The global microcellular foam market is entering a period of transformative expansion, expected to grow from USD 6,975.6 million in 2025 to an impressive USD 21,665.3 million by 2035. This robust rise represents an absolute gain of USD 14,689.7 million, or a 210.6% total growth, translating into a CAGR of 12.0% over the decade. The market’s growth trajectory, nearly tripling in value within ten years, underscores how lightweighting, environmental sustainability, and advanced material technologies are shaping the future of manufacturing across key industries like automotive, packaging, electronics, and medical devices.

Microcellular foam technology, distinguished by its microscopic cellular structure, has rapidly evolved from niche industrial applications into a critical component of modern lightweight materials engineering. Its strength-to-weight ratio, structural stability, and energy absorption capabilities make it indispensable in automotive design, high-performance electronics, and next-generation packaging. As manufacturers and research institutions seek to balance performance, cost-efficiency, and sustainability, microcellular foams have become a cornerstone material supporting this global transition.

Between 2025 and 2030, the market is projected to increase from USD 6,975.6 million to USD 12,293.5 million, marking an addition of USD 5,317.9 million—roughly 36.2% of total decade-long expansion. This first growth phase will be defined by accelerating automotive lightweighting efforts, surging demand for recyclable packaging materials, and broader adoption in electronics and medical applications. Established players like BASF, Dow Chemical, and Huntsman are scaling production capabilities and investing in R&D to develop advanced polyurethane-based microcellular foams with superior processability and reduced environmental footprint.

From 2030 to 2035, the market’s second expansion phase will add another USD 9,371.8 million, contributing nearly 64% of the total decade growth. This period will witness the emergence of next-generation foam technologies designed for premium applications, green manufacturing, and recycling integration. Companies such as Saint-Gobain Performance Plastics, Evonik, and Rogers Aerospace are expected to lead innovation in high-performance foams for aerospace, defense, and electronics, focusing on properties like thermal stability, biocompatibility, and enhanced recyclability. The shift toward material circularity—where foams are designed for reuse and reprocessing—is poised to redefine production models across the global supply chain.

The market’s expansion is largely anchored in the increasing global demand for lightweight materials. Automotive manufacturers are aggressively pursuing materials that reduce vehicle weight without compromising strength or safety, driven by emission regulations and fuel efficiency mandates. Microcellular foams have emerged as ideal solutions for replacing heavy traditional polymers, metals, and composites in both structural and interior components. Simultaneously, the packaging industry is adopting eco-friendly foam variants that offer recyclability, superior protection, and reduced material consumption—key factors aligning with sustainability mandates and consumer preferences.

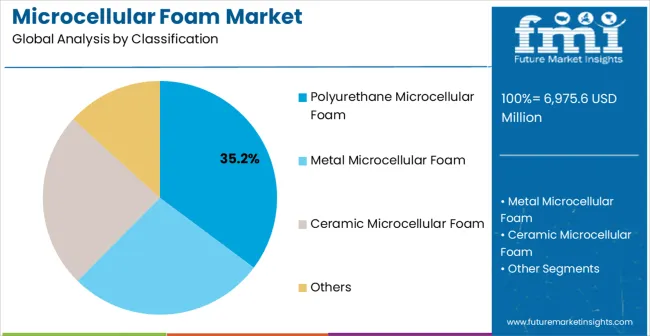

Polyurethane microcellular foam stands out as the leading material type, accounting for 35.2% of the market in 2025. Its dominance stems from processing versatility, stable chemistry, and compatibility with mass production environments. Major players like Wanhua Chemical Group, ERA Polymers, and Shincell are enhancing polyurethane formulations to improve flexibility, durability, and environmental performance, ensuring the material remains a preferred choice across automotive, footwear, and electronics applications. Meanwhile, specialized segments such as metal and ceramic microcellular foams are gaining attention for their use in aerospace and defense—markets where high-temperature tolerance and structural rigidity are paramount.

By application, the automotive sector leads with a projected 39.0% market share in 2025. Automakers increasingly rely on microcellular foams for crash protection, insulation, and structural efficiency. As governments worldwide tighten emission standards, manufacturers like BMW, Toyota, and Tesla are partnering with advanced materials companies to integrate lightweight foams into electric vehicle platforms. Beyond automotive, sectors such as consumer electronics and medical devices are driving growth in high-precision foam formulations that provide vibration damping, insulation, and biocompatibility for sensitive components and instruments.

Regionally, Asia Pacific will remain the growth powerhouse, with China and India demonstrating staggering CAGRs of 16.2% and 15.0%, respectively. China’s rapid automotive manufacturing expansion, supported by government incentives and investments in material technology, positions it as the global leader in microcellular foam production and consumption. Domestic players such as Ningbo Micro-foam Technology and Shanghai Huayi Group are building large-scale production facilities to meet rising domestic and export demands. In India, the “Make in India” initiative and growing electronics manufacturing ecosystem are fueling adoption across multiple sectors.

Germany continues to lead Europe’s microcellular foam market, with a CAGR of 13.8% through 2035. The country’s engineering excellence, particularly in automotive and aerospace applications, ensures steady demand for premium foams that meet stringent performance requirements. Companies like BASF and Evonik are at the forefront of developing sustainable foam formulations that support Europe’s broader climate goals. The United States follows closely with an 11.4% CAGR, backed by strong research infrastructure and adoption in advanced automotive and industrial manufacturing.

In Latin America, Brazil is emerging as a key regional player with a CAGR of 12.6%, driven by automotive sector growth and increasing awareness of lightweight material advantages. Meanwhile, Japan maintains steady progress at 9.0%, emphasizing precision manufacturing and high-quality foam products that cater to both domestic and export markets. These regional trends reflect a global alignment toward innovation, sustainability, and performance optimization.

Established global leaders such as BASF, Dow Chemical, and Saint-Gobain continue to dominate the competitive landscape with comprehensive materials portfolios, advanced R&D programs, and global manufacturing networks. Huntsman, Evonik, and Rogers Aerospace focus on high-value applications, integrating chemistry innovation and specialized foam processing for critical industrial use. On the other hand, emerging companies such as TOPWIN, MATSUI, and Aearo Technologies are carving out niches in performance-driven markets by leveraging cost-efficient production methods and targeting high-growth sectors like automotive interiors and energy-efficient packaging.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/26858

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-26858

Manufacturers are not only competing on material performance but also on sustainability credentials. Companies are introducing eco-friendly foam formulations designed for recyclability and integrating renewable raw materials into their production processes. Wanhua Chemical Group, for instance, is investing heavily in closed-loop foam production systems, while Cymat Technologies and Alulight International are pioneering metal-based microcellular foams tailored for aerospace and defense applications. Such developments are reshaping the market into a hub for green innovation and technology-driven transformation.

Technology integration remains at the forefront of market evolution. Automation, precision foaming systems, and AI-assisted material optimization are improving production efficiency and reducing waste. As industries transition toward net-zero objectives, the integration of clean manufacturing systems is expected to become a defining feature of next-generation foam production. Advanced foams with optimized cell structures, improved mechanical stability, and reduced energy input requirements are set to dominate the product pipelines of leading manufacturers by 2035.

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube