demands and fertilizer wastage. In regions facing water scarcity or high operational costs, the mineral supports measurable productivity gains while reinforcing resource conservation.

Technological Advancements and Digital Integration

The modernization of EU agriculture continues to intersect with data-driven precision farming. Potassium sulfate’s compatibility with sensor-based fertigation and real-time nutrient monitoring tools makes it a vital input for next-generation farms. With soil sensors, drone imaging, and digital farm management platforms becoming more common, growers can now monitor potassium and sulfur levels accurately, ensuring consistent quality outcomes.

Manufacturers are increasingly focusing on formulation innovation — optimizing particle size, solubility, and nutrient ratios for hydroponic, greenhouse, and organic applications. The powdered form, which accounts for 42% of total demand, dominates the European market due to its water solubility and cost-effective production via the Mannheim process. This product segment is expected to strengthen further as controlled-environment farming expands across Western and Southern Europe.

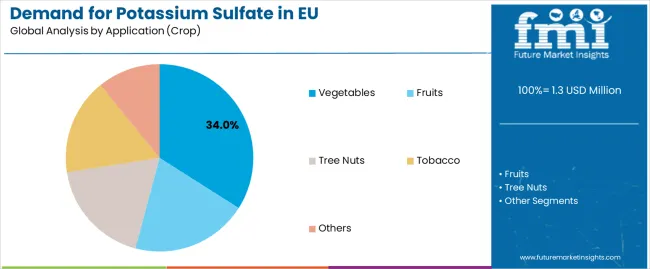

Vegetable and Horticultural Applications Lead Demand

Among all applications, the vegetable segment holds the leading share at 34%, reflecting the strong reliance of high-value greenhouse vegetable producers on chloride-free fertilizers. Greenhouse-grown tomatoes, cucumbers, and peppers are key beneficiaries, with potassium sulfate contributing to improved color, shelf life, and firmness — critical parameters in European retail and export markets.

Modern vegetable growers increasingly incorporate potassium sulfate into nutrient programs aimed at organic certification and premium produce markets, emphasizing its role in improving fruit quality and post-harvest stability. With expanding consumer demand for organic and high-quality vegetables, this segment is expected to remain the cornerstone of market growth through 2035.

Regional Demand: Spain and Netherlands Lead Growth

The regional analysis reveals a nuanced landscape. Spain leads the EU with a projected CAGR of 3.6%, driven by its intensive horticultural production and export-oriented fruit cultivation, particularly in citrus and table grapes. The Netherlands, growing at 3.1%, continues to showcase world-class greenhouse technology and advanced fertigation systems that rely heavily on water-soluble fertilizers.

Italy’s growth at 3.0% underscores its strong fruit and vegetable base, while France (2.7%) and Germany (2.4%) demonstrate stable demand supported by diversified horticulture and organic farming. Together, these nations form the backbone of Europe’s potassium sulfate demand, collectively representing over 70% of regional consumption.

In these markets, potassium sulfate plays an increasingly strategic role in chloride-sensitive crops, supporting not just productivity but also market differentiation through quality and sustainability credentials.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/27233

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-27233

Competitive Landscape: Established Leaders and New Entrants Innovate

Europe’s potassium sulfate industry is characterized by a mix of global giants and emerging regional specialists who are reshaping the market through innovation and sustainability.

K+S AG, with approximately 14% market share, continues to lead through its integrated Mannheim process facilities and extensive European distribution network. Its focus on agronomic advisory services and product quality has reinforced its presence among large-scale greenhouse and fruit producers.

ICL Group, holding about 11% share, leverages its diversified production base and extensive R&D capabilities to serve both conventional and organic segments. ICL’s European operations emphasize customized water-soluble formulations designed for precision agriculture and controlled-environment applications.

Tessenderlo Group contributes roughly 8% share, maintaining strong positions in fertigation-grade products for the greenhouse sector. Its expertise in water-soluble nutrients and long-standing relationships with horticultural producers have made it a key partner in sustainable crop programs.

Arab Potash Company, holding around 7%, strengthens the market with its natural mineral-based potassium sulfate exports and partnership-driven approach with EU distributors.

In parallel, new and regional manufacturers are entering the market with innovations in granule coating, particle engineering, and organic-grade certification — helping expand accessibility and reduce dependency on imports. Companies across Spain, the Netherlands, and Eastern Europe are setting up localized production units to meet growing regional demand efficiently.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube