The global metal casting market is entering a pivotal decade of expansion, projected to grow from USD 159.9 billion in 2025 to approximately USD 255.6 billion by 2035. This represents a total increase of nearly USD 95.6 billion, marking a 59.8% surge in market value and an impressive compound annual growth rate (CAGR) of 4.8%. This expansion reflects the vital role metal casting plays in modern industrial ecosystems — from automotive manufacturing to infrastructure development and renewable energy systems.

As the global demand for lightweight, durable, and high-performance metal components intensifies, foundries worldwide are upgrading technologies and expanding capacity. Established players such as Dynacast Ltd., GF Casting Solutions, Rheinmetall, and Ryobi Limited are strengthening their global presence with new casting methods, while emerging manufacturers in Asia and Latin America are entering the industry through strategic collaborations and advanced automation adoption.

Growth Drivers: Automotive and Infrastructure Propel the Market

The metal casting market’s growth is intrinsically linked to the ongoing transformation in the automotive sector. Manufacturers are increasingly prioritizing lightweight components that enhance fuel efficiency and comply with stringent emission standards. Complex engine blocks, transmission housings, and structural parts are now produced using precision casting methods to ensure high strength and reliability. With automotive applications accounting for 60% of total demand, foundries are leveraging new technologies to meet evolving performance expectations.

Parallelly, infrastructure development across emerging economies continues to accelerate demand. Rapid urbanization in countries such as China, India, and Brazil is creating strong demand for metal cast components used in construction, industrial machinery, and transportation systems. As governments roll out infrastructure and renewable energy projects, the requirement for robust, high-tolerance cast metal parts is expected to increase dramatically through 2035.

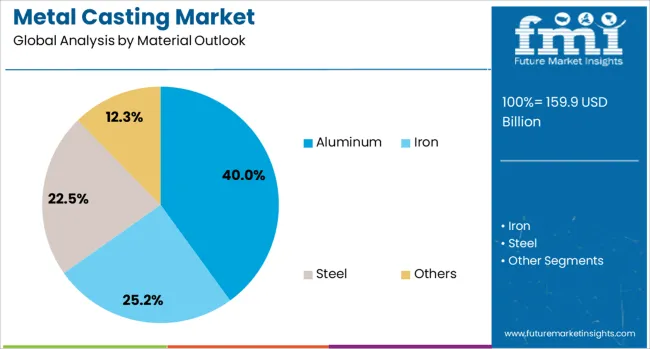

Aluminum Leads Material Segments with Sustainable Potential

Among material categories, aluminum remains dominant, capturing 40% of the total market share in 2025. Its superior properties — including light weight, corrosion resistance, and thermal efficiency — make it indispensable for automotive and aerospace components. The rise of electric vehicles (EVs) has further bolstered aluminum demand due to its recyclability and contribution to vehicle range optimization.

The continuous development of advanced aluminum alloys and casting processes is enabling greater precision, design flexibility, and cost efficiency. Established manufacturers like Alcast Technologies Ltd. and Ahresty Corporation are pioneering aluminum die-casting innovations, while smaller regional producers are investing in alloy development to gain a foothold in the evolving mobility ecosystem.

A Decade of Two Distinct Phases of Growth

Between 2025 and 2030, the metal casting industry is projected to grow from USD 159.9 billion to USD 200.9 billion, representing 42.9% of total forecasted expansion. This phase will be driven primarily by the post-pandemic manufacturing rebound, surging automotive production, and construction booms across Asia and the Middle East.

From 2030 to 2035, market value is forecast to increase by an additional USD 54.6 billion, contributing 57.1% of the decade’s overall growth. This second phase will mark a transition toward automation, digital foundries, and green casting processes, where sustainability and precision become central to competitive strategy. Integration of Internet of Things (IoT) technologies and data analytics in foundries will enable real-time monitoring, predictive maintenance, and optimized production cycles — all crucial for quality consistency and resource efficiency.

Automation, Digitalization, and Green Casting Shape the Future

Modern foundries are evolving beyond traditional production environments into digitally connected ecosystems. Robotics, 3D sand printing, and AI-based quality inspection are reshaping how metal components are designed and manufactured. The introduction of automated handling systems and smart monitoring sensors ensures improved consistency, safety, and throughput.

In parallel, sustainability has emerged as a key differentiator. Foundries are transitioning toward low-emission casting technologies, waste heat recovery systems, and eco-friendly alloys to comply with tightening global environmental regulations. Companies like GF Casting Solutions and Endurance Technologies Limited are actively investing in carbon-neutral foundry operations to align with global net-zero goals.

For stakeholders and investors, the shift toward eco-efficient production not only reduces operational costs but also positions them favorably in supply chains that increasingly prioritize environmental responsibility.

Regional Outlook: Asia Leads, Europe Innovates, and North America Stabilizes

The regional performance of the metal casting market highlights a dynamic global landscape. China leads with a 6.5% CAGR, fueled by large-scale automotive production, infrastructure megaprojects, and government-backed industrial policies promoting advanced manufacturing. The country’s modernization of foundry technologies and workforce training programs continues to set global benchmarks.

India, expanding at 6.0% CAGR, is rapidly developing its automotive and industrial casting capabilities, supported by the “Make in India” initiative. The growth of domestic OEMs and the expansion of global auto manufacturers in the region are driving the demand for high-quality, cost-effective cast metal parts.

In Europe, Germany remains the leader with 5.5% CAGR, driven by its world-class automotive engineering ecosystem. The country emphasizes precision casting technologies and sustainability-focused production. France (5.0%) and the United Kingdom (4.6%) follow closely, leveraging their strengths in aerospace, defense, and high-value component manufacturing.

Meanwhile, the United States maintains a steady 4.1% CAGR, relying on a mature industrial base and technological advancements in casting automation. Brazil, growing at 3.6%, showcases developing industrial potential and rising automotive manufacturing capabilities, signaling opportunities for international partnerships.

Competitive Landscape: Established Leaders and Rising Challengers

Competition in the metal casting market is intensifying as established corporations and new entrants race to secure their positions in a transforming global industry. Market leaders like Dynacast Ltd., GF Casting Solutions, Rheinmetall AG, and Ryobi Limited dominate high-precision automotive and industrial casting segments with advanced digital and automation-driven facilities.

Alcast Technologies Ltd. specializes in high-strength aluminum components for the automotive and industrial sectors, while Endurance Technologies Limited has become a major supplier for the Indian and global two-wheeler and passenger car markets. Ahresty Corporation and Proterial, Ltd. from Japan continue to drive innovation through alloy enhancement and process automation.

In the United States, Calmet and Metrics Holdings are strengthening their presence through precision casting solutions and alloy innovation, particularly in defense and industrial equipment. Emerging manufacturers across Asia are now investing in robotic foundry operations and simulation-based design platforms to match international production standards and cost competitiveness.

Purchase this Report for USD 5,000 Only | Get an Exclusive Discount Instantly! https://www.futuremarketinsights.com/checkout/26154

Everything You Need—within Your Budget. Request a Special Price Now! https://www.futuremarketinsights.com/reports/sample/rep-gb-26154

About Future Market Insights (FMI)

Future Market Insights, Inc. (ESOMAR certified, recipient of the Stevie Award, and a member of the Greater New York Chamber of Commerce) offers profound insights into the driving factors that are boosting demand in the market. FMI stands as the leading global provider of market intelligence, advisory services, consulting, and events for the Packaging, Food and Beverage, Consumer Technology, Healthcare, Industrial, and Chemicals markets. With a vast team of over 400 analysts worldwide, FMI provides global, regional, and local expertise on diverse domains and industry trends across more than 110 countries.

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

Website: https://www.futuremarketinsights.com

LinkedIn| Twitter| Blogs | YouTube