The demand for polyisocyanurate (polyiso) insulation in the European Union is on a steady upward trajectory, projected to rise from USD 5.0 billion in 2025 to nearly USD 7.6 billion by 2035, growing at a compound annual rate of 4.3%. Verified by Future Market Insights (FMI), this increase represents an overall expansion of 52.9% as Europe accelerates its energy transition and enforces stricter thermal efficiency standards under the EU Green Deal framework.

This surge in demand is being powered by the region’s shift toward high-performance building materials that deliver superior thermal efficiency and long-term sustainability. Polyiso, with its exceptional R-value per inch, moisture resistance, and fire safety, has emerged as Europe’s preferred insulation solution across commercial roofing, continuous insulation, and advanced building envelope applications. Between 2025 and 2030, the market is expected to grow by USD 1.2 billion, primarily driven by energy code revisions, renovation activity, and the adoption of foil-faced rigid boards in both residential and commercial projects.

Sustainability, Building Codes, and Innovation Shape the Market Outlook

Europe’s tightening building energy codes have created a strong foundation for the insulation industry’s expansion. The European Performance of Buildings Directive (EPBD) and national codes in Germany, France, and the Netherlands are requiring ever-higher thermal resistance standards, pushing builders and specifiers toward polyiso as a high-value solution that combines insulation performance with fire safety.

Manufacturers are responding by developing non-halogenated flame retardants and bio-circular polyiso formulations designed to comply with the EU’s REACH regulation and sustainability targets. This shift toward greener chemistry is reducing reliance on TCPP-based systems and advancing low-emission, recyclable materials that align with Europe’s 2030 and 2050 carbon neutrality objectives.

By 2030, the polyiso industry will see rapid product diversification — from rigid boards and spray foams to hybrid insulation systems suited for below-grade waterproofing, cold storage, and zero-energy buildings. This wave of innovation is not only expanding market opportunities but also strengthening Europe’s position as a global leader in energy-efficient construction materials.

Established and Emerging Manufacturers Lead the Charge

The European polyisocyanurate insulation market is home to both long-established producers and emerging innovators committed to sustainability and technical excellence. Kingspan Group, with an estimated 18% market share, remains a leading force through its vertically integrated operations and expertise in insulated panels, roofing systems, and cold storage applications. The company continues to push boundaries with its low-GWP blowing agents and circular design principles that enhance recyclability.

Soprema Group, holding around 12% share, leverages its strong roofing and waterproofing portfolio, blending insulation with advanced building envelope technologies tailored for renovation markets. Recticel Insulation, accounting for about 10% share, maintains deep expertise in façade systems and building performance optimization, serving architects and contractors across continental Europe. Carlisle Construction Materials (EU), with a 7% share, continues to grow its European presence through integrated roofing systems and commercial contractor relationships.

New entrants and regional manufacturers, supported by polyurethane suppliers such as BASF SE and Dow, are increasingly focusing on TCPP-free and bio-based product lines. These developments are enabling smaller producers to compete through technological differentiation — offering advanced rigid boards, high-compressive-strength formulations, and systems tailored for circular economy objectives.

Rigid Foam Boards Dominate EU Insulation Demand

Among all product types, rigid foam and board insulation remains the undisputed market leader, accounting for approximately 53.5% of total sales in 2025 and expected to reach 54.5% by 2035. The segment’s dominance stems from its superior thermal stability, ease of installation, and ability to meet the strictest performance requirements for low-slope roofing and continuous insulation systems.

Contractors favor rigid boards for their dimensional accuracy and compatibility with mechanized installation methods, allowing faster project delivery without compromising quality. As continuous insulation becomes a regulatory necessity across Europe, rigid polyiso boards are expected to remain the material of choice for architects and builders seeking to eliminate thermal bridging and achieve higher energy ratings.

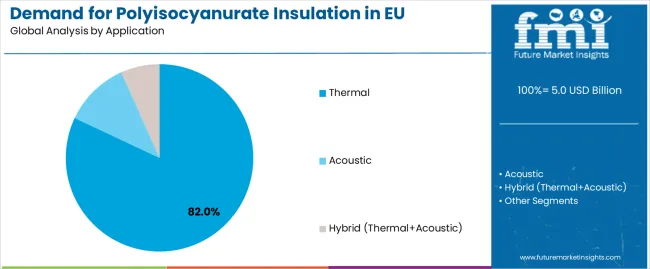

Thermal Insulation Leads Applications with 82% Market Share

Thermal insulation continues to represent the largest application segment, commanding an 82% market share in 2025 and maintaining near-dominance through 2035. Polyiso’s unrivaled R-value and compressive strength make it indispensable for thermal applications, from commercial roofing systems to residential walls and foundations.

The combination of rising energy costs and the EU’s decarbonization initiatives is encouraging property owners to invest in high-performance insulation systems that ensure long-term energy savings. Manufacturers are simultaneously enhancing moisture resistance and dimensional stability to ensure product reliability over decades of building operation.

Building & Construction Sector Drives Consumption Growth

The building and construction industry represents approximately 73.5% of total polyiso insulation demand in 2025, expanding slightly to 74% by 2035. This segment’s dominance is tied to Europe’s robust commercial roofing market, growing retrofit activities, and the widespread integration of continuous insulation into façade and wall designs.

Renovation incentives under EU green policies, particularly in Italy and France, are accelerating retrofit projects aimed at improving building energy efficiency. These trends are positioning polyiso as a material of strategic importance in achieving both economic and environmental goals.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/27139

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-27139

Technological Transformation and Circular Innovation Define the Future

From 2030 onward, technological advancements will define the industry’s next phase. Producers are increasingly integrating bio-based polyols, mass-balance-certified MDI, and recycled content materials into production lines to reduce embodied carbon and promote circularity. These efforts support EU directives on sustainable construction, with manufacturers publishing Environmental Product Declarations (EPDs) and lifecycle carbon assessments to prove environmental performance.

The adoption of non-halogenated flame retardants and low-GWP blowing agents marks another leap forward. Companies are developing phosphorus-based and mineral-enhanced formulations that deliver equivalent fire protection to conventional products while minimizing environmental impact — a vital step for compliance with evolving European chemical standards.

Country Insights: Spain, Netherlands, and Germany Take the Lead

Spain is projected to record the fastest growth at a CAGR of 4.8%, fueled by renewed construction activity and strict energy efficiency regulations. The Netherlands follows closely with 4.7% growth, driven by green construction mandates and BREEAM-certified developments prioritizing sustainable insulation materials. Germany, maintaining the largest market share at over 30%, continues to set benchmarks in building quality and energy performance standards through its EnEV regulations and advanced architectural practices.

France and Italy also contribute substantially to overall demand, benefiting from renovation subsidies and energy retrofit programs aligned with national decarbonization policies.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube