The Middle East’s 3D printing materials market is entering a transformative growth phase, with demand expected to soar from USD 2.7 billion in 2025 to USD 12.6 billion by 2035, according to Future Market Insights (FMI). This remarkable 366.7% increase marks one of the fastest regional expansions globally, translating into a compound annual growth rate (CAGR) of 16.7%. The surge is driven by rapid additive manufacturing adoption in aerospace, healthcare, and industrial sectors, alongside government-led localization initiatives and digital transformation programs across the UAE, Saudi Arabia, and Israel.

Over the decade, both established global manufacturers and emerging regional players are reshaping the market through innovation, partnerships, and investment in advanced polymer, resin, and metal powder technologies. The 3D printing materials sector is no longer a niche field—it is becoming central to the Middle East’s industrial diversification, healthcare modernization, and aerospace competitiveness.

Regional Growth Anchored by Industrial Localization and Innovation

From 2025 to 2030, regional demand is expected to nearly double, rising to USD 6.1 billion. This phase will be characterized by accelerated adoption of FDM desktop and industrial printing systems, and a surge in photopolymer resin usage for medical and dental applications. Global leaders such as SABIC, Evonik, Arkema (Sartomer), and Stratasys are expanding their Middle Eastern operations, forming partnerships with GCC-based manufacturers to strengthen material availability and application support.

Between 2030 and 2035, the market will add another USD 6.5 billion, with growth driven by advanced metal powder technologies for aerospace applications, biocompatible materials for healthcare, and composite innovations for industrial and defense uses. Countries like the UAE, Saudi Arabia, and Qatar are investing heavily in digital spare parts programs and localized production networks, further boosting demand for specialized materials with precise technical capabilities.

UAE Leads with 3D Printing Mandates and Free Zone Expansion

The United Arab Emirates remains the Middle East’s 3D printing powerhouse, growing at an expected CAGR of 18.9%. Driven by Dubai’s 3D Printing Strategy and manufacturing free zone development, the country’s ecosystem fosters collaboration between government entities, technology startups, and global suppliers. Federal mandates that require 3D printing integration into construction, healthcare, and aerospace operations have positioned the UAE as a regional benchmark for additive manufacturing excellence.

Companies such as Stratasys and 3D Systems, operating through strong regional networks, are supporting this expansion with material portfolios tailored to high-temperature environments and certified for medical and aerospace use. Their efforts are complemented by new entrants and research institutions developing specialized polymers and photopolymers suited for local applications.

Saudi Arabia Strengthens Industrial Base with Vision 2030

Saudi Arabia follows closely with a projected CAGR of 17.6%, as the Vision 2030 initiative accelerates industrial diversification and manufacturing localization. National petrochemical leader SABIC is spearheading polymer production expansion, focusing on thermoplastic filaments and powder bed fusion materials. The country’s growing aerospace and healthcare sectors are also catalyzing demand for engineering thermoplastics and biocompatible resins, with new facilities integrating additive manufacturing into component production.

Saudi Arabia’s localization policies are attracting both multinational suppliers and regional startups, fostering technology transfer and local workforce training programs. The result is a resilient manufacturing ecosystem built around innovation, sustainability, and material self-sufficiency.

Israel Drives Medical and Aerospace Material Innovation

Israel’s robust innovation landscape continues to fuel demand for precision photopolymer resins and high-performance metal powders. With an expected CAGR of 16.8%, the country’s medical device and aerospace industries are advancing specialized resin formulations and titanium-based powders for surgical and defense applications. Partnerships between research institutes and material developers such as Evonik, Arkema, and Markforged are strengthening the region’s leadership in R&D-intensive additive manufacturing materials.

These developments are not only enabling Israel to meet domestic demand but also to export high-value materials and technologies across the GCC and European markets.

Material and Application Segmentation Reflects Market Sophistication

Polymers remain the dominant material category, accounting for 56% of regional demand in 2025. Engineering thermoplastics such as PA/PA12, ABS/ASA, and PETG/PC continue to support industrial and prototyping applications, while photopolymer resins are gaining traction in precision medical and dental printing. Metal powders, composites, and elastomers are expanding rapidly as industrial and aerospace sectors demand stronger, heat-resistant, and chemically stable materials.

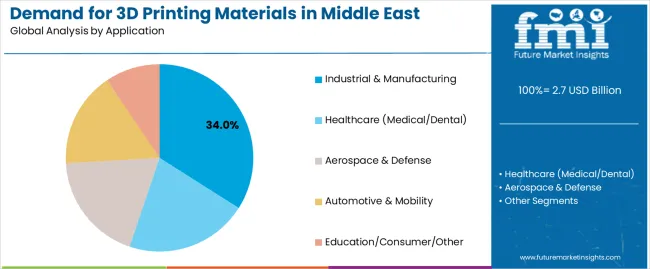

Industrial and manufacturing applications account for 34% of total demand, making them the largest application segment. The focus is on functional parts, jigs, and fixtures for low-volume production—core use cases that deliver immediate productivity and cost benefits.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/27126

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-27126

Innovation Pathways for Manufacturers and New Entrants

The Middle East’s 3D printing materials landscape presents unique entry points for both established manufacturers and new startups. For global leaders like SABIC, Evonik, and BASF Forward AM, the opportunity lies in expanding certified material offerings and deepening regional partnerships. Meanwhile, emerging local manufacturers are focusing on niche polymer formulations, biocompatible resin development, and cost-efficient filament production.

FMI highlights several strategic pathways, including the enhancement of polymer engineering capabilities, investment in healthcare-grade materials, and regional capacity expansion for metal powder systems. Such initiatives are expected to generate new revenue pools across industrial, healthcare, and aerospace sectors, with cumulative growth potential exceeding USD 900 million in specialized material innovation.

Competitive Landscape and Future Outlook

Competition in the Middle East’s 3D printing materials market is intensifying, with multinational corporations, equipment manufacturers, and regional distributors forming synergistic alliances. Companies such as EOS, Desktop Metal, and Sandvik are reinforcing their positions through technical collaborations and application-specific certifications. Continuous innovation in material properties, regulatory compliance, and digital process integration will define the next decade of market leadership.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube